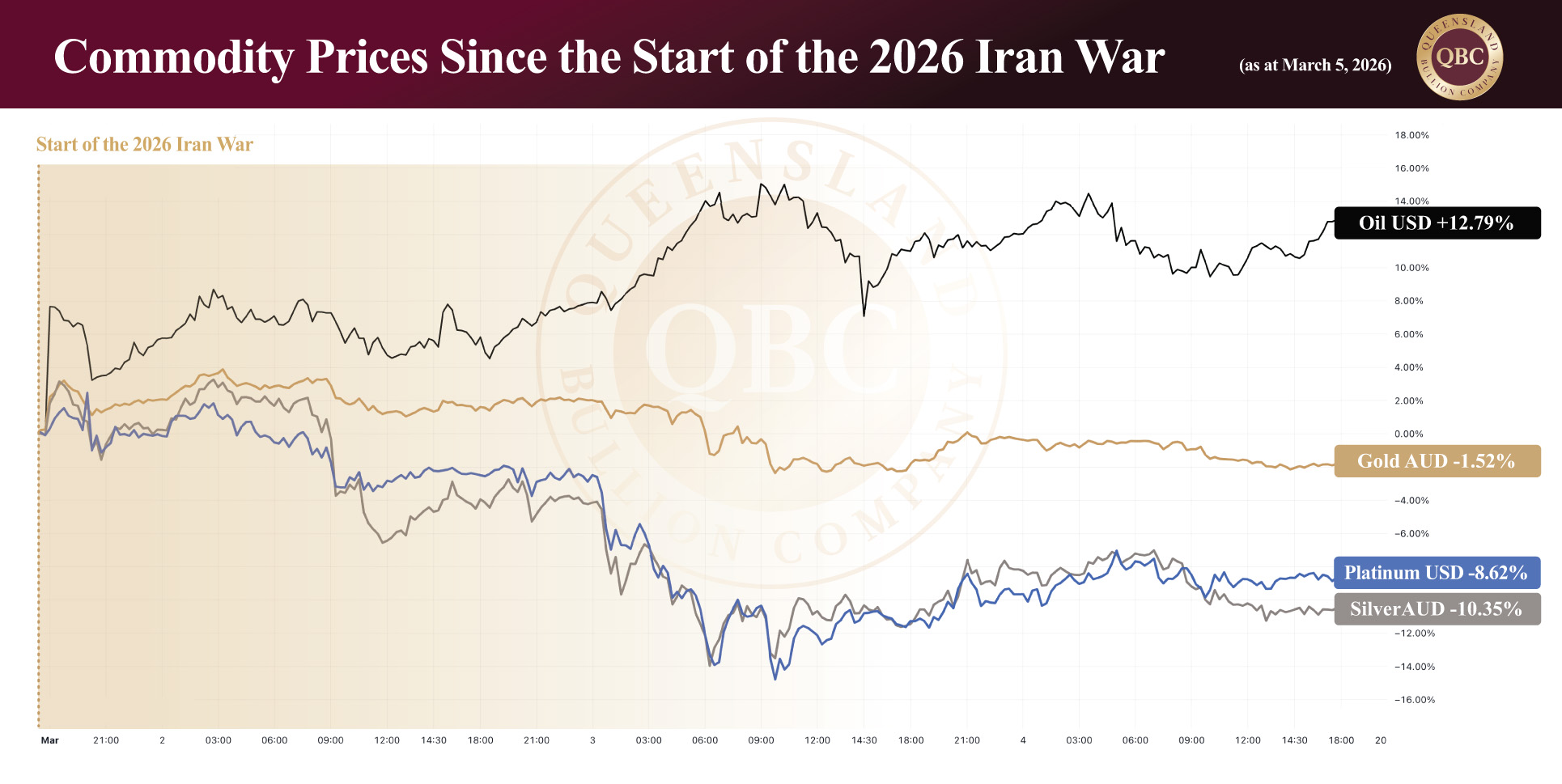

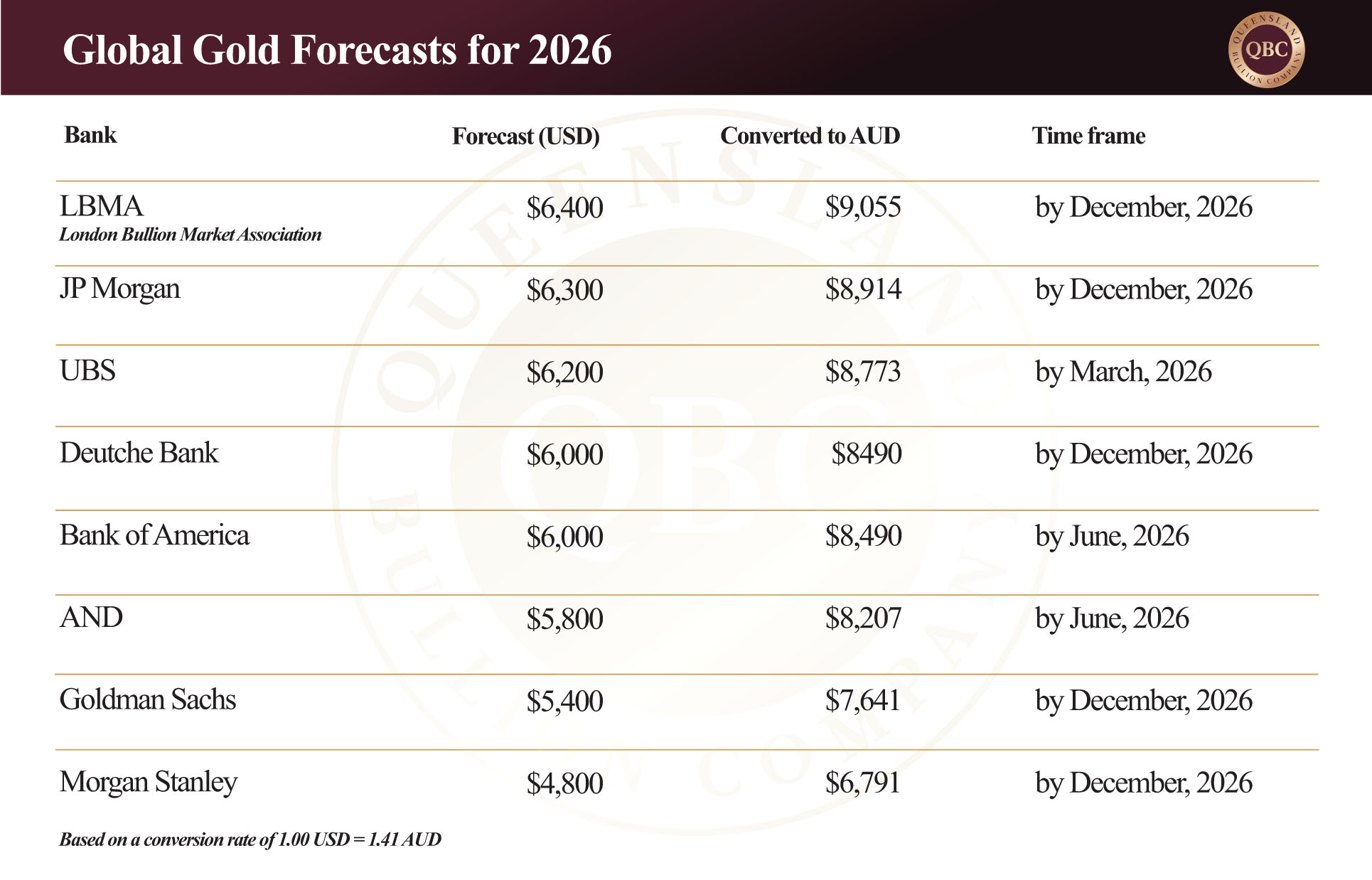

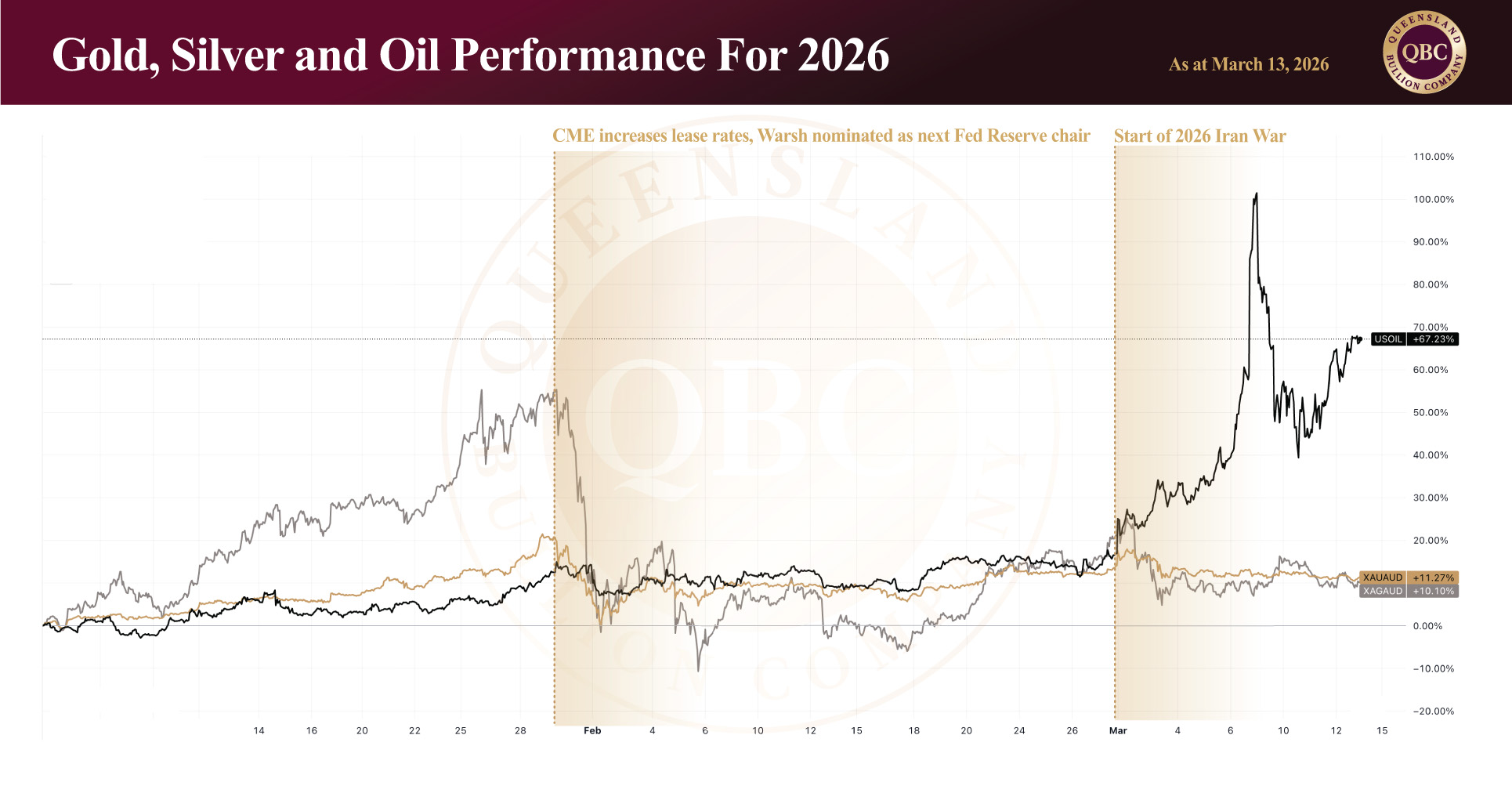

Since the outbreak of the 2026 Iran War, precious metals markets have behaved in a way that has surprised many observers. Rather than surging dramatically on geopolitical risk, gold and silver have largely traded sideways, with only brief spikes followed by consolidation. At the time of writing, gold trades around AUD $7,226 per ounce, silver sits near AUD $119.20, and platinum around AUD $3019.88.

This muted response has sparked a wave of explanations across financial media. Many commentators have pointed to oil prices, inflation expectations and the prospect of Federal Reserve rate cuts as the key drivers of precious metals demand. Yet when examined closely, these explanations fail to fully account for the market’s behaviour. To understand what is actually happening, investors must look at three interconnected forces shaping the current environment: interest rate expectations, inflation dynamics, and the unfolding reality of the conflict itself.

