Inflation’s Unfinished Business

by Evie SoemardiThe first Federal Open Market Committee (FOMC) meeting, under new Federal Reserve Chair Kevin Warsh, delivered no change to interest rates, but it may prove significant for another reason. Rather than focusing on future rate cuts, the Federal Reserve has signalled that inflation remains its primary concern and that financial markets should place greater emphasis on incoming economic data rather than central bank guidance. At the time of writing, gold trades at approximately AUD $5,818, silver at AUD $83.56 and platinum at AUD $2294. Meanwhile, the Federal Reserve has maintained the federal funds rate at 3.50% to 3.75%, as largely expected by the market. More importantly, the meeting marked a noticeable change in tone from the Federal Reserve itself.

What changed at Kevin Warsh’s first Federal Reserve meeting?

Warsh’s first meeting was notable not only for the decision to leave rates unchanged, but also for how the decision was communicated. Under former Chair Jerome Powell, financial markets became accustomed to extensive forward guidance; Warsh appears intent on moving in a different direction. The June policy statement was significantly shorter and less detailed than those issued under previous leadership. Warsh also removed forward guidance from the statement and declined to submit his own interest rate projections as part of the committee’s quarterly “dot plot.” Instead, he repeatedly emphasised that financial markets should respond to economic data rather than attempting to interpret Federal Reserve intentions. In practical terms, this means Wall Street may receive fewer clues regarding future policy decisions. Investors, economists and fund managers will likely need to place greater emphasis on inflation reports, employment data and economic activity rather than relying on guidance from the central bank itself.

Why did the Federal Reserve hold interest rates steady?

The primary reason for maintaining current interest rates is straightforward: inflation remains too high. The latest Consumer Price Index (Headline CPI) report showed annual inflation running at 4.2% in May 2026, the highest reading in three years. This represents a significant increase from the 2.4% annual rate recorded in January, before the escalation of conflict involving Iran and the subsequent energy shock. The Federal Reserve’s preferred inflation target remains 2%. Current inflation therefore remains more than double the desired level.

Perhaps more importantly, the committee’s own projections suggest policymakers are becoming less inclined to cut rates anytime soon. Every participating policymaker projected that rates would either remain unchanged or move higher by year end. Median forecasts place the federal funds rate at 3.8% in 2026, 3.6% in 2027, 3.4% in 2028 and 3.1% over the longer term. The balance of risks appears tilted toward higher rates rather than lower ones, for the moment.

Why is inflation still running above the Fed’s target range?

Energy

While energy prices have been the most visible contributor to inflation, the broader picture remains more complex. The U.S.-Israel-Iran war and the disruption of energy markets has had a substantial impact on headline inflation (or overall inflation). In May, overall energy costs were up 23.5% year over year. Petrol prices increased 33%, while fuel oil prices surged 58.9% in the U.S. The national average price for regular petrol climbed from approximately USD $3.12 per gallon a year ago to USD $4.15 (USD 69 cents to $1.10 per litre).

Shelter

However, inflation is not solely an energy story. Shelter costs, which represent the largest component of the CPI basket, continue to rise steadily. The shelter index increased 3.4% over the previous twelve months. Because housing costs typically adjust slowly as leases are renewed, shelter inflation tends to remain elevated long after other categories begin cooling.

Services

Services inflation also remains persistent. Transportation services were up 4.1% year over year, while medical care services increased 3.6%. These categories are particularly important because they often reflect broader labour costs and underlying economic demand rather than temporary commodity price shocks.

Collectively, these factors explain why the Federal Reserve remains reluctant to declare victory over inflation.

Why isn’t the labour market forcing rate cuts?

Another major factor influencing interest rates is employment. Historically, the Federal Reserve faces pressure to lower rates when unemployment rises sharply or economic activity deteriorates. Technically, neither condition currently exists. Employers added approximately 172,000 jobs during May, while the unemployment rate remained stable at 4.3%. Over the past year, unemployment has largely remained within a narrow range between 4.3% and 4.5%. This is a markedly different environment from 2022 at the height of the Covid 19 Pandemic Era, when there were just over two job vacancies per unemployed worker and labour shortages were driving rapid wage growth throughout the economy. Today’s labour market appears substantially more balanced with about one job vacancy per unemployed worker.

