The escalation of conflict in the Middle East has once again placed global markets on high alert. What began as rising tensions between Israel and Iran has quickly evolved into a broader regional war involving multiple state and non-state actors. Traditionally, such geopolitical instability sends investors rushing toward safe-haven assets like gold and silver. Yet the latest market reaction has been more complex than expected.

At the time of writing, gold trades around AUD $7,269 per ounce, silver sits near AUD $118, and platinum has also experienced downward pressure in recent sessions currently at AUD $3066. While precious metals initially surged when the war erupted, price action has since diverged. Gold has largely moved sideways, while silver and platinum have declined from their conflict-driven highs. To understand this unusual behaviour, investors must look beyond the battlefield itself and examine the wider forces shaping markets, particularly oil prices, inflation expectations, and global monetary policy.

The war expands

The current crisis has rapidly grown into a multi-front regional conflict involving the United States, Israel, Iran, Hezbollah in Lebanon, and several Gulf states that host American military bases and assets. President Donald Trump has suggested the war could last five weeks or longer, raising concerns about broader regional destabilisation.

Israeli officials have described the military campaign as a “broad and joint operation to thoroughly degrade the Iranian terrorist regime and remove existential threats to Israel over time,” noting that the current escalation follows months of close strategic coordination between themselves and America. Western allies have begun to participate in varying capacities. France has entered the war in what it describes as a strictly defensive role, deploying naval and air assets to the region. The United Kingdom has also positioned forces in Cyprus and reportedly intercepted drones over Jordan as tensions intensify.

Civilian safety concerns are escalating alongside military operations. On March 2, the U.S. State Department advised American citizens to “depart immediately” from fourteen Middle Eastern countries, including Bahrain, Egypt, Iran, Iraq, Israel, the West Bank, Gaza, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, the United Arab Emirates and Yemen. Similar warnings have been issued by allied governments. More than 100,000 Australians are currently in the Middle East, and the Australian government has advised citizens to avoid travel to key transit hubs such as Qatar and the UAE.

Public opinion remains deeply divided. Public opinion in America indicates that only 25% of respondents support the U.S.–Israeli attacks on Iran, highlighting the controversial nature of the expanding war.

