The Cost of War: Who Pays and What Comes Next

by Evie SoemardiWar is often measured in headlines and territory, but its true cost runs far deeper, both visible and hidden. As the U.S.-Israel-Iran war in the Middle East extends into another phase, the financial burden is beginning to surface across multiple layers of the global economy. At the time of writing, gold trades at approximately $6,560 per ounce, silver near $105.29, and platinum around $2,771. While these figures reflect recent volatility, they also sit within a broader framework shaped by rising geopolitical tension, escalating defence spending, and shifting capital flows. To understand where precious metals move next, it is essential to first understand the real cost of war, who bears it, and how those costs ripple through the global system.

A modern war machine under strain

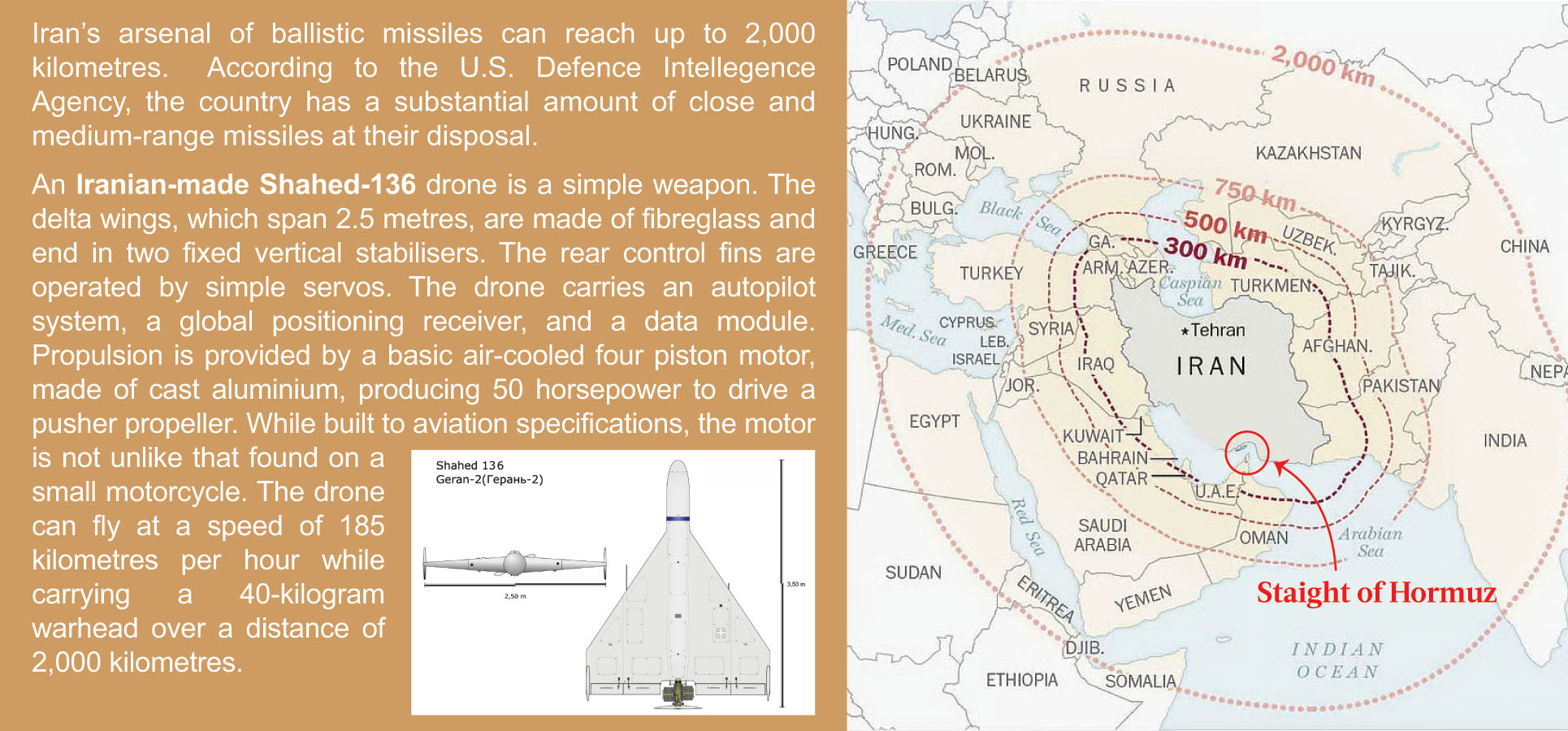

Recent developments highlight just how quickly modern conflicts consume resources. Independent discussions between major U.S. automakers Ford, General Motors and Pentagon officials signal a potential return to wartime industrial mobilisation where civilian factories pivot to produce weapon components, reminiscent of the “Arsenal of Democracy” seen during both World Wars. The fact that civilian manufacturing may need to supplement defence production underscores a key issue: existing military supply chains are already under strain. Fighting has been intense with Iran proving to be a significant foe. According to figures released by Gulf authorities earlier this week, one country faced 165 ballistic missiles and more than 500 drones in the first days of the war.

At the same time, the nature of warfare itself has shifted. Having studied the Russian’s use of Iran-supplied drones (unmanned aerial vehicles), it has employed the same drone-swarming tactics alongside missile barrages, representing a strategy designed not only to strike targets but to exhaust Western defensive systems over time. Analysts note that drones are being used to saturate air defences, force the use of expensive interceptors, and stretch protection systems across a wider geographic footprint. This is not simply a tactical evolution; it is a financial one. Iran has little choice but to fully commit to this conflict, and appears intent on demonstrating to the West that any prolonged engagement will come at a significant cost, both in operational efficiency and endurance, fiscally, as well as in firepower.

