The AI IPO Wave: Boom or Bubble?

by Evie SoemardiFinancial markets appear poised for one of the largest concentrations of initial public offerings (IPOs) in modern history. Over the coming months, three of the most prominent names in artificial intelligence and advanced technology, SpaceX, OpenAI and Anthropic, are expected to seek public listings with combined valuations approaching USD $4 trillion. With Morgan Stanley, Goldman Sachs, Bank of America, Citigroup and JPMorgan as typical underwriters confidence is brimming. At the time of writing, gold trades at approximately AUD $6,123 per ounce, silver at AUD $95, and platinum at AUD $2,496. While precious metals have spent much of the year consolidating, equity markets continue to chase growth, particularly anything associated with artificial intelligence.

The question facing investors is whether these listings represent the next stage of technological innovation or the latest chapter in a speculative cycle that increasingly resembles previous market manias. More importantly, what happens to broader financial markets when trillions of dollars of capital are required to fund a handful of highly anticipated public offerings?

Valuations reach extraordinary levels

While the companies themselves are undeniably influential, valuation remains a separate question. Based on reported 2025 revenue of approximately USD $18.67 billion, SpaceX’s proposed valuation of USD $1.75 trillion implies a trailing price-to-revenue ratio of roughly 94 times, compared to Tesla at approximately 17 times revenue when it floated. Supporters argue such comparisons struggle to account for businesses creating entirely new industries as SpaceX is expected to achieve. Critics, however, point to the dot-com boom of the late 1990s when investors similarly argued conventional valuation methods no longer applied. While many of those technologies ultimately transformed the world numerous share prices proved unsustainable. The same debate now surrounds artificial intelligence: the technology may be revolutionary, but investors must still determine how much future growth has already been incorporated into current valuations.