The Market Reaction: A Narrative That Doesn’t Quite Fit

Last week we explored the possibility of high oil prices increasing inflation over time and thus pushing the U.S. federal funds rate higher. This week the market entertains different ideas. The explanation circulating most widely in financial media centres is a simple idea: cooling oil prices reduce inflation fears, which in turn increases expectations for Federal Reserve rate cuts and creates a more dovish policy outlook. Under this framework, investors would naturally rotate into precious metals as monetary conditions loosen.

It is a tidy narrative. It also does not hold up under scrutiny.

A look at the CME FedWatch tool (the instrument traders use to price interest rate expectations in real time) tells a very different story. The probability of the Federal Reserve holding rates steady at next week’s FOMC meeting currently sits at 99.4%. That meeting is only days away.

More revealing than the number itself is the trajectory behind it. A month ago, markets were already assigning roughly 80% probability to no change in policy, meaning the outcome has been widely anticipated for weeks. Rather than softening as the meeting approaches (which the rate-cut narrative would require) expectations have only hardened. The probability of a rate cut has significantly reduced and now sits at around one-fifth of where it was a week ago.

In other words, the Federal Reserve is not moving, and markets know it. The metals market knew it as well and precious metals held its ground. That alone suggests the mainstream explanation is incomplete.

Inflation, Oil and the Real Yield Equation

While the market is focused on oil prices and inflation data, the key issue for investors is not simply whether inflation rises or falls, but how it compares to available yields. In the current environment, the Federal Reserve is expected to maintain its policy stance, leaving bond yields relatively stable while inflation risks remain tied to developments in global energy markets.

What ultimately matters for capital allocation is the relationship between inflation and those yields. Investors measure returns in real terms, the difference between the income provided by bonds and the erosion of purchasing power caused by inflation. If yields exceed inflation, Treasury bonds tend to attract capital. If inflation rises above those yields, assets that preserve purchasing power, such as gold typically hold more appeal.

Markets are therefore attempting to price several competing forces simultaneously: the possibility of inflationary pressure from oil, a Federal Reserve that appears unwilling to move rates in the near term, and geopolitical uncertainty surrounding the conflict in the Middle East. The result is a delicate equilibrium in which safe-haven flows are divided between U.S. Treasury bonds, the U.S. dollar, and precious metals, rather than concentrating in any single asset class.

Reality on the Ground

While financial markets appear to be pricing in a relatively short conflict between U.S.–Israeli forces and Iran, developments on the ground suggest a far more fluid situation.

President Donald Trump stated earlier in the week that the United States and Israel were making significant progress in the war and that the conflict could end “very soon,” comments that temporarily eased energy markets and moderated oil prices. Yet within hours, the administration’s messaging shifted. Defence Secretary Pete Hegseth indicated that the next wave of strikes would be the most intense bombing campaign yet, suggesting the conflict could expand before any resolution emerges.

As the second week draws to a close, the Western public has been told that the military campaign has already struck nearly 2,000 targets inside Iran since operations began on February 28. Iranian officials have made it clear that Tehran — not Washington — will determine when hostilities end. And Iran’s foreign minister has dismissed any immediate return to diplomatic negotiations.

The conflict’s economic consequences are also beginning to spread. Iran has declared the Strait of Hormuz closed, a move that threatens one of the most critical chokepoints in global energy trade. The disruption has already forced Iraq to curtail production and led Saudi Arabia’s largest refinery to suspend operations. Recently two oil tankers carrying Iraqi oil have been attacked with one dead and both tankers ablaze. Additionally, three merchant ships have been struck with a Thai registered bulk carrier sustaining significant damage with crew rescued by the Omani Navy.

