Moody’s Downgrade and Market Reaction: Implications for Gold

by Evie SoemardiMoody’s has downgraded the United States’ credit rating this week from AAA (negative) to AA1 (stable), and in doing so, put the stock market in a tailspin. The result for precious metals was an initial rise in value with a softening in prices overnight. With gold trading at AUD $5,160, silver at AUD $51.78, and platinum at AUD $1,706.57, it is difficult to predict what direction precious metals will take without assessing the role that American government bond rates have on the stock market, real estate, and consequently, gold and silver. After all, they all compete for the same market capital.

The downgrade and what it means

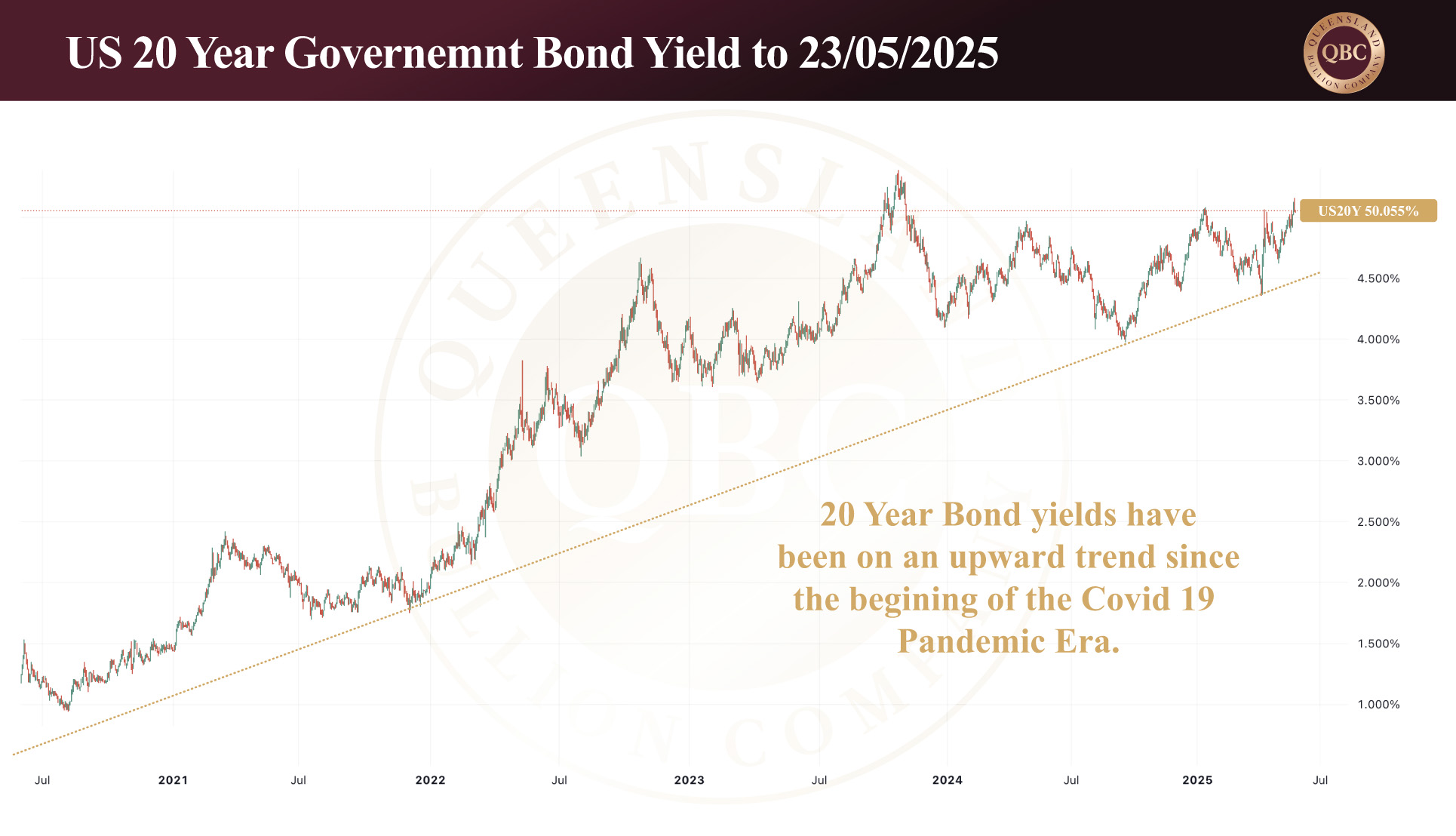

When Moody’s downgraded the US credit rating, it essentially reinforced the growing scepticism amongst investors of the government’s ability to pay back their debt. This is reflected in the recently auctioned 20-year Treasury bonds where investors held out for interest rates as high as 5.16%. To put this in perspective, the pre-Pandemic Era rate was only 1.19%. While it is a great result for those investing in bonds, it has caused a significant pull back in equities.

How do bond rates affect equities? Simply put, the private sector needs to provide better financial yields than the government—and it’s not. With a perfect track record of paying debt (and the ability to print money), the government is seen as low-risk and reliable when it comes to honouring their treasury bonds—the mechanism by which they sell their debt. If confidence in the government’s ability to do so is compromised, then the market dictates a higher interest rate for returns prior to purchasing to reflect any perceived risks. This is what unfolded in the last week.

On the other hand, the private sector (stock market) is seen as a higher risk when it comes to investing. It generally must provide higher returns than government bonds to attract capital. Stock dividends are set according to free cash flow. Hence, the only way to secure higher yields than those investing in bonds is to wait for the value of the shares to drop while dividends remain the same. The result is that investors pause their equity purchases and the stock market dips—just as it did this week as the Dow Jones Industrial Average (DJI) sank more than 800 points, or nearly 2%.

Margin calls

At this point, it could be argued that it’s a win/win situation. Bond holders have secured higher interest rates and equity investors better value; however, the point of contention has simply been moved onto the publicly traded companies. If the value of their shares goes down, so does the asset that the investor relies on for funding. As asset values decrease, the potential result is a margin call from the investor’s financiers wherein they may be obliged to sell off assets to close their position.

The swift selling of assets in such a fashion is what preceded the Global Financial Crisis (GFC), and this is the underlying concern regarding high Treasury bond interest rates. It is market mechanisms that dictate bond interest rates and share prices—not the government or the Federal Reserve. Ultimately, both must give in to the market or risk catastrophic financial pain.

Where does this leave gold?

There are two ways this can play out for gold. If bond yields remain high, then the price of gold may soften as it competes against bonds for capital. By this we mean, that investors may obtain government debt with a higher interest rate which may be more beneficial than an asset increasing in value. However, when American bond yields are high, they are usually accompanied by a stronger Greenback. Also, if the underlying cause drivers are fiscal stress, credit worries or persistent inflation fears, real yields actually stay depressed, allowing gold to hold ground or rally. The implication for Australian investors is that it could potentially signal a higher value of gold in local markets.

However, fundamentally the Western financial system is far from healthy. Read about factors that play into this—such as inflation and the Fed’s balance sheet, overvaluation of stocks and real estate, and the repatriation of gold—in our previous articles. If bond yields normalise and the status quo is re-established, then eventually the West will have to take its medicine and deal with these systemic failures. If the price remains soft, consider it a perfect time to hedge against financial uncertainty by investing in gold.