A historically crowded IPO calendar

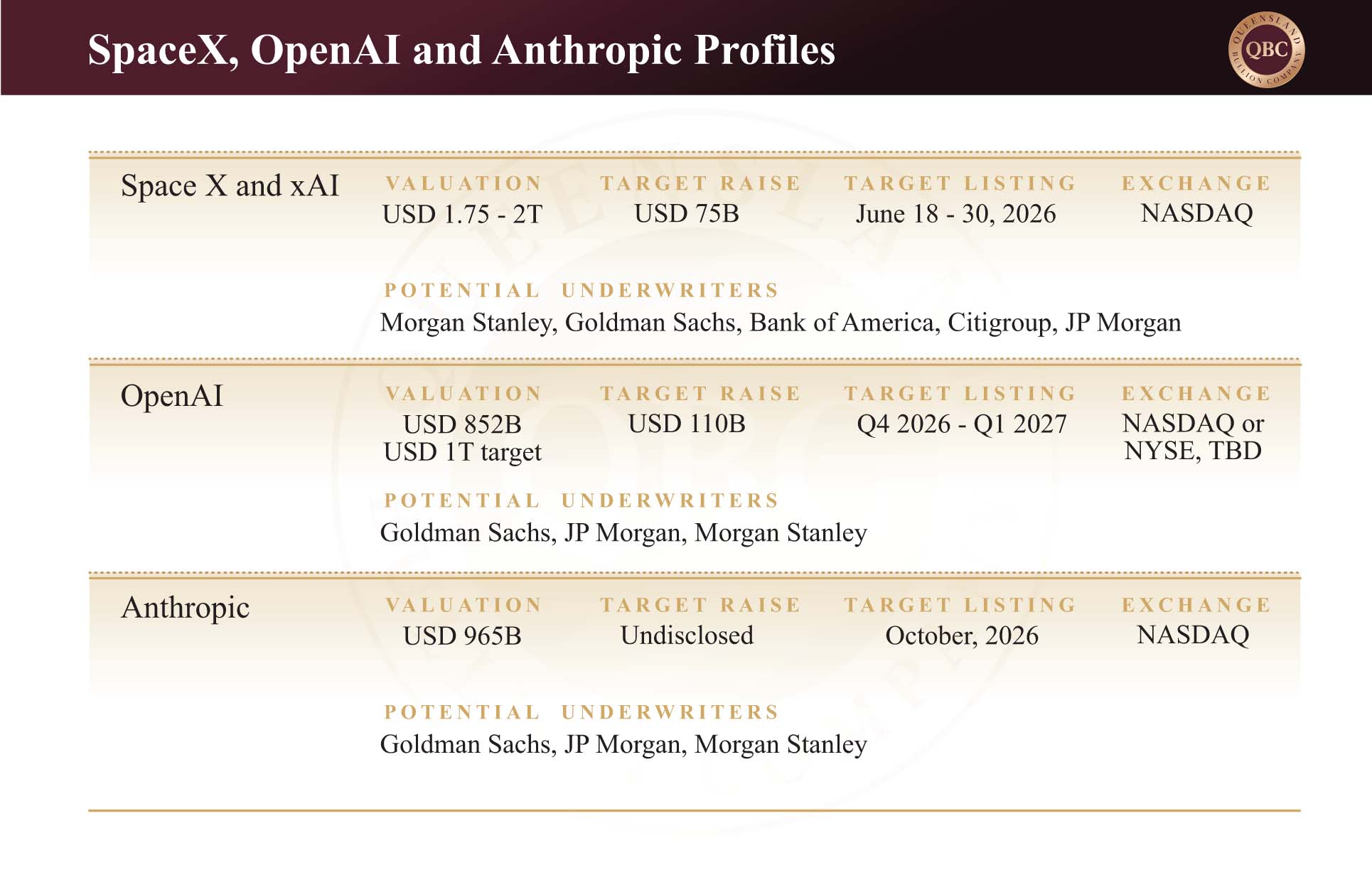

The scale of what is being proposed is difficult to overstate. SpaceX is targeting a valuation of approximately USD $1.75 to $2 trillion. OpenAI will pursue near USD $1 trillion, while Anthropic seeks a valuation exceeding USD $965 billion. Combined, these three companies potentially represent around USD $3.7 to $4 trillion in market capital. To place this into perspective, the entire Australian Securities Exchange (ASX) currently carries a market capitalisation of approximately AUD $3.2 trillion (or USD $2.28 trillion). The implications are significant.

An initial public offering is the process by which a private company sells shares to public investors for the first time. Of the 5% that SpaceX is selling, the company intends to reserve up to 30% of the offering for retail investors. This is significantly above the industry norm of 5% to 10%. The smaller than normal exposure to the wholesale market presents questions that only time will answer.

The liquidity question

Beyond valuation, another issue receives far less attention: liquidity. Every dollar invested in an IPO must come from somewhere. When multiple mega-capitalisation listings occur within a compressed timeframe they compete for the same pool of investment capital.

SpaceX alone is expected to sell approximately 555.6 million shares at around USD $135 per share to raise roughly USD $75 billion. OpenAI and Anthropic could collectively seek hundreds of billions more as they transition into public ownership. This creates an unusual dynamic. Large allocations into new offerings can therefore drain liquidity from other areas of the market. Investors seeking exposure to these listings may fund their participation by reducing positions in existing technology giants such as Apple, Microsoft, Alphabet, Amazon, Nvidia and Meta, and above all, Bitcoin. Such a rotation could create heightened volatility across the broader technology sector as capital is redistributed toward a small number of highly anticipated IPOs.

Dotcom Bubble Déjà Vue?

The closest historical comparison may be the dot-com boom of the late 1990s. As internet adoption accelerated, investors poured capital into technology companies at an unprecedented rate, often placing growth potential ahead of profitability, cash flow and conventional valuation metrics. The result was a speculative frenzy that drove the Nasdaq to a peak of 5,048 on 10 March 2000. What followed was a sharp reversal. By 4 October 2002, the index had fallen to 1,139, wiping out 76.81% of its value and destroying trillions of dollars in market capitalisation. More importantly, the recovery was measured not in months but in decades. The Nasdaq did not reclaim its previous high until April 2015, approximately fifteen years later.

Today, artificial intelligence is generating a similar level of enthusiasm, and the proposed IPOs are arriving into a market already willing to assign extraordinary valuations to future growth. The 18.6-year Real Estate and Economic Cycle places this IPO wave at the height of broader market euphoria that typically occurs just before a significant economic downfall that could see 30% wiped off the stock market overnight. Are we certain this will happen in the near future? No. But could the IPO event turn into one of the largest dotcom-esque “pump and dump” schemes in history? Yes. At this stage in the cycle, anything is possible.

Echoes of previous cycles

None of this means the AI revolution is not real. Artificial intelligence is already reshaping software development, research, automation, customer service, healthcare and defence applications. Unlike many speculative themes of previous decades, genuine revenue and commercial adoption exist today. However, history demonstrates that transformative technologies and speculative excess often arrive together. Railways transformed transportation. Electrification transformed industry. The internet transformed communication. Yet each of those innovations was accompanied by periods where investor enthusiasm pushed valuations far beyond what fundamentals could justify. The danger for investors is not necessarily choosing the wrong technology. It is paying too much for the right technology. That distinction becomes increasingly important when market participants begin valuing future possibilities rather than present realities.

What it means for precious metals

At first glance, the AI IPO boom appears unrelated to precious metals. In practice, the connection is straightforward. Periods of speculative enthusiasm typically attract capital away from defensive assets such as gold and silver. Investors become willing to accept greater risk in pursuit of higher returns. Money flows toward growth sectors, emerging technologies and momentum trades. This dynamic can create temporary headwinds for precious metals; however, speculative cycles also tend to increase systemic risk over time. Elevated valuations, concentrated capital flows and excessive leverage create vulnerabilities that often remain hidden during the boom phase. When expectations eventually collide with reality, capital frequently rotates back toward defensive assets. Gold and silver have performed this role repeatedly throughout history.

For precious metals investors, the key takeaway is that the broader macroeconomic backdrop has not changed. Debt continues to rise, fiscal deficits continue to widen, and central banks remain trapped between inflation and economic growth. Whether the AI boom ultimately becomes the next great technological success story or the next great market bubble, those longer-term fundamentals remain supportive of gold and silver. As always, the challenge is distinguishing between excitement and value before the market does it for you.