Why has gold softened in 2026?

by Evie Soemardi

At the time of writing, gold trades at approximately AUD $6,018, having retreated significantly from the record highs reached earlier this year. Following one of the strongest annual performances in decades during 2025, the correction has understandably raised questions about whether the bull market has run its course. The short answer, according to many of the world’s largest financial institutions, is no.

Rather than signalling a structural reversal, most institutional research suggests the recent weakness reflects a combination of higher bond yields, a more hawkish Federal Reserve, profit taking following gold’s extraordinary rally, and improving investor appetite for risk assets. While these factors have weighed on prices in the short term, the longer-term outlook remains surprisingly consistent. From the World Gold Council to central banks and major investment banks, the overwhelming consensus is that gold continues to occupy an increasingly important role within the global financial system. And where gold goes, silver ( currently at AUD $89.93) and platinum (AUD $2,395) will follow.

What is the World Gold Council saying about gold?

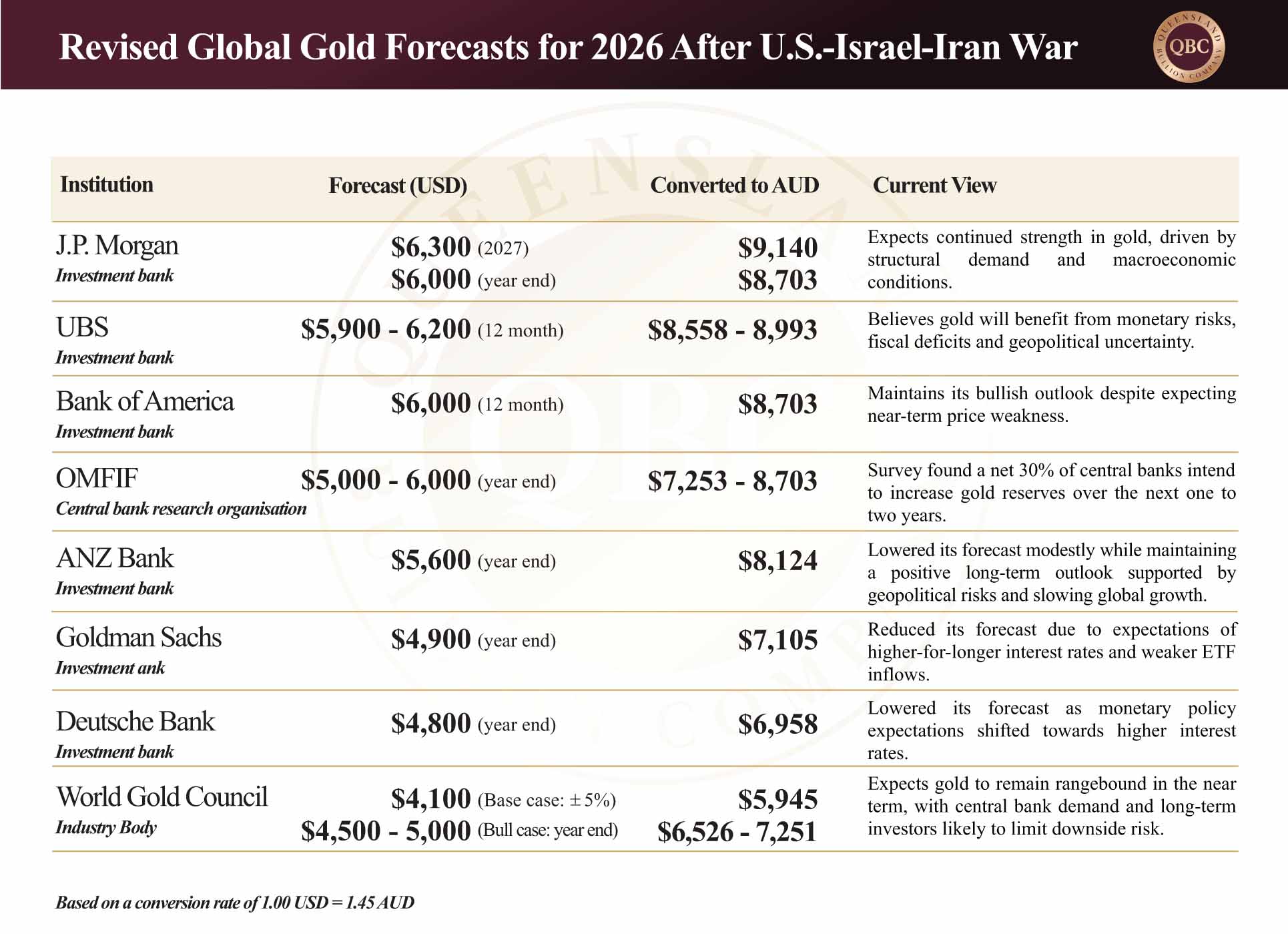

The World Gold Council (WGC) believes current prices broadly reflect today’s macroeconomic environment. Its latest mid-year outlook describes an economy characterised by moderate growth, cooling but still elevated inflation, and expectations that central banks will maintain relatively tight monetary policy. Under these conditions, the Council expects gold to remain broadly rangebound, fluctuating approximately 5% either side of USD $4,100 per ounce unless a new catalyst emerges. Importantly, the Council does not view the recent correction as unusual. Gold’s realised volatility briefly exceeded 50% during the escalation of the U.S.-Israel-Iran War before easing back below 30%. While this remains above the long-term average of approximately 17%, history suggests these periods of elevated volatility are typically temporary and tend to moderate as markets stabilise.

