With expectations baked in for a Reserve Bank of Australia (RBA) rate cut next week, all eyes are on how this long-awaited monetary shift will reshape Australia’s economic landscape. The major banks are in rare alignment, unanimously forecasting a 25 basis point reduction in the cash rate—from 3.85% down to 3.6%—as inflation softens and household stress intensifies. There are even some analysts that suggest a 50 basis point reduction is possible this time around. Markets are pricing in a 97% chance of this move. The RBA rate reflects more than just market momentum. It is are a mirror of Australia’s evolving macroeconomic reality. Amid this transition, precious metals remain in sharp focus. At the time of writing, gold is trading at AUD $5,072, silver at AUD $56.11, and platinum continues its surge, now at AUD $2,112.

The Case for a Cut: Inflation Tamed, Growth Falters

The RBA’s mandate is to balance full employment with price stability, targeting inflation between 2–3%. With inflation now at 2.4%, within that comfort zone, and retail sales growth barely above zero, the path is clear for easing monetary policy. ANZ, NAB, Commonwealth Bank, and Westpac all project further rate reductions beyond July’s meeting, with some forecasts suggesting as many as four cuts by May 2026. The anticipation of weak wage growth, slowing job creation, and a deteriorating participation rate strengthen this argument. Meanwhile, GDP per capita has been declining for six consecutive quarters, marking the deepest real income per capita recession for a very long time. Against this backdrop, justification for monetary easing is a logical position.

Weakening AUD: A Tailwind for Precious Metals

As Australian interest rates decline relative to those abroad, our local currency tends to weaken. This is because a rate cut makes Australian assets (such as Treasury bonds) less attractive to foreign investors, who then seek higher yields outside of Australia. Reduced investment capital inflows combined with increased outflows is one element that pushes the currency downward; however, there are multiple facets that combine that affect currency movement.

Because the American Dollar is the currency that precious metals are priced in, it is important to also consider USD’s position. The Greenback is in a downward spiral compared to other currencies including our own. Aggressive fiscal policies, rising debt, trade policies and tariff uncertainties, international shifts toward de-dollarisation, lack of investor confidence and how this affects capital flows all play a role in weakening the dollar.

Both reserve bank rate cuts and the moving of the USD is important to factor in when considering the Australian dollar and its effect on precious metals prices. Precious metals have historically outperformed during such currency devaluations—both as inflation hedges and stores of value when fiat confidence erodes. For investors holding physical bullion in Australian dollars, a falling AUD boosts returns even if global spot prices remain flat.

Property’s Artificial Revival: Short-Term Relief, Long-Term Risk

While a rate cut will offer welcome relief to mortgage holders—saving approximately $90 a month on a $600,000 loan—it is also likely to reignite speculative heat in the housing market. Research suggests a 0.25% rate cut can lift property prices by 1.5% to 2% within a year. With housing supply constrained and affordability stretched, this risks deepening the divide between asset holders and younger Australians priced out of the market. It also highlights the fragility of a property market reliant on low interest rates for price support. Lower rates may buy time, but they do not resolve structural imbalances. Investors should therefore consider diversifying into hard assets with a different risk profile—particularly as debt burdens and global volatility mount. When the property market finally corrects, capital will leave this sector and look for another venue to both preserve wealth and continue growth.