Asymmetric costs: America vs Iran

The imbalance in costs between the United States and Iran is stark. In the opening phase alone, U.S. forces deployed approximately 170 Tomahawk missiles in just 100 hours. This is three times the number that the Pentagon procured from American defence contractor, Raytheon, in the entire 2026 fiscal year. America is using their fire power far quicker than they can replace them according to Stephen Flynn, a Northeastern University national security expert. Each of these systems represents a significant financial outlay, and more importantly, a strain on replenishment capacity.

Interceptor systems further highlight this disparity. A single Patriot missile costs around USD $4 to $4.5 million, while advanced systems such as the Terminal High Altitude Area Defence (THAAD) truck mounted interceptors can reach USD $12.8 million each. Naval-based SM-3 systems range between USD $10 million and $28 million per shot. These are the tools required to defend against incoming threats, yet they are increasingly being used against vastly cheaper weapons.

By contrast, Iran’s strategy relies heavily on low-cost drones. A Shahed 136 Geran-2 drone is widely estimated in Western and Persian reports to cost between USD $20,000 and $50,000. But Iranian academics with knowledge of Iran’s defence industry place the figure realistically closer to USD $4,000. Even at the higher estimate, the cost disparity is extraordinary. It creates a scenario where defending against an attack can cost potentially 100 times more than launching it. Said another way, it costs America $4 million to defend against a single $4000 drone. This puts the defence against more than 500 drones in the opening days of the conflict into an entirely different perspective, especially since they have deployed thousands more since the start of the war. As one analyst succinctly noted, it is unsustainable to use million-dollar interceptors against low-cost aerial threats.

This imbalance is not incidental; it is a deliberate strategy employed by Iran. It is designed to stretch budgets, deplete stockpiles, and force strategic decisions based not just on military effectiveness, but financial endurance. In this environment, the cheapest weapon often becomes the most disruptive.

The expanding price tag

The financial cost of the war is escalating rapidly. Within the first week, estimates placed the total expenditure at approximately USD $12.7 billion with projections climbing as operations continue. The Pentagon has already sought an additional USD $200 billion in supplemental funding, signalling that this is not a short-term engagement.

Beyond direct military spending, the indirect costs are equally significant. Supply chains are being strained, skilled labour shortages are limiting production capacity, and energy markets are reacting to instability. Oil price movements alone have the potential to feed directly into inflation, increasing costs across transportation, manufacturing, and food production. In effect, the cost of war extends well beyond the battlefield. It becomes embedded in everyday economic activity, influencing everything from interest rates to household expenses.

Economic consequences: the public pays

Ultimately, the cost of war is not borne solely by governments but is transferred to the public. In the United States, this transfer occurs through two primary channels: inflation and economic slowdown. In addition to rising oil prices, if war-driven spending contributes to pushing inflation higher central banks will be forced to maintain or increase interest rates to contain it. Higher rates increase borrowing costs, reduce disposable income, and slow economic growth. Alternatively, if economic weakness becomes the dominant concern, rates may be lowered to stimulate activity, but at the risk of further inflation.

Either path carries a cost. Households pay through higher living expenses or reduced economic opportunity. This is the core reality of modern conflict: regardless of policy direction, the financial burden eventually flows through to the broader population.

Compounding this is the growing risk of stagflation, where inflation remains elevated while growth stagnates. In such an environment, traditional investment strategies struggle, and capital begins to seek a hedge against inflation.

Positioning for what comes next

In periods where geopolitical uncertainty intersects with economic strain, capital does not disappear, it reallocates. Investors begin to prioritise preservation over growth, shifting toward assets that are not dependent on counterparty risk or yield dynamics.

Gold and silver have historically occupied this role for a reason. They do not rely on the performance of a government, a corporation, or a financial system. They simply exist a store of value. Geopolitical events often express themselves through competing forces such as bond yields and currency strength, but this does not signal weakness in precious metals. Indeed Goldman Sachs still projects USD $5,400 and Wells Fargo has doubled down at up to USD $6,300 for gold by end of year. Importantly, if nothing else, metals remain an effective hedge against inflation, helping investors preserve purchasing power in an increasingly expensive environment.

What matters is the broader trend. Central banks continue to accumulate gold. Industrial demand for silver remains structurally strong. And as the cost of war feeds into the global economy and demand for metal, the case for holding tangible assets becomes increasingly clear.

Periods like this are rarely comfortable. Volatility tests conviction and short-term narratives dominate headlines. But history suggests that these are precisely the conditions where positioning matters most. War reshapes economies, redistributes capital, and exposes structural weaknesses. Those who recognise this early tend to focus less on timing the market and more on securing exposure to assets that endure beyond it.

In summary

The cost of war is not confined to defence budgets or military assets. It is a layered and expanding burden that touches manufacturing, energy, inflation, and ultimately the everyday economy. The asymmetry between low-cost offensive systems and high-cost defensive responses is reshaping how conflicts are fought, and more importantly, how they are funded.

For the United States, the challenge lies in sustaining a high-cost military strategy against a lower-cost adversary. For Iran, the strategy is endurance, leveraging cost efficiency to stretch its opponent over time. For the global economy, the consequence is rising uncertainty and increasing financial pressure.

In that environment, the role of precious metals becomes clearer. Not as a reaction to every headline, but as a strategic position within a system under strain. The dynamics driving this conflict are unlikely to resolve quickly. And as they continue to unfold, the question is not whether there is a cost, but who ultimately pays it.