Five Macro Catalysts to Watch in 2025

by Evie Soemardi

Since the United States first flagged sweeping tariff measures in April, markets have struggled to adjust positions across asset classes in real time. As we move into the second half of 2025, several macroeconomic and geopolitical forces remain in focus. These catalysts are already shaping investor sentiment and asset valuations across global markets. With gold currently trading at AUD $5,068.79, silver at AUD $57.90, and platinum at AUD $2,160.07, here are five critical forces that could influence market direction in the months ahead.

1. Central Banks Hold Their Nerve—for Now

Both the Reserve Bank of Australia and the U.S. Federal Reserve have resisted pressure to aggressively cut rates thus far. The Fed has held its benchmark rate steady at 4.38% across the last seven meetings, and the RBA has only made a single 25 basis point cut in the last five. With inflation easing but not defeated and new tariff measures from the U.S. still unfolding, central banks appear to be in cautious observation mode.

Australia’s fiscal position is notably more sound than that of the U.S. from a debt to GDP perspective; however, one key distinction remains: America continues to hold its gold reserves on its balance sheet at a nominal USD $42.22 per ounce (requiring legislative changes to revalue it). A simple revaluation would materially improve its financial position overnight—something Australia, which revalues gold annually at market prices, cannot mirror. As global growth continues to stall, unconventional options like these will become increasingly compelling. Read more about the Fed’s position here.

2. Persistent Inflation and the Stagflation Threat

Despite modest growth in some sectors, inflation remains sticky. A combination of sluggish GDP growth and sustained inflation has raised the spectre of stagflation—a damaging economic mix reminiscent of the 1970s.

In such an environment, monetary tools become blunt instruments. Raise rates and nations risk contraction and job losses; cut rates and another inflationary wave may be unleashed. Business margins shrink, household confidence deteriorates, and capital seeks refuge in assets uncorrelated to fiat—namely, precious metals.

3. A Weakening U.S. Dollar and Diminished Global Trust

The U.S. dollar has lost over 10% of its value in 2025 with the dollar index falling sharply amid ballooning fiscal deficits and lower demand for Treasuries. New tax cuts have added trillions to the projected deficit, while foreign central banks are quietly trimming their exposure to U.S. debt.

Meanwhile, the BRICS alliance continues its push toward dedollarisation, accelerating the erosion of confidence in the Greenback as the global reserve. However, USD’s status as a safe haven is yet to be tested in a significant way. For Australians, a weaker USD lifts metal prices locally—on the contrary a softer Australian dollar against the USD has the opposite effect. And the strength of our local currency is very much dependant on international growth, natural resources and ultimately China.

4. Central Bank Gold Buying Reshapes the Market

In just the first quarter of 2025, central banks purchased 244 tonnes of gold—25% higher than the five-year quarterly average. This follows three straight years of net gold buying above 1,000 tonnes. Our previous article has already covered that 60% of reserve banks are accruing gold for the purposes of diversification (aka dedollarisation or “monetary neutrality” for the BRICS nations). Then they cite protection against geopolitical risk, and then as a hedge against inflation.

Central banks, unlike retail investors, are usually price-insensitive—they are more concerned with strategic allocation than entry level pricing. Their demand builds a strong price floor for gold and has become one of the clearest bullish fundamentals in the market.

