The Rise of Bond Yields

by Evie SoemardiFinancial markets are increasingly focused on one metric that quietly influences almost every asset class: the yield on U.S. Treasury bonds. While equities, precious metals and cryptocurrencies often dominate headlines, Treasury yields arguably provide one of the clearest measures of investor confidence in the broader economy. At the time of writing, gold trades at AUD $6,307 per ounce, silver at AUD $105.90, platinum at AUD $2,730, and the U.S. 10-year Treasury yield sits at approximately 4.46%.

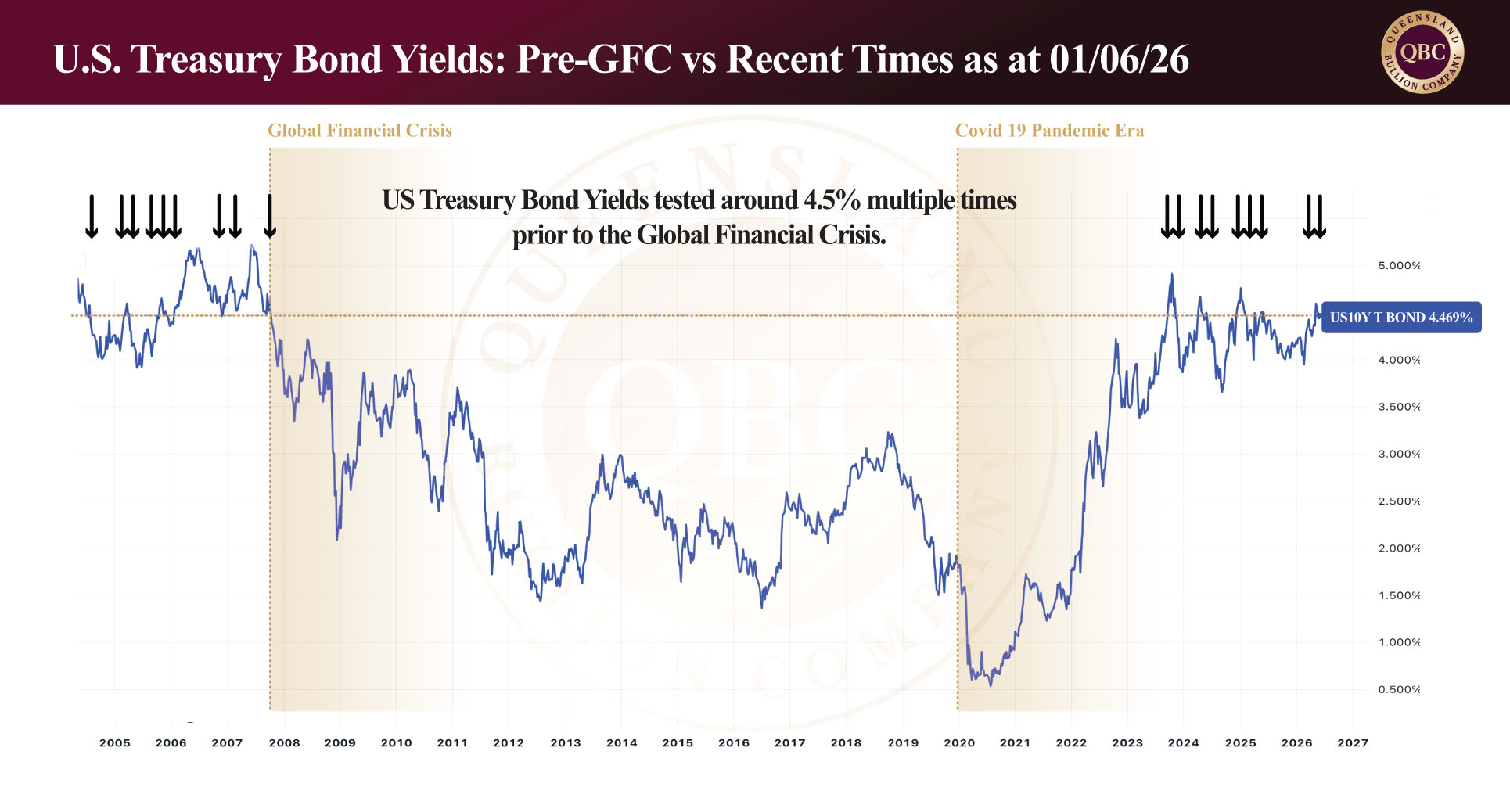

While this marks the fourth occasion the 10-year yield has reached this level in the past three years, it has not sustained these levels consistently since October 2007, immediately preceding the Global Financial Crisis (GFC). Interestingly, the period leading into the GFC displayed a similar pattern, with yields testing this level four times across a three-year period before broader financial stresses emerged. While history does not repeat exactly, it often rhymes. Understanding why yields are rising, and what investors are attempting to price into the market, provides valuable insight into the outlook for precious metals and financial markets more broadly.

