Budget Pressures and Precious Metals

by Evie Soemardi

Global markets continue to operate under mounting fiscal and structural pressure, and Australia’s 2026–27 Federal Budget has added another layer to that uncertainty. While framed around housing affordability, cost-of-living relief and economic resilience, the broader implications extend well beyond day-to-day politics. At the time of writing, gold trades at approximately AUD $6,384 per ounce, silver at AUD $109.71 and platinum at AUD $2,801.

Importantly, the budget is not directly bullish for precious metals because of any explicit policy toward bullion. Rather, it is the broader macroeconomic consequences that matter most. Expanding deficits, rising debt burdens, inflationary spending pressures, and property tax reforms all contribute to an environment in which investors increasingly reassess how and where they preserve wealth.

Structural Deficits and Rising Debt

Despite Treasury highlighting improvements in the budget position, Australia’s debt trajectory continues upward with gross federal debt already exceeding AUD $1 trillion. Large spending commitments across healthcare, defence, housing, energy transition initiatives and cost-of-living support ensure ongoing deficits and increased borrowing. Persistent deficits matter because they require continued bond issuance and reinforce concerns surrounding fiat currency purchasing power and long-term fiscal sustainability. The broader concern is not simply the size of the debt itself, but the growing dependency on debt-funded growth. Governments globally are increasingly relying on fiscal stimulus to support slowing economies, maintain employment and offset weakening private-sector activity. Over time, that creates pressure on currencies, interest rates and inflation expectations simultaneously.

Historically, these conditions have supported hard assets such as gold. This does not necessarily imply an immediate surge in precious metal prices. However, it strengthens the longer-term case for monetary metals as investors increasingly seek assets outside the traditional debt-based financial system.

Property Reforms and Capital Rotation

One of the most significant components of the budget was the proposed restructuring of investment taxation, particularly changes to the Capital Gains Tax (CGT) discount and negative gearing. Under the announced measures, from 1 July 2027 the 50% CGT discount for assets held longer than 12 months would be replaced with a cost-base indexation model alongside a new 30% minimum tax rate on real capital gains. Negative gearing deductions would also become largely restricted to new residential builds.

While the measures remain proposed rather than legislated, they are already influencing investor sentiment. Australian investors have historically concentrated heavily in residential property due to favourable tax treatment and leverage accessibility. If leveraged property becomes materially less tax-efficient, capital will inevitably begin searching for alternative stores of value. This matters because the Australian bullion market remains comparatively small relative to property and equities. Even a modest reallocation toward physical gold and silver could materially affect retail demand.

Survey data already points toward changing investor behaviour. A recent survey found that 61% of property investors would reduce exposure to the market if both the CGT and negative gearing reforms proceed. Industry modelling also suggests the combined reforms could reduce dwelling starts by tens of thousands of homes while simultaneously increasing rental pressures;

However, with average weekly rents already exceeding $700 in Brisbane, Darwin, Canberra and Perth, and approximately $800 in Sydney, the property market is more likely to gradually soften in line with broader economic cycles.