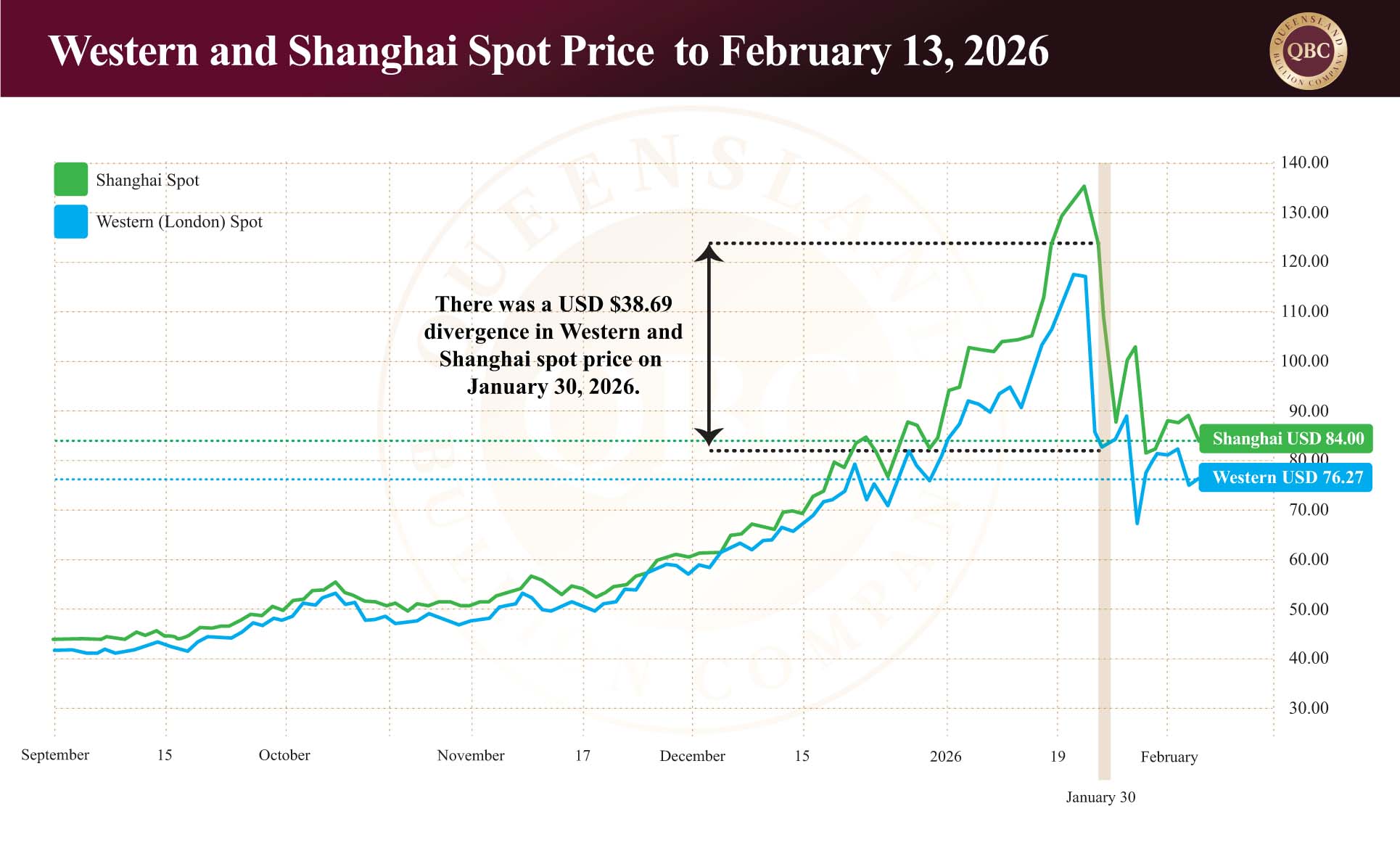

Even brief interruptions in the Strait of Hormuz can send shockwaves through energy markets. Despite a temporary pullback in oil prices earlier this week, the broader supply shock remains unresolved. In that context, the brief dip in gold and silver attributed to dollar strength was quickly absorbed by the market.

In Summary

Financial markets currently appear to be operating under one central assumption: the conflict will be short-lived. Asset prices, including gold, silver and oil, reflect this expectation.

Yet history suggests that wars rarely unfold according to early forecasts.

The last major regime-change operation conducted by the United States was in Iraq which began in March 2003 and lasted nearly nine years, concluding only in December 2011. More recently, Russia announced in February 2024 that its “Special Military Operation” in Ukraine would last ten days. Two years later, the conflict remains ongoing.

If the Iran conflict resolves quickly as President Trump suggests, markets may remain relatively stable. Risk-on sentiment would strengthen, oil prices could retreat, and precious metals might consolidate further after their recent advances.