The report identifies three potential catalysts capable of reigniting the rally: deteriorating economic or geopolitical conditions, lower interest-rate expectations, or renewed buying from long-term investors. Under those circumstances, the WGC believes gold could recover towards USD $4,500 per ounce, with a move towards USD $5,000 possible if conditions deteriorate significantly.

On the downside, the Council acknowledges that higher bond yields, continued U.S. dollar strength and stronger investor confidence with a growing preference for risk-on assets could place further pressure on prices. Even so, it argues that declines beyond 10% to 15% from current levels would likely attract significant buying interest, limiting further downside.

Perhaps most notably, the Council highlights that much of gold’s recent buying has occurred during Asian trading hours, while many of the price declines have occurred during U.S. trading. The observation reinforces the growing influence of Asian investors and central banks in determining gold’s long-term direction.

Why are central banks still buying gold?

If the World Gold Council provides the market’s assessment, central banks provide perhaps the strongest evidence of long-term confidence. According to the WGC, official sector purchases have averaged approximately 1,000 tonnes annually since 2022. Although some central banks temporarily reduced purchases or conducted gold swaps during the first quarter of 2026, the Council expects them to remain net buyers for the year overall.

Separate research from the Official Monetary and Financial Institutions Forum (OMFIF) reinforces this trend. Surveying 74 central banks responsible for more than USD $10 trillion in reserve assets, OMFIF found that 82% currently hold physical gold, compared with 71% only a year earlier. More significantly, a net 30% intend to increase their gold holdings over the next one to two years, making gold the most sought-after reserve asset among all investment categories surveyed.

The motivations are equally revealing. Fifty-one percent of reserve managers cited geopolitical risk as a primary reason for holding gold, an increase of eleven percentage points from the previous year. Eighty-five percent identified instability in the Middle East as the greatest geopolitical threat to reserve portfolios, while 81% highlighted uncertainty surrounding U.S. foreign policy. Nearly 80% also believe the global monetary system is gradually evolving towards a more multipolar structure, increasing the appeal of reserve assets that sit outside any single country’s currency system. Interestingly, 61% of reserve managers expect gold to trade between USD $5,000 and USD $6,000 per ounce within the next twelve months, despite prices already sitting near historically elevated levels.

What are major banks forecasting for gold?

Commercial banks have become more cautious in the short term without abandoning their long-term outlook. Goldman Sachs recently reduced its year-end 2026 target from USD $5,400 to USD $4,900 per ounce, reflecting expectations that the Federal Reserve will keep interest rates elevated for longer, limiting inflows into gold-backed exchange traded funds. Deutsche Bank also lowered its fourth-quarter target from USD $6,000 to USD $4,800 per ounce for similar reasons; however, neither institution has abandoned its broader bullish view. Bank of America continues to maintain a 12-month target of USD $6,000 per ounce despite acknowledging that prices may remain under pressure in the near term. UBS expects gold to trade between USD $5,900 and USD $6,200, arguing that gold ultimately protects against the monetary consequences of conflict, including rising deficits, currency debasement and slowing economic growth rather than conflict itself. ANZ recently lowered its year-end forecast slightly to USD $5,600, while maintaining that geopolitical uncertainty and slowing global growth continue to support higher long-term prices. J.P. Morgan remains among the most optimistic, forecasting gold could reach USD $6,000 by the end of 2026 and potentially USD $6,300 during 2027.

The revisions therefore appear less like a change in conviction and more like a recognition that higher interest rates are delaying, rather than preventing, the next stage of the cycle.

Is gold still in a long-term bull market?

The current environment presents two opposing forces. On one side are higher bond yields, a resilient U.S. dollar and a Federal Reserve that continues prioritising inflation over economic stimulus. These remain genuine headwinds for gold and help explain why prices have softened after their remarkable gains throughout 2025.

On the other side sit the longer-term structural drivers. Central banks continue accumulating gold at historically elevated levels. Reserve managers remain concerned about geopolitical risk, sovereign debt and the evolution of the international monetary system. Commercial banks have trimmed their near-term forecasts, yet almost universally continue to expect substantially higher prices over the next one to two years.

The distinction is important. Short-term price movements are often driven by monetary policy and investor positioning. Longer-term trends are shaped by structural changes in the global financial system, and those changes continue to favour physical gold. Markets rarely move in a straight line. Gold is no exception. Yet beneath the day-to-day volatility, institutional demand continues to suggest that the broader investment case for physical gold remains firmly intact.