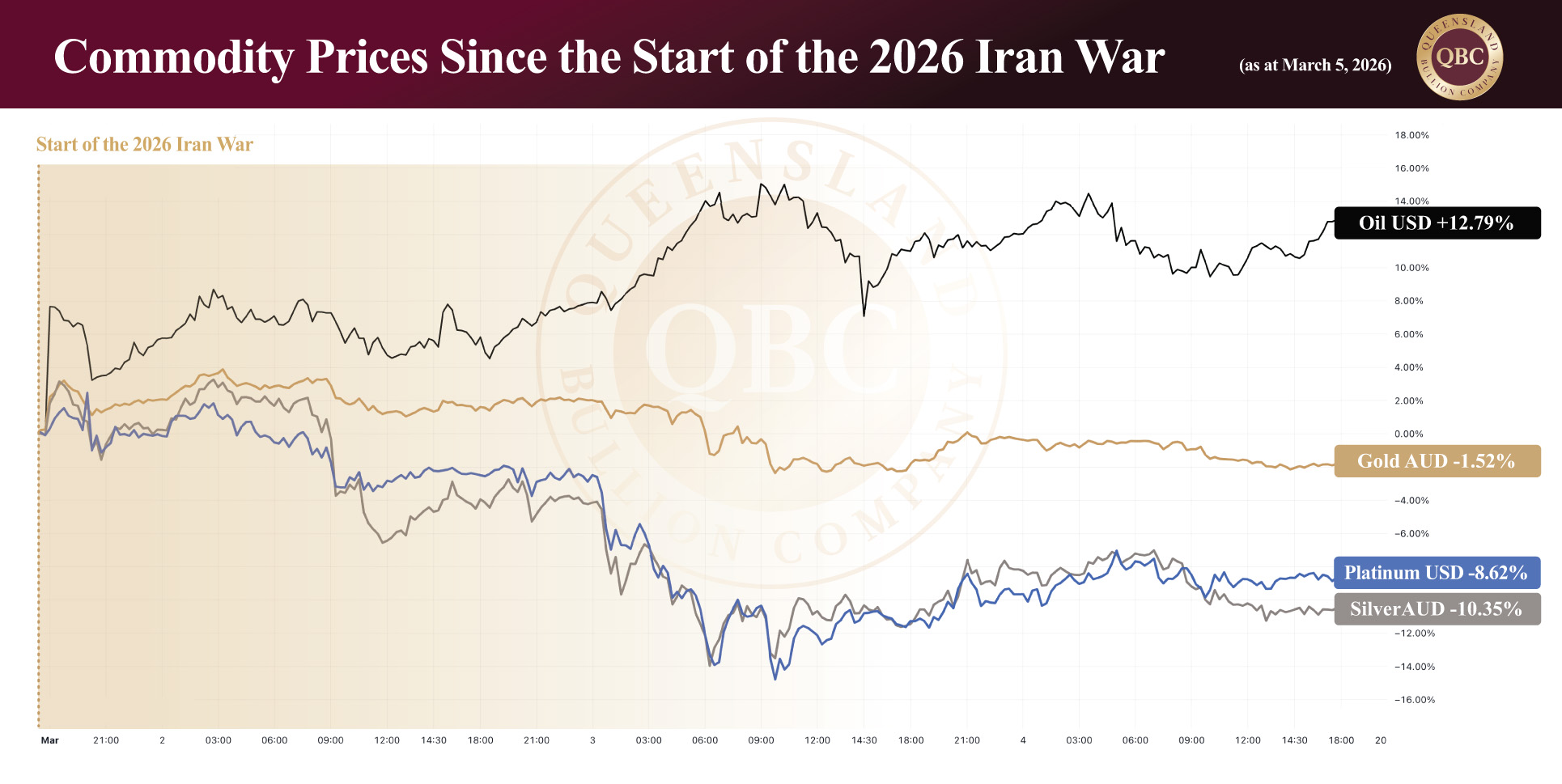

Oil, inflation and the precious metals puzzle

One of the most immediate economic consequences of the conflict has been disruption to global energy markets. The Strait of Hormuz, one of the world’s most critical energy chokepoints, has become a focal point of concern. Iranian Revolutionary Guard forces reportedly warned vessels that passage through the strait was prohibited, effectively threatening a key artery for global energy trade.

Approximately 20% of global oil supply and roughly $500 billion worth of energy shipments pass through the Strait of Hormuz each year. The waterway also handles shipments of chemicals and fertilisers, meaning prolonged disruption could ripple through agriculture and food supply chains worldwide. Following the initial attacks, oil prices surged from USD $70.51 to USD $76.07, a 7.8% increase since the start of the conflict. Analysts warn that if the war significantly disrupts supply, crude oil could rise toward USD $100 per barrel, potentially adding 0.6–0.7 percentage points to global inflation. How this translates to the cost of living is that there could be a significant inflationary increase between 20 and 30%.

Higher oil prices have important implications for monetary policy, particularly in the United States. The Federal Reserve operates under a dual mandate: maintaining price stability and promoting maximum employment. Inflation currently sits slightly above target at 2.68%, while the Federal Open Market Committee (FOMC) has maintained the federal funds rate between 3.5% and 3.75% in an effort to curb inflation.

If rising oil prices push inflation higher, the Fed may respond by tightening monetary policy or maintaining higher interest rates for longer. When interest rates rise, U.S. Treasury yields become more attractive to investors, drawing capital into bond markets and strengthening the U.S. dollar. Both Treasuries and the dollar are also considered safe-haven assets, meaning that during periods of geopolitical stress, capital can flow into these assets instead of precious metals.

This dynamic helps explain the recent market behaviour. Rather than seeing a broad surge in commodity pricing, investors have split capital across multiple safe havens: Treasury bonds, the U.S. dollar, and precious metals. Because gold does not produce a yield, stronger bond returns can temporarily reduce its appeal. Meanwhile silver has a significant industrial component, meaning concerns about slower global growth (potentially triggered by higher energy costs) can weigh on its price in the short term.

In summary

The muted reaction in precious metals despite escalating geopolitical tensions highlights the complexity of modern markets. In the short term, the lack of a dramatic surge in gold and silver suggests two factors could be playing out. Firstly, investors may have already priced in a significant degree of geopolitical risk before the conflict escalated. Secondly, markets may be assuming the confrontation will remain limited in duration compared to previous large-scale regime-change conflicts; however, wars based on regime change have not historically lasted weeks as anticipated by the American government, rather it usually takes years (the Iraq War being case in point).

Over the longer term, the broader outlook for precious metals remains strong. The underlying drivers (persistent geopolitical instability, structural debt pressures, ongoing inflation risks, and silver supply deficit) have not disappeared. If the conflict deepens or begins to threaten global energy supply more severely (especially if it takes more time than anticipated), markets may rapidly reassess their positioning. If it does last longer, military application of silver will no doubt put upward pressure on pricing as both sides look to accumulate sufficient supply to achieve their military goals. In that scenario, gold and silver could once again move sharply higher as investors seek protection against both geopolitical and economic uncertainty.