The West’s Financial Challenges are Structural, Not Situational

by Evie SoemardiMarkets continue to react to every diplomatic ripple in the Middle East, pricing gold up or down depending on the headlines of the day. But while newsrooms focus on missiles and ceasefires, a deeper crisis continues to unfold in the background—one that will shape the future of fiat currencies and precious metals alike. From spiralling sovereign debt to persistent supply deficits and fragile delivery mechanisms, the evidence points to a fundamental, structural strain underpinning today’s global economy. Geopolitical tension may be the match, but the kindling has long since been laid. As one seasoned analyst noted recently: “If you’re waiting for gold to collapse once the Middle East quiets down, you might be missing the bigger picture.” With gold trading at AUD $5,038, silver at AUD $55.98, and platinum at AUD $2,123.49, let us explore why the structural health of the financial system does not need a bomb in order to rupture.

Debt Crisis

As far as potential catalysts go for financial shakedowns, one of the most pressing structural fault lines in global markets today is debt. According to the Institute of International Finance, global debt has now reached an eye-watering $325 trillion, representing 328% of world GDP—a record. This isn’t merely a by-product of recessionary cycles or COVID-era stimulus; it is a long-standing trajectory embedded in Western fiscal planning. Ray Dalio, founder of Bridgewater Associates, warned just weeks ago that the U.S. faces a “debt-induced economic heart attack” if current trends persist. Most notably, U.S. interest payments now exceed defence spending—a staggering milestone for the world’s largest economy. The debt ceiling has become a floor which has become the baseline expectation for government spending. For investors, this undermines faith in fiat currency systems and highlights the appeal of tangible, non-counterparty assets like gold and silver. The Federal Reserve’s swollen balance sheet, combined with sticky inflation, suggests that central banks are trapped between credibility and solvency, a problem that ultimately cannot be printed away like so many other fiscal and financial problems.

Silver and Platinum Supply Deficits

Silver and platinum both entered structural deficits years ago—an imbalance long underreported by official figures. Since 2021, silver demand has consistently outpaced supply driving prices over 50% higher. While the Silver Institute projects a slightly narrower deficit in 2025—117 to 118 million ounces, down from 148.9 million in 2024—these numbers exclude key emerging sectors. Military demand remains unquantified. Indicators for this use remain opaque at best and is estimated to amount to up to fifteen times more than any other industrial application. Likewise, silver’s expanding role in emerging industries such as aerospace, AI, robotics, and solid-state batteries is inadequately captured in conventional forecasts. Platinum faces similar dynamics: a two-year supply shortfall of nearly one million ounces persists despite growing industrial and green energy demand. As hydrogen cell vehicles enter the mainstream, platinum’s role has become increasingly strategic. With 90% of global supply coming from geopolitically sensitive regions like South Africa and Russia, the risk of supply shock is high—and rising. Investors should take note: these are not temporary bottlenecks, but long-term mismatches between available resources and accelerating use cases. Read more about platinum here.

