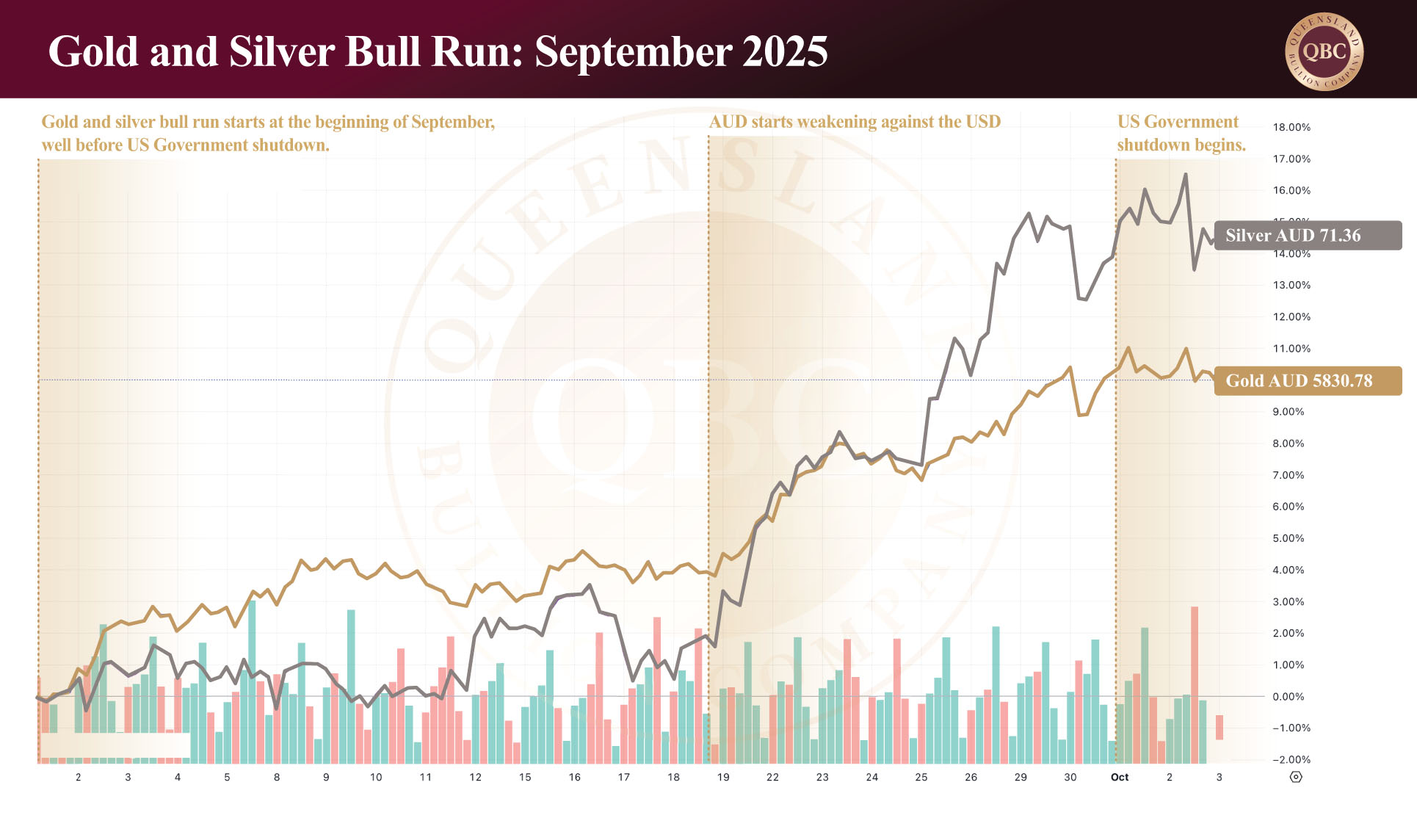

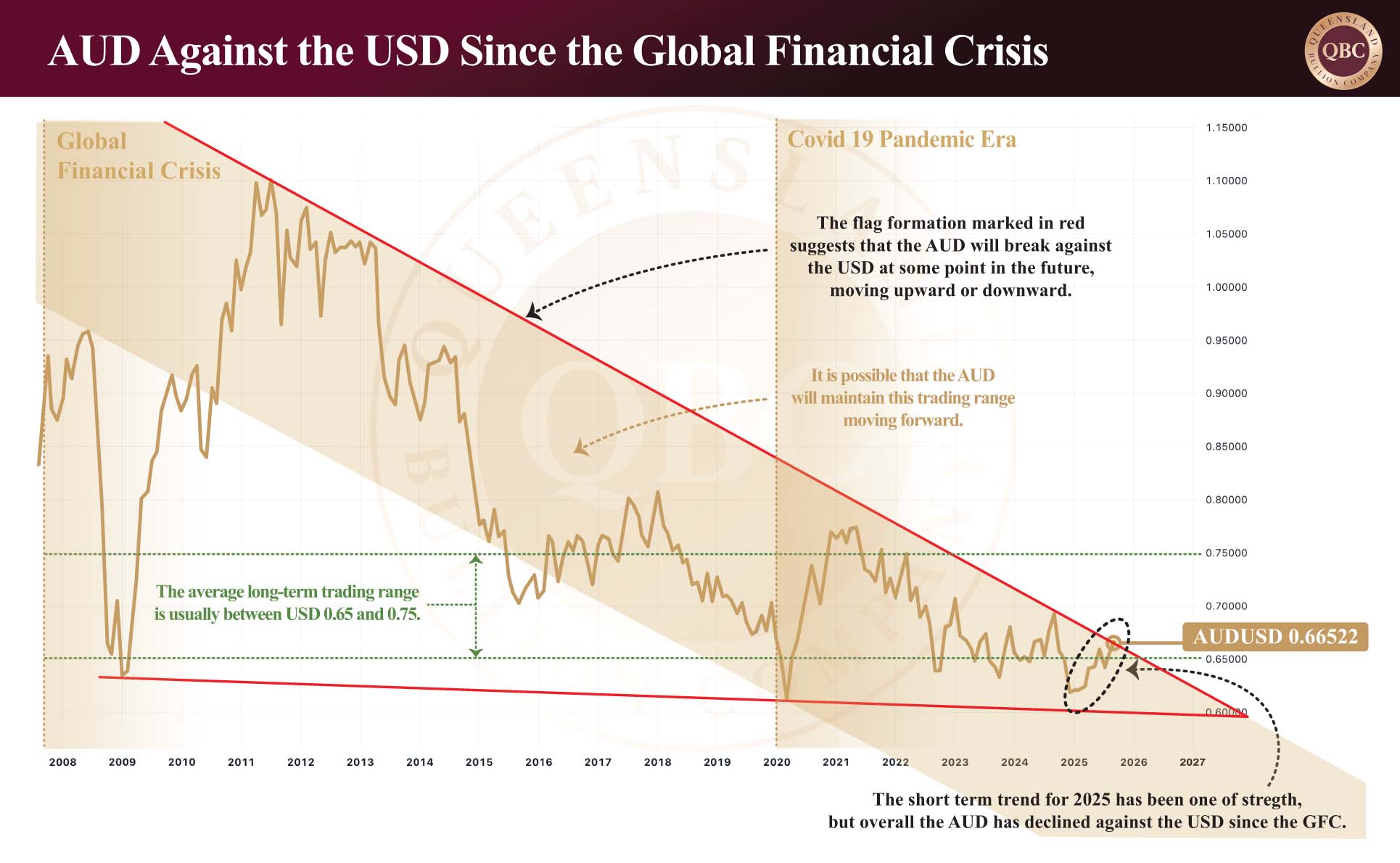

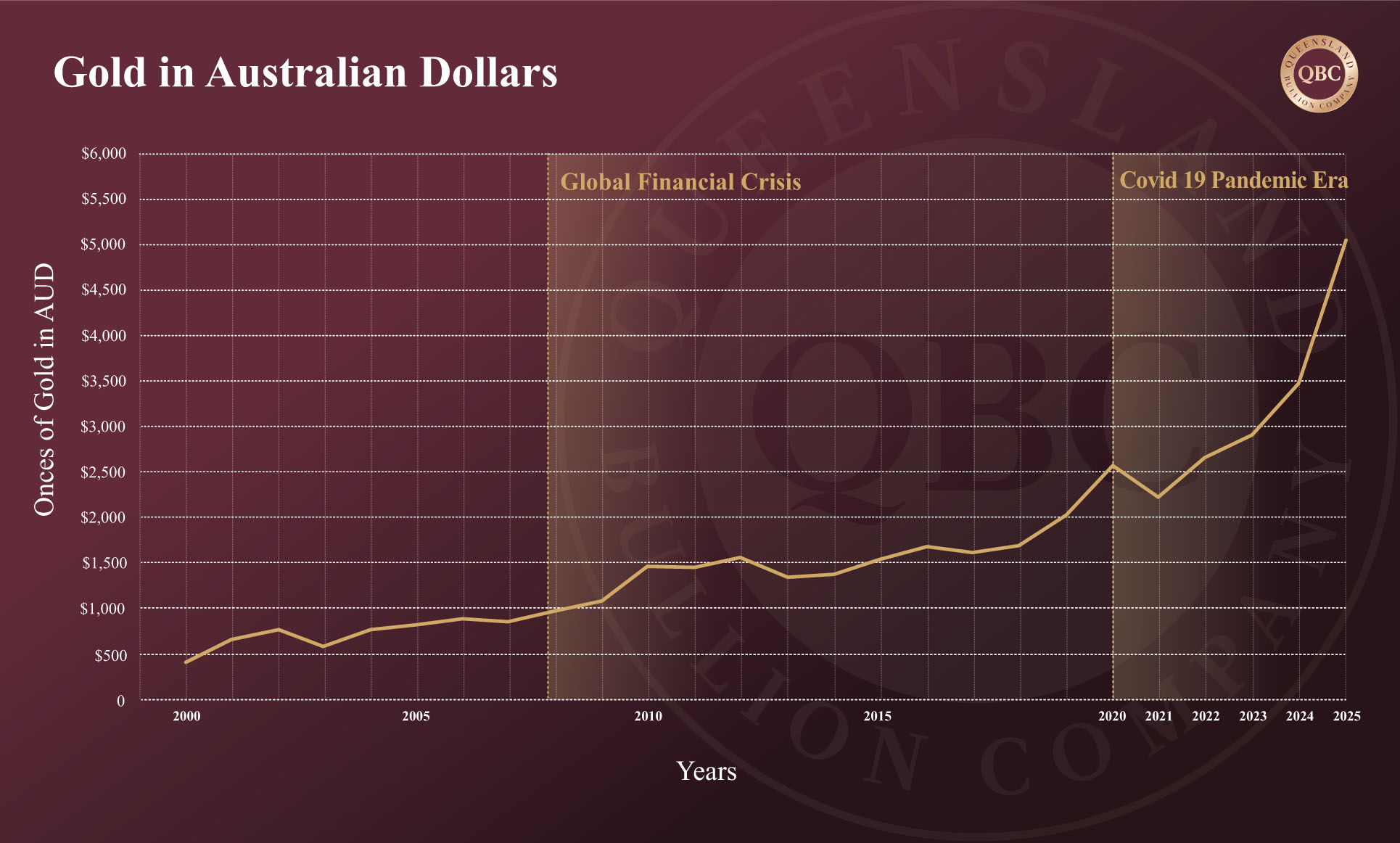

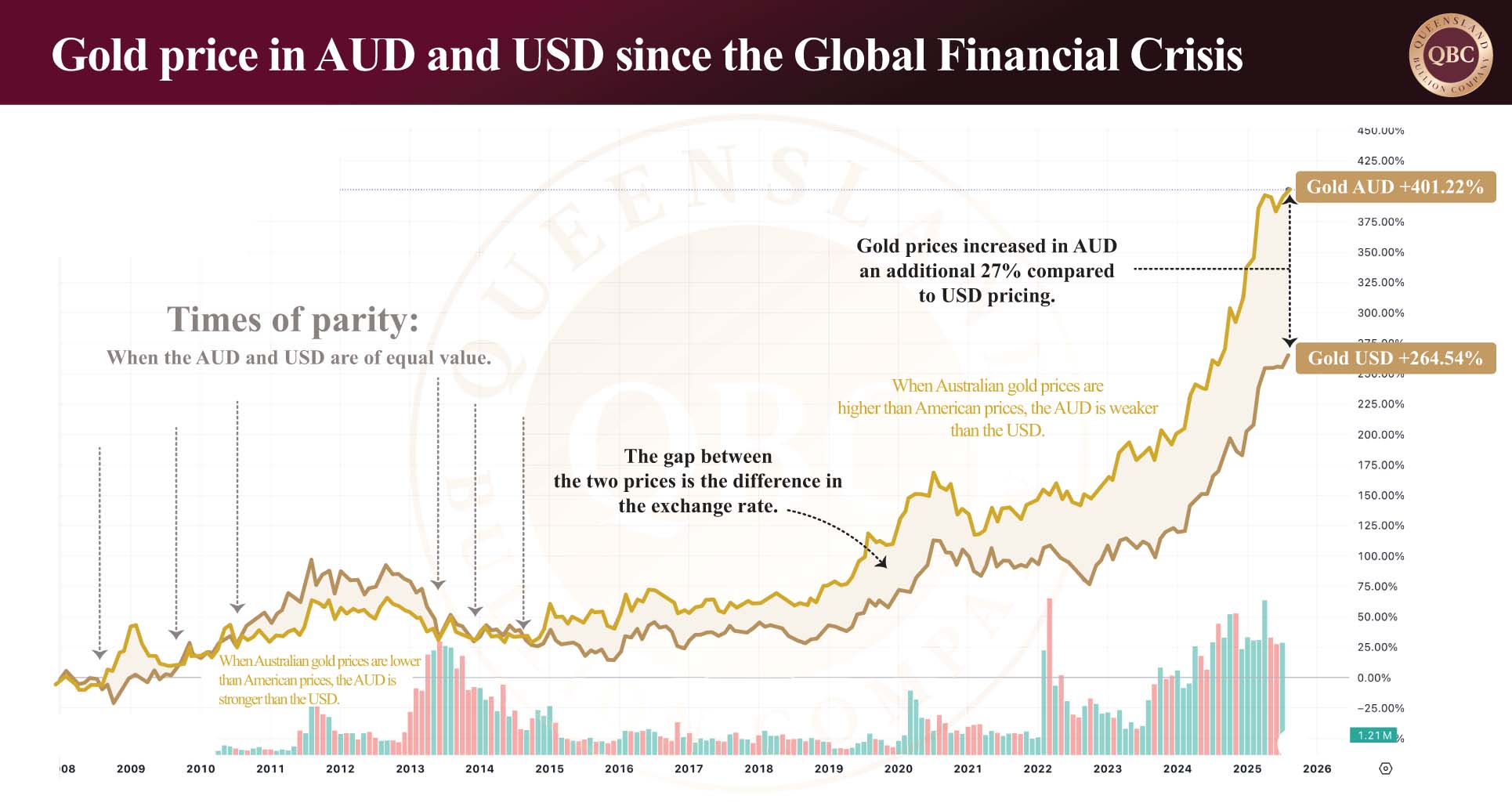

A week ago, gold surpassed the psychologically important milestone of USD $4,000 per ounce, reaching an intraday high of USD $4,218 yesterday. It currently trades at AUD $6,476. Platinum also achieved a new all-time intraday high of USD $1,686 last Thursday, now trading at AUD $2,604. Yet the real highlight lies with silver, which has climbed more than AUD $10 since the start of October — a remarkable gain of over 19%, rising from intraday prices of AUD $69.85 to AUD $83.14 in just fifteen days. In America it surpassed all-time highs and broke USD $50 six days ago, continuing with strong upward momentum.

Such rapid movement underscores a shifting dynamic in global precious metal markets. Silver’s dual identity as both a precious and industrial metal positions it uniquely within this environment. While demand remains structurally strong, growing delays in the physical bullion are have emerged in the Australian market. Together, these elements define the current state of silver, one of rising appetite and mounting logistical pressure.