Why Now Is the Time to Buy Gold, Silver, and Platinum

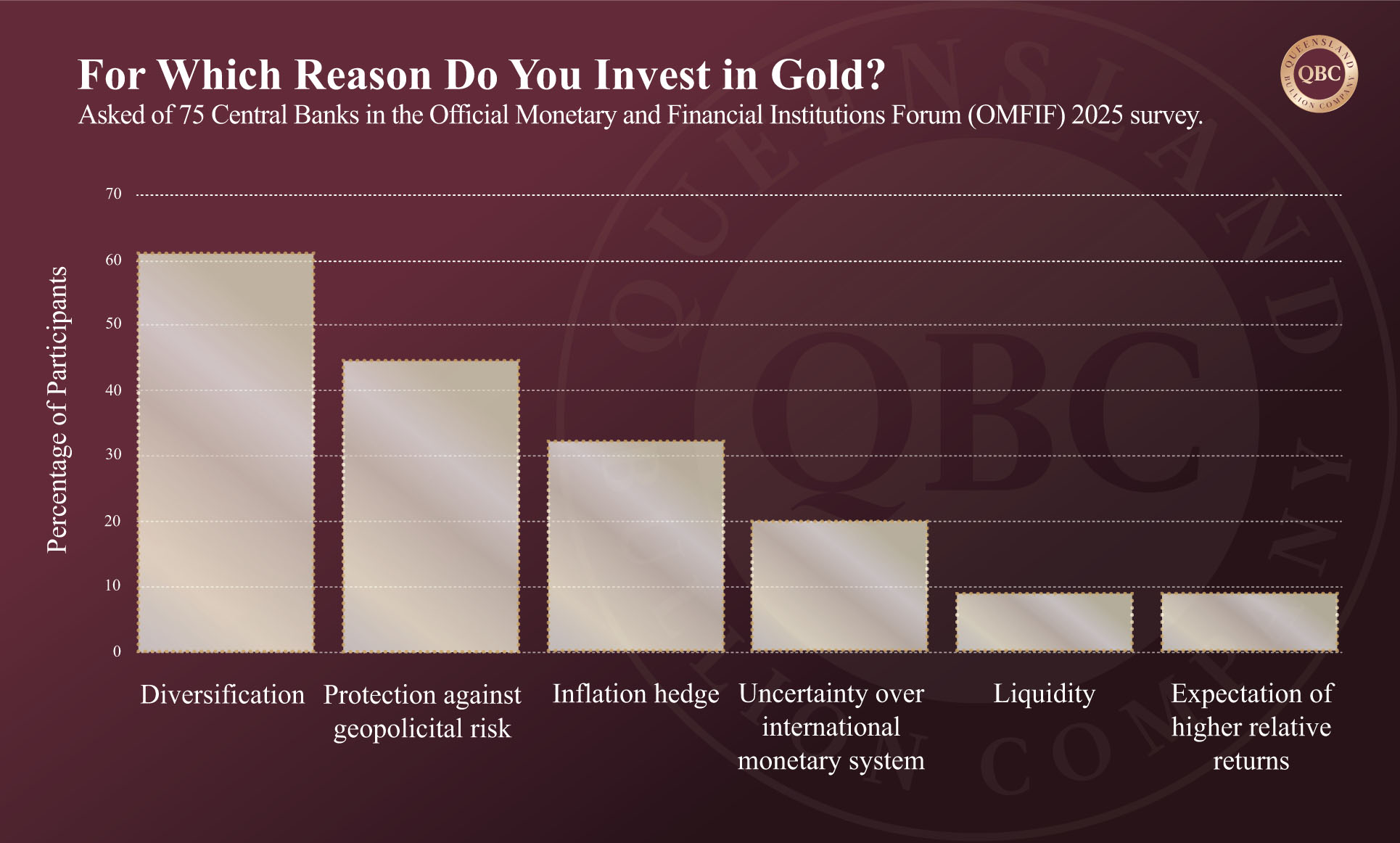

The anticipated rate cut marks more than a tactical shift in policy—it is a signal that Australia’s monetary authorities are preparing for an extended period of a softer economy. With central banks worldwide still buying gold—32% planning to increase reserves in the next year—and with physical shortages emerging in both silver and platinum markets, the case for owning precious metals has never been clearer. Add to this the RBA’s likely reluctance to provide forward guidance, and investors are left to navigate uncertainty with limited visibility. In this environment, physical gold, silver, and platinum offer the one thing the broader market cannot: simply stability. They are not just a hedge against rate cuts or currency weakness—they are protection against a system increasingly reliant on monetary intervention for survival.

As we often tell our clients there is nothing more certain in an uncertain world than precious metal.