But if the conflict continues or expands the current market assumptions may prove incorrect. In that case, volatility could increase sharply. Risk-off sentiment would return, and safe-haven demand for gold and silver could reassert itself.

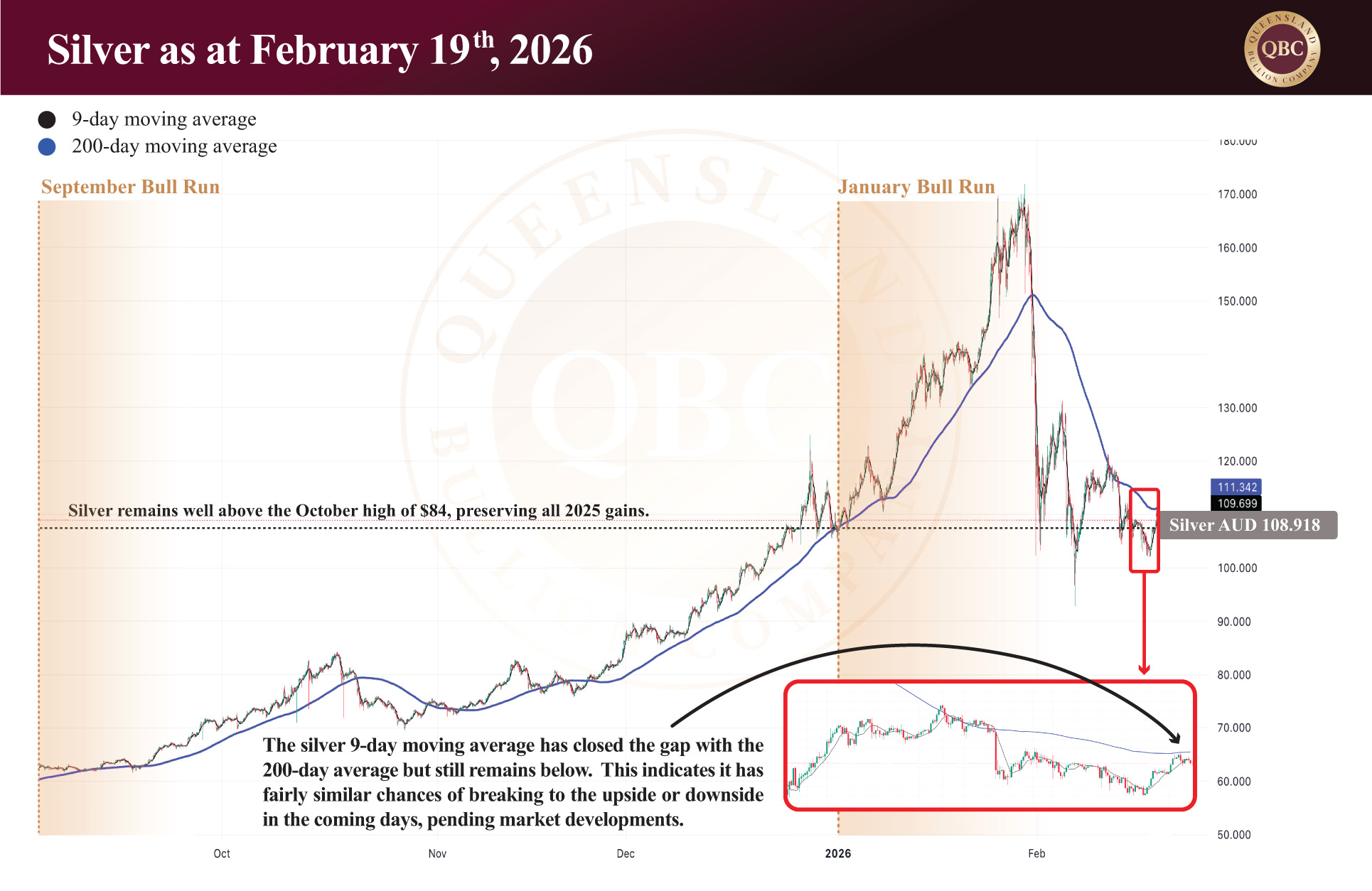

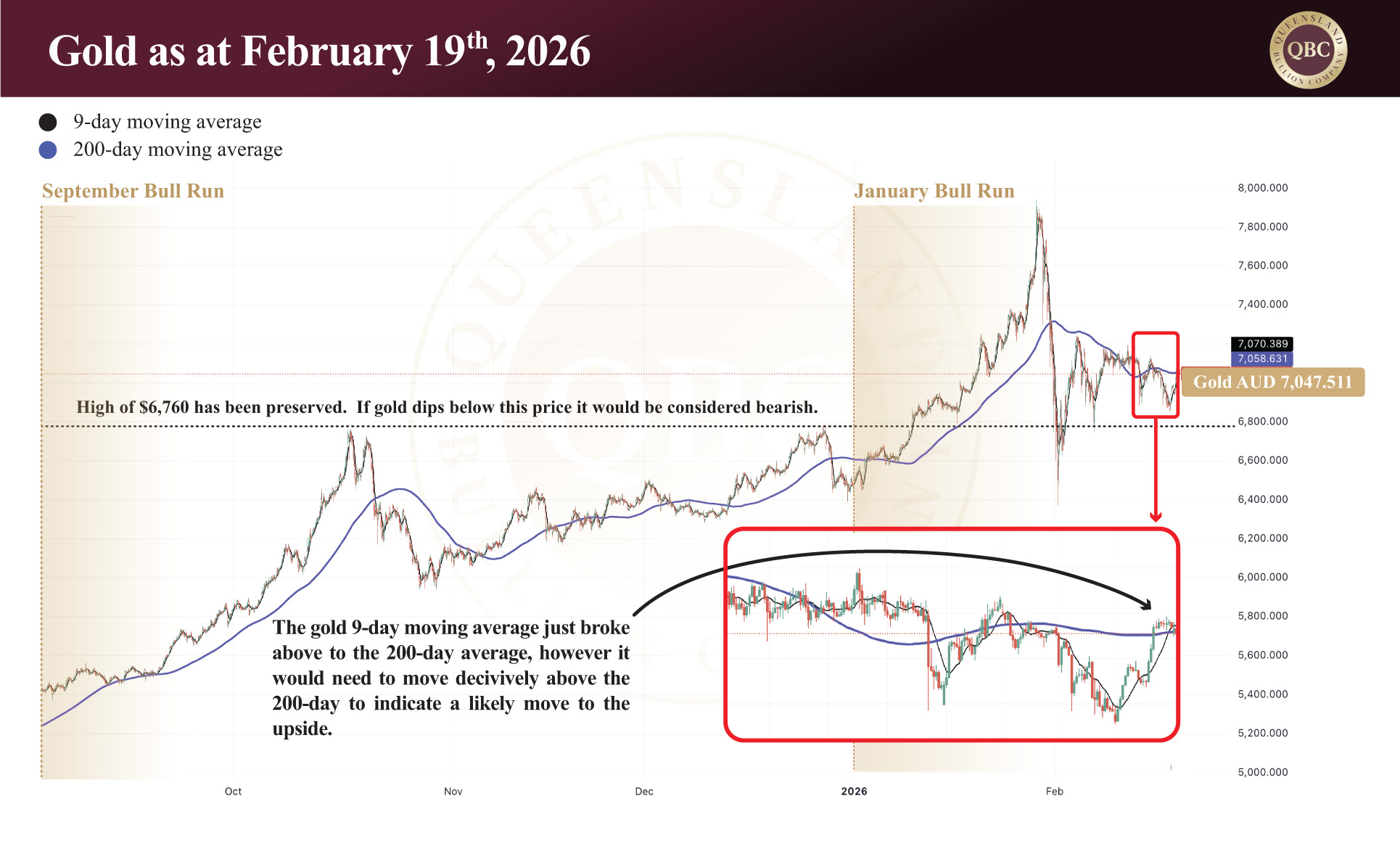

Current geopolitical risk has followed historical corrections in the metals markets. Since the highs in January, gold dropped 17.5% and silver 42% in less than a week. Since then they have both made progress in recovering with gold reducing this pull back to just 8.5% and silver to 29%. Periods like this often test market consensus. Investors tend to position themselves according to what they believe will happen next. Yet history repeatedly shows that major market shifts occur when those expectations turn out to be wrong. If that moment arrives again, precious metals may once again move rapidly as investors reassess the true scale of geopolitical risk.