The global state of demand

Global silver markets are undergoing a multi-year transformation. In 2024, total silver demand fell by 3%, shaped by competing forces across the investment and industrial sectors. Silverware consumption recorded a modest 2% decline, while investment in cast bars and coins dropped by 22% — the lowest level in five years — led by a sharp 46% fall in the United States. According to the Silver Institute, this pullback in investor demand reflects profit-taking at higher prices, market saturation, and reaction to President Trump’s election.

In contrast, industrial demand rose 7% to reach 700 million ounces, accounting for 59% of total global consumption in 2025. Certain industrial segments have become clear leaders: photovoltaic demand for solar panels has quadrupled since 2015, with the Silver Institute forecasting a further 20% increase this year. Electronics has maintained steady growth of around 5–7% annually since 2021, while electric vehicles and the broader automotive sector continue to expand at approximately 10% per year. Jewellery fabrication also climbed 3%, largely driven by renewed demand in India.

Below is a graph of global silver coin and cast bar demand since 2015, a reflection more of retail investment as opposed to industrial consumption. The fall in demand since 2022 can mainly be attributed to profit taking, tighter household budgets (or weaker retail sentiment), and preference shifting towards the “paper” silver market.

The global state of supply

The physical deficit in silver now totals nearly 800 million ounces since 2021. This gap shows little short-term relief to any supply concerns. Global silver mine production has declined 7% since 2016. Global mine production is expected to peak in 2026 before beginning to decline as several major projects reach end-of-life (mainly in Mexico). In developed nations new mining projects typically require five to eight years to progress from discovery to production. And with roughly 72% of silver sourced as a byproduct of other metals, supply cannot easily respond to rising demand. Recycling will offer limited relief, while refined output faces increasing costs and environmental constraints.

However, persistent global supply deficits remain a defining feature of the market stretching over the past four years, with 2025 expected to mark the fifth. The net result is a tightening market, where physical availability continues to contract even as industrial and investor interest builds. In 2025 demand clearly still exceeds supply — leaving the market in a sustained structural deficit. Yet history shows that each major silver deficit has ultimately set the stage for stronger prices, as physical inventories tighten and market confidence erodes.

Demand in Australia

Silver demand in Australia continues to accelerate as an extraordinary squeeze on silver plays out across the country. The Perth Mint is West Australia’s government owned refinery and the only establishment that publishes sales figures. The refinery saw minted silver products total 578,588 troy ounces in September 2025 — a 36% increase from August and the highest monthly figure since April. It is estimated that the increase could be between 40-60% or even higher for bullion merchants in the private sector.

The Perth Mint’s total silver bullion sales (minted plus cast bars) reached 721,338 troy ounces in September — a 28% increase from August. This surge highlights the renewed strength of the local silver market and a growing concern about the state of the global financial landscape, fiat currency and confidence in our bureaucrats.

Supply in Australia

Access to physical silver has significantly tightened across Australian retail markets in October. This is not due to a lack of raw supply, but rather production bottlenecks in refining and bar manufacturing. With demand roughly double what it was at this time last year, refineries producing branded cast bars are facing increasing pressure. Lead times for delivery have doubled, and further delays are inevitable if the current pace of buying continues. Now the cost of sourcing both gold and silver is creeping up for refineries as the run on metals deepens further into the supply chain; this will ultimately affect the retail price of both metals sooner rather than later.

While supply constraints are currently logistical rather than structural, they point to a growing imbalance between immediate demand and fabrication capacity — a pattern often seen in the early stages of sustained bull markets.

In summary

Silver investment in 2025 has been defined by a clash of forces: strong investor appetite and constrained supply on one side, and a changing global economy on the other. The metal’s unique dual role for both industrial use and as a safe-haven asset continues to shape its volatility. Trade tensions, equity market corrections, and ongoing geopolitical risks all add to its appeal as a portfolio diversifier.

Expected US interest rate cuts and elevated uncertainty should continue to support silver’s momentum through year-end. With the gold-to-silver ratio still historically high, many investors see further upside potential. However, as access to physical bullion begins to slow, the issue of delay becomes as relevant as demand. Having a good relationship with your bullion dealer has never been more important.

For Australian investors, the message is clear: silver’s strength is being matched by growing lead times. Securing positions now, while supply remains available and delays are still manageable, could prove a prudent step in an increasingly constrained market.