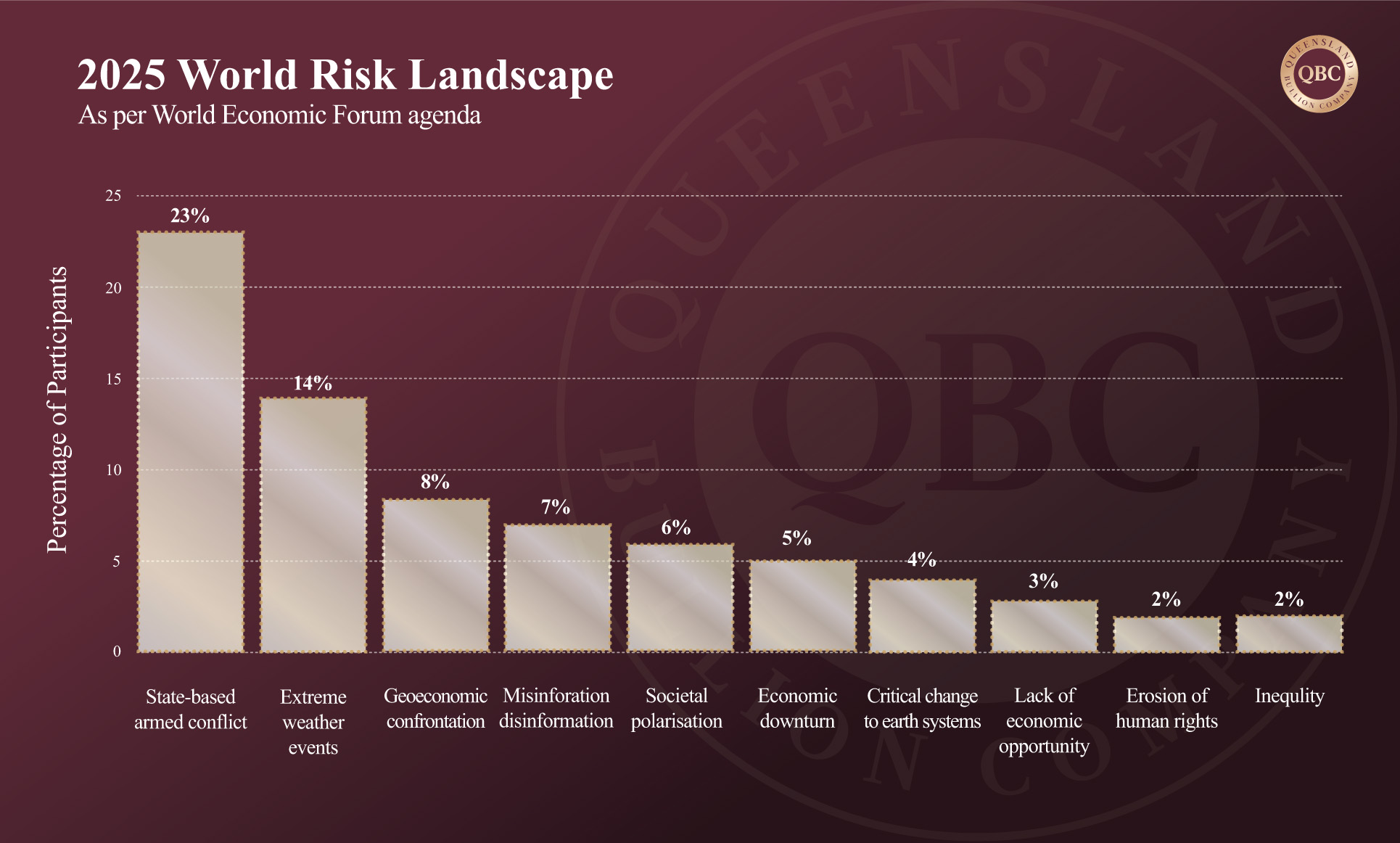

5. Geopolitical Risk as the Wildcard

Geopolitical risks remain elevated in 2025, with ongoing conflicts and trade disputes posing threats to global economic stability. The World Economic Forum’s Global Risks Report highlights state-based armed conflicts as the top risk for the year, emphasising the potential for significant disruptions in trade and financial markets.

Such tensions can lead to increased market volatility and impact investor confidence worldwide. But investors in the precious metals market are familiar with why gold and silver are considered safe haven assets in times of uncertainty and prepare accordingly.

Positioning for What Comes Next

For investors who hesitate at current price levels, a prudent and diversified physical metals strategy is key. The following multi-pronged approach to take advantage of the above fundamentals could include:

Dollar-cost average

Experienced investors know it is more important to accumulate according to financial capacity rather than trying to time the market to secure best prices. Dollar-cost averaging—strategically buying during price dips—can help reduce the average cost per ounce, offsetting earlier purchases made at higher prices. This can be an effective strategy if the market allows.

Prioritise insured storage

While securing bullion is a matter of preference, as prices rise risk tolerances can be eventually tested. Geographic diversification of storage can minimise risk. For example, you may be comfortable holding 100% of your holdings in a safe a home, but when it doubles in value you may prefer to move 50% of it to a private vaulting facility.

Favour physical over paper positions

“If you don’t hold it, you don’t own it” is certainly conservative, but when applied to the gold and silver paper futures markets it is on point. The leverage on gold but especially silver paper contracts is eyewatering equating to millions of dollars’ worth of bullion with multiple claims against it. The number of paper contracts taking delivery of the physical asset has escalated since America announced its tariff policy in April. At some point, when the physical asset runs out, a very few will hold the metal and everyone else will be left holding the bag.

Conclusion

Each of these five macro catalysts is powerful on its own; together, they signal that the case for precious metals is not merely intact—it is strengthening. Whether it’s central banks, sovereign wealth funds, or retail investors—capital is clearly positioning for a world where volatility is the new normal and trust in fiat is rapidly being repriced.

In uncertain times, nothing is more certain than tangible assets. Gold, silver, and platinum aren’t just commodities—they are insurance against systemic fragility.