Inflation Pressures Remain Sticky

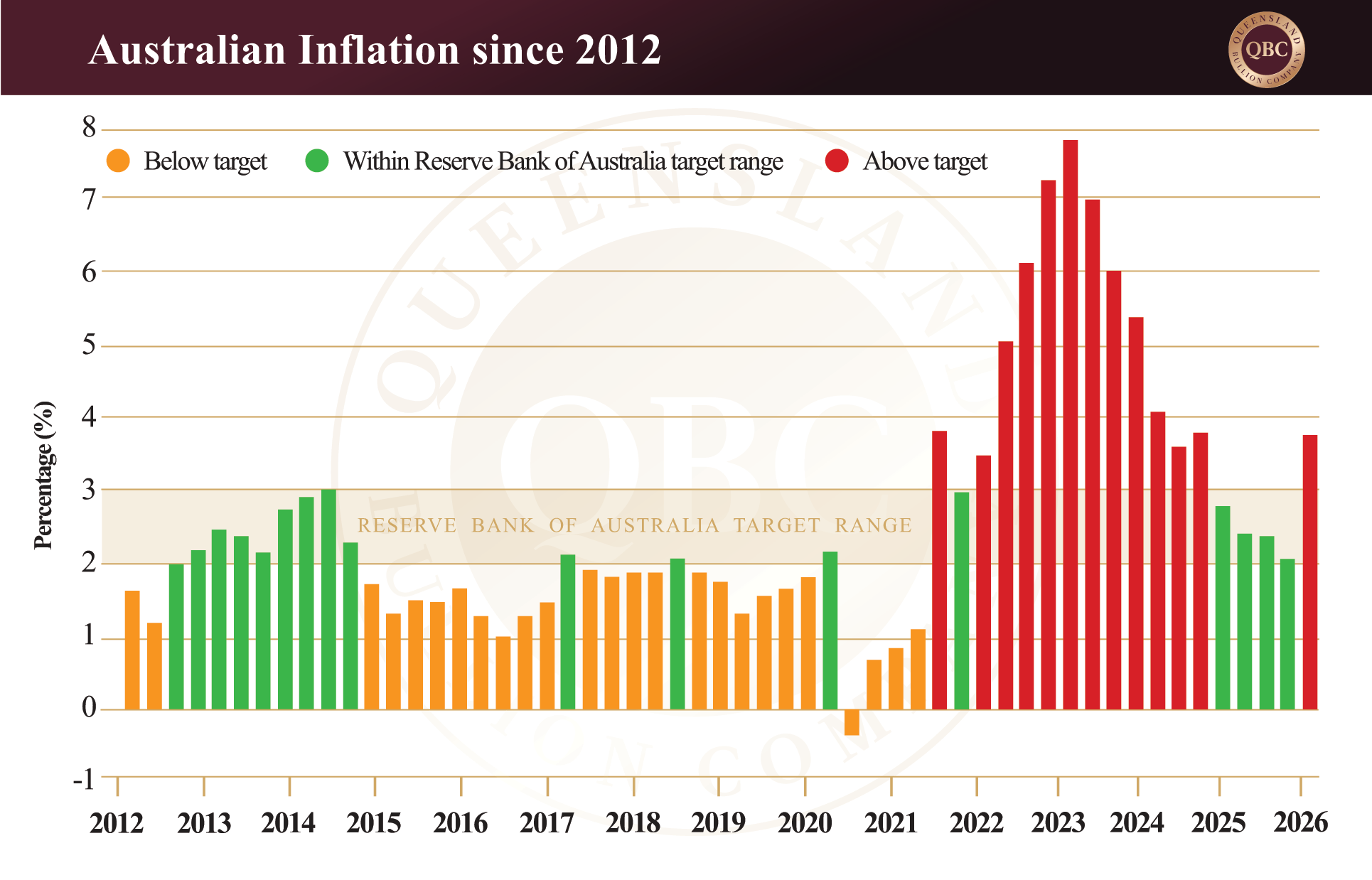

Another important implication of the budget is the ongoing risk of persistent inflation. Large-scale fiscal spending supports aggregate demand and can keep inflation elevated for longer than central banks would prefer. While inflation has moderated from the 7.8% peak reached in 2022, at 3.72% it remains above the traditional 2–3% target range. If inflation remains sticky, policymakers may be forced to maintain higher interest rates for longer. Alternatively, if economic conditions weaken materially while inflation remains elevated, central banks may eventually be pressured toward lower rates despite inflation risks. This is where real interest rates become critical.

Gold is influenced less by nominal rates themselves and more by real yields; that is, interest rates after inflation is taken into account. If inflation remains higher than bond yields, investors effectively lose purchasing power holding cash or fixed-income assets. Under those conditions, gold often becomes increasingly attractive because it preserves purchasing power over long periods.

Silver behaves somewhat differently because it carries both monetary and industrial demand characteristics. During later-stage inflationary cycles, silver can outperform gold as speculative capital enters the market alongside manufacturing demand linked to electrification and industrial production.

Trusts and Investment Structures

Beyond property itself, the budget also introduced proposed changes affecting discretionary trusts and broader investment structures. From 1 July 2028, income distributed through discretionary trusts would become subject to a minimum 30% tax rate under the announced measures. Questions also remain surrounding how the new CGT framework may interact with managed investment structures and indirectly held assets. Importantly, superannuation funds currently appear largely excluded from many of the proposed changes based on Treasury commentary so far. This may incentivise investors to increase precious metal holdings via self-managed superfunds as opposed to discretionary trusts.

Additionally, physical bullion occupies a unique position because it carries no counterparty risk. Unlike leveraged property investments, equities or managed funds, physical gold and silver are not dependent on the solvency of financial institutions or the performance of broader credit markets.

In Summary

The 2026–27 Federal Budget is not directly a “bullish bullion” policy package; however, the broader economic consequences of the measures announced are generally supportive for precious metals over the medium to long term. For decades, Australian wealth has concentrated heavily in leveraged property, equities and banking assets. But as taxation settings shift and fiscal pressures intensify, capital may gradually begin rotating toward alternative stores of value.

At the same time, the broader macroeconomic backdrop continues to favour hard assets. Real interest rates remain under pressure, sovereign debt continues expanding globally, and geopolitical fragmentation is becoming increasingly embedded within the international financial system. While short-term price movements will continue to fluctuate alongside economic data and geopolitical events, the longer-term structural drivers supporting precious metals remain firmly intact.