Gold and Institutional Buying

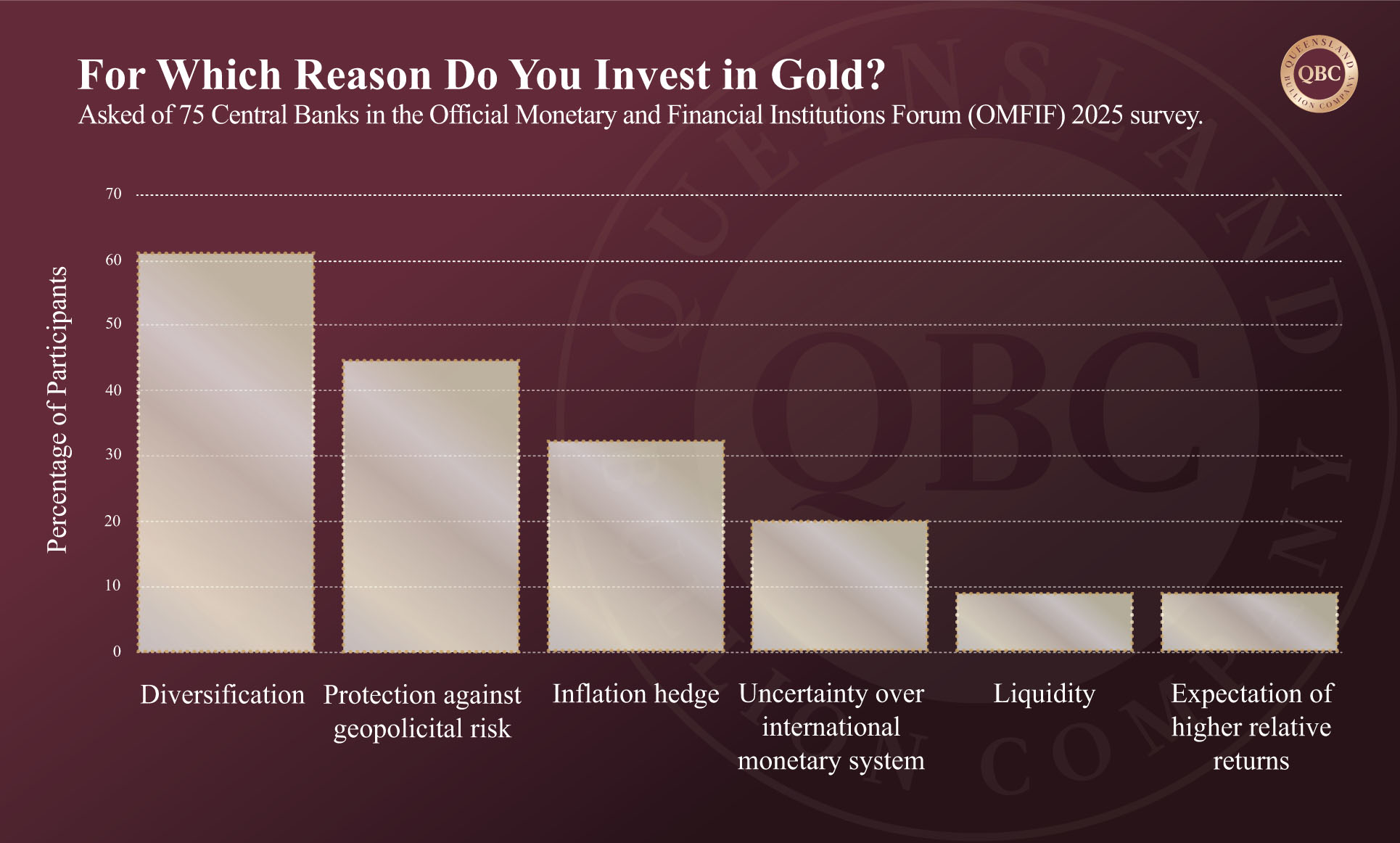

While silver and platinum gain industrial-use momentum, gold remains the reserve asset of choice for institutions. According to the latest Official Monetary and Financial Institutions Forum (OMFIF) survey, 32% of central banks intend to increase their gold holdings over the next 12–24 months—the highest conviction rate in five years. This is not a short-term trade. The reasons are clear with the first priority being diversification, then hedging geopolitical risk, and then protecting against inflation. For the fourth consecutive year, analysts expect central bank gold purchases to exceed 1,000 tonnes. This sustained and deliberate accumulation reflects how gold is not just seen as a wealth preservation tool, but increasingly also as a protection against future instability. What is striking is how quietly this repositioning is occurring. While retail investors chase headlines, central banks are rebuilding their balance sheets with physical bullion. This suggests an enduring revaluation of gold’s role not just as a crisis hedge, but as a strategic reserve asset. Institutional demand does not chase price; it sets the floor beneath it.

The Silent Precious Metals Crisis

Beneath the surface of daily spot movements lies a more alarming trend: the growing disconnect between paper and physical precious metals markets. In Q1 2025, only 1.2% of COMEX gold and 0.9% of silver futures contracts ended in physical delivery. Meanwhile, May 2025 saw a staggering 16,200 silver contracts—equal to 81 million ounces—stand for delivery, consuming 16% of registered COMEX inventories. This is the highest delivery-to-stock ratio since 2008 and signals serious stress within the system. Alarmingly, 23% of silver delivery requests were redirected to cash settlement, up from 12% in 2024. This means the warehouse system cannot reliably meet physical obligations. Adding to concerns, 84% of silver futures are held by a handful of commercial traders—primarily investment banks—who dominate spread trading and price discovery. The $920 million JP Morgan spoofing settlement resolved only 0.3% of the firm’s alleged manipulative trades executed between 2015-2020, underscoring the depth of systemic vulnerabilities in precious metals paper trading. The illusion of liquidity in the paper market masks an increasingly illiquid physical reality—a dangerous divergence for any asset class, but especially for metals regarded as trust anchors in uncertain times.

Conclusion: Structural, Not Situational

Markets will always respond to geopolitical shockwaves, but the deeper story is the slow-motion erosion of economic foundations. The West’s financial challenges are not about any single war, central bank statement, or election cycle; they are the cumulative result of structural imbalances—runaway debt, overstretched supply chains, institutional manipulation, and a global pivot back to tangible assets. Precious metals are not spiking or softening solely because of crisis headlines; they fluctuate because the scaffolding beneath fiat currency systems is beginning to creak. Investors who understand this distinction—who look beyond the noise and into the bedrock—are those best positioned for the decade ahead. In this environment, gold, silver, and platinum are not just hedges. They are a means to survive and thrive.