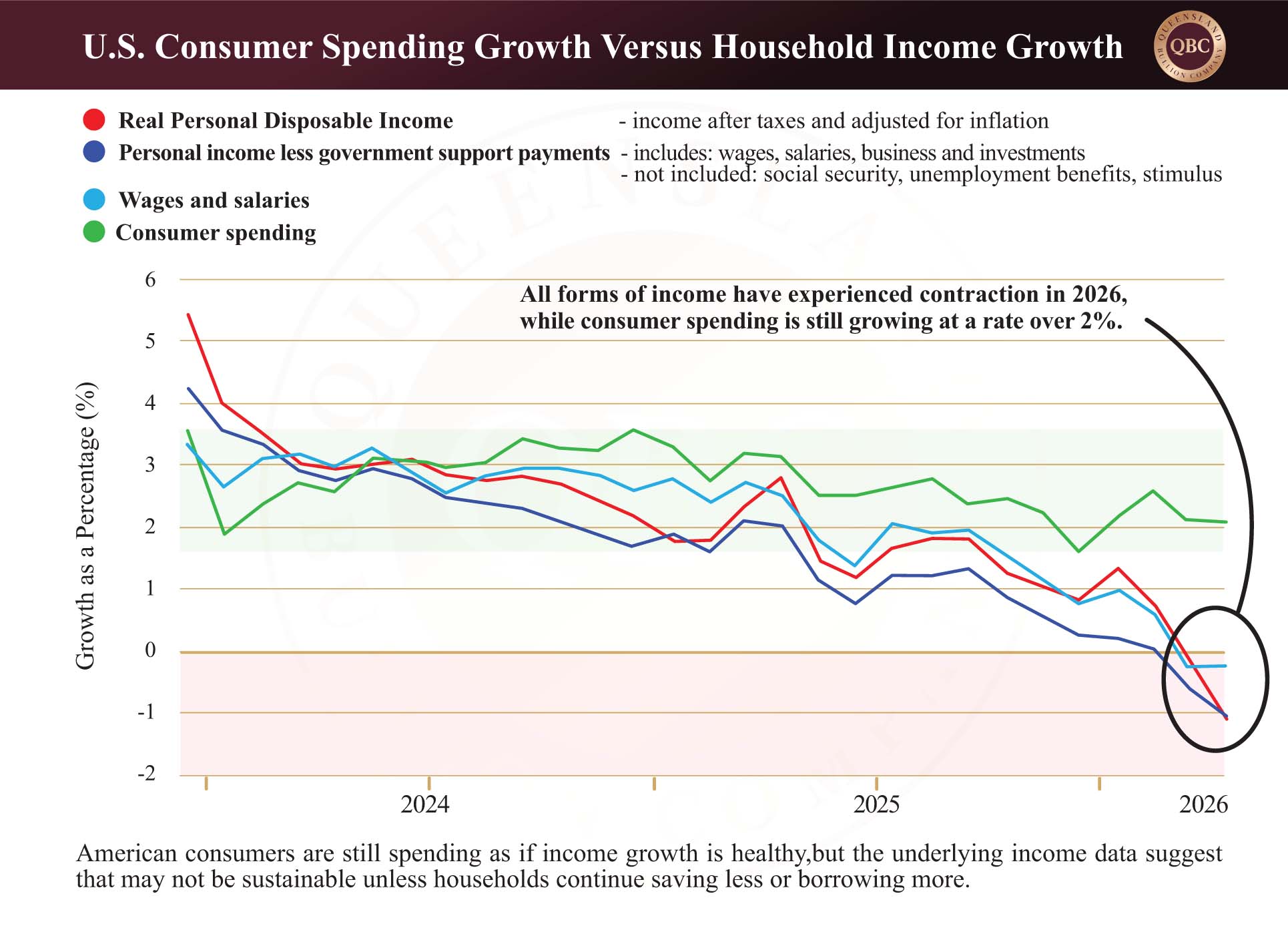

However, while inflation continues to rise, both wage growth and the household savings rate in the United States have moved sharply lower. Rather than being supported by stronger earnings, consumption is increasingly being sustained through reduced savings, as the chart below illustrates. While some economists may regard this as a red flag, the Federal Reserve insists that with employment remaining relatively stable, it has room to wait and assess whether inflation continues easing or begins accelerating further.

What is the bond market telling investors?

One of the most immediate consequences of the Fed’s decision can be seen in bond markets.

The U.S. 10-year Treasury yield currently sits near 4.5%, a level last consistently observed in September 2007 before the Global Financial Crisis (GFC). Meanwhile, the 30-year Treasury yield has climbed to approximately 4.9%, levels not seen since July, 2007. Australian bond markets reflect similar conditions. Australian 10-year government bond yields currently sit around 4.8%, while 30-year bonds yield approximately 5.3%. For investors, these yields are becoming increasingly attractive.

Core CPI (inflation without the volatility of food and energy included) currently sits at approximately 2.9% while Headline CPI (which includes everything) is 4.2%. A 10-year Treasury yielding 4.5% therefore provides a real return buffer of roughly 1.6% compared to Core CPI or 0.2% when measured against Headline CPI, while longer-duration bonds offer an even greater margin above inflation. Either way, Government bond yields offer investors immediate protection against inflation. Bonds once again provide meaningful income and a reasonable opportunity to maintain purchasing power.

How do higher interest rates affect gold and silver?

This environment creates a more challenging short-term backdrop for precious metals. Gold and silver do not generate income, so when bond yields rise and investors can earn a return above inflation, some capital naturally shifts toward fixed-income markets. This helps explain why precious metals often consolidate during periods of rising yields; however, the broader picture remains more complex. Inflation has not been resolved, government debt continues to expand, geopolitical tensions remain elevated, and energy markets are still vulnerable to disruption. These same pressures that support higher bond yields also strengthen the long-term case for tangible assets. In the short term, gold and silver must compete with bonds for capital. Over the longer term, their role is tied to purchasing power preservation, currency risk, and confidence in the broader financial system. If inflation outstrips bond yields (as it did leading up to the GFC and during the Covid 19 Pandemic Era), look to see capital rotate back to precious metals. As the second half of 2026 unfolds, the tension between these forces is likely to remain one of the most important themes across global markets.