Why are yields rising?

At its simplest, a bond yield is the return investors receive for lending money to a government. When investors become concerned about inflation, fiscal sustainability, or future economic uncertainty, they demand a higher return to compensate for taking on additional risk. The result is higher yields on newly issued bonds and lower bond prices in secondary markets.

The United States provides no shortage of reasons for concern. According to the U.S. Treasury, national debt has reached approximately USD $39 trillion while the country currently runs an unsustainable 7% account deficit. The debt-to-GDP ratio now sits at roughly 100.2%, the first time it has exceeded 100% since World War II. For the 2026 financial year, federal interest payments alone are expected to reach approximately USD $1.039 trillion, while the annual budget deficit remains around USD $2.5 trillion. The Congressional Budget Office projects debt could climb to 175% of GDP by 2056 if current trends continue. The United States now spends 50% of its annual tax revenue on making interest-only payments towards its debt. The scale of borrowing is difficult to comprehend. U.S. debt is currently increasing by approximately USD $55 to 88 billion every day. As more debt is issued larger volumes of Treasury bonds must be absorbed by the market, increasing supply and placing upward pressure on yields.

Viewed through a business lens, the explanation becomes relatively straightforward. When a company takes on increasing amounts of debt without a corresponding improvement in its financial position, lenders demand a higher rate of return to compensate for the growing risk. Governments are no different. While the United States remains the world’s largest economy and the issuer of the global reserve currency, investors are increasingly scrutinising its fiscal trajectory. Rising debt levels, persistent deficits, and rapidly growing interest expenses are prompting bond markets to demand greater compensation for lending money to the U.S. government.

When higher yields are not good news

What makes the current environment particularly interesting is that the apparent strength in bond yields may actually be signalling a deeper weakness in the underlying currency itself. Throughout history, governments confronted with excessive debt burdens have ultimately resorted to some form of currency debasement to ease the pressure. The 1970s provide a useful example. During that decade, the U.S. dollar lost roughly half its purchasing power while gold rose from USD $35 to USD $850 per ounce. Importantly, that move was not a straight line. Sharp corrections and periods of investor pessimism repeatedly interrupted the broader trend before gold ultimately reached new highs. Today, many investors remain focused on the attraction of higher bond yields, yet those yields exist partly because markets are demanding greater compensation for fiscal and monetary risks. In that sense, rising yields and rising gold prices need not be opposing forces over the longer term. Both can be interpreted as different market responses to the same underlying concern: preserving purchasing power in an increasingly debt-laden financial system.

The inflation problem

Rising debt would be less concerning if economic growth was strong and inflation remained contained. However, investors are now attempting to price multiple risks simultaneously. The ongoing disruption to global energy markets, particularly surrounding the Strait of Hormuz, has pushed oil prices materially higher causing fundamental supply and demand issues. Higher energy costs eventually filter through transport, manufacturing, agriculture and consumer goods, creating a flow-on effect of inflationary pressure throughout the economy.

This places central banks in a difficult position. If inflation remains elevated, policymakers may be forced to keep interest rates higher for longer. If they lower rates too quickly, inflation risks accelerating once again.

What does this mean for gold and silver?

Traditionally, rising bond yields can create short-term headwinds for gold because Treasury bonds begin offering more attractive income streams. Investors comparing a non-yielding asset such as gold against a government bond yielding close to 5% may favour the bond initially; however, yields alone do not tell the whole story. The more important measure is the real yield, being the difference between bond yields and inflation. If inflation continues rising faster than yields, investors still lose purchasing power despite earning interest. This is the point where gold often begins outperforming.

History shows that precious metals tend to struggle during the early stages of rising yields but perform strongly when markets begin questioning whether governments can realistically control debt and inflation simultaneously. The current environment is increasingly moving in that direction.

In summary

Rising bond yields are not occurring in isolation. They reflect growing concerns surrounding inflation, government borrowing, fiscal sustainability and the long-term health of the global financial system. With U.S. debt approaching USD $39 trillion, annual deficits more than USD $2 trillion, and interest costs exceeding USD $1 trillion per year, yields on Treasuries are bound to increase.

In the short term, higher yields may continue to compete with gold and silver for investment capital. However, if inflation persists and debt continues expanding at its current pace, the market may eventually reach a point where bond yields can no longer adequately compensate for the loss of purchasing power. Historically, that is when precious metals become increasingly attractive. Rising yields may appear bearish for gold today, but they may ultimately be signalling the very conditions that support higher precious metals prices tomorrow.