The AI Capital Race Expands

by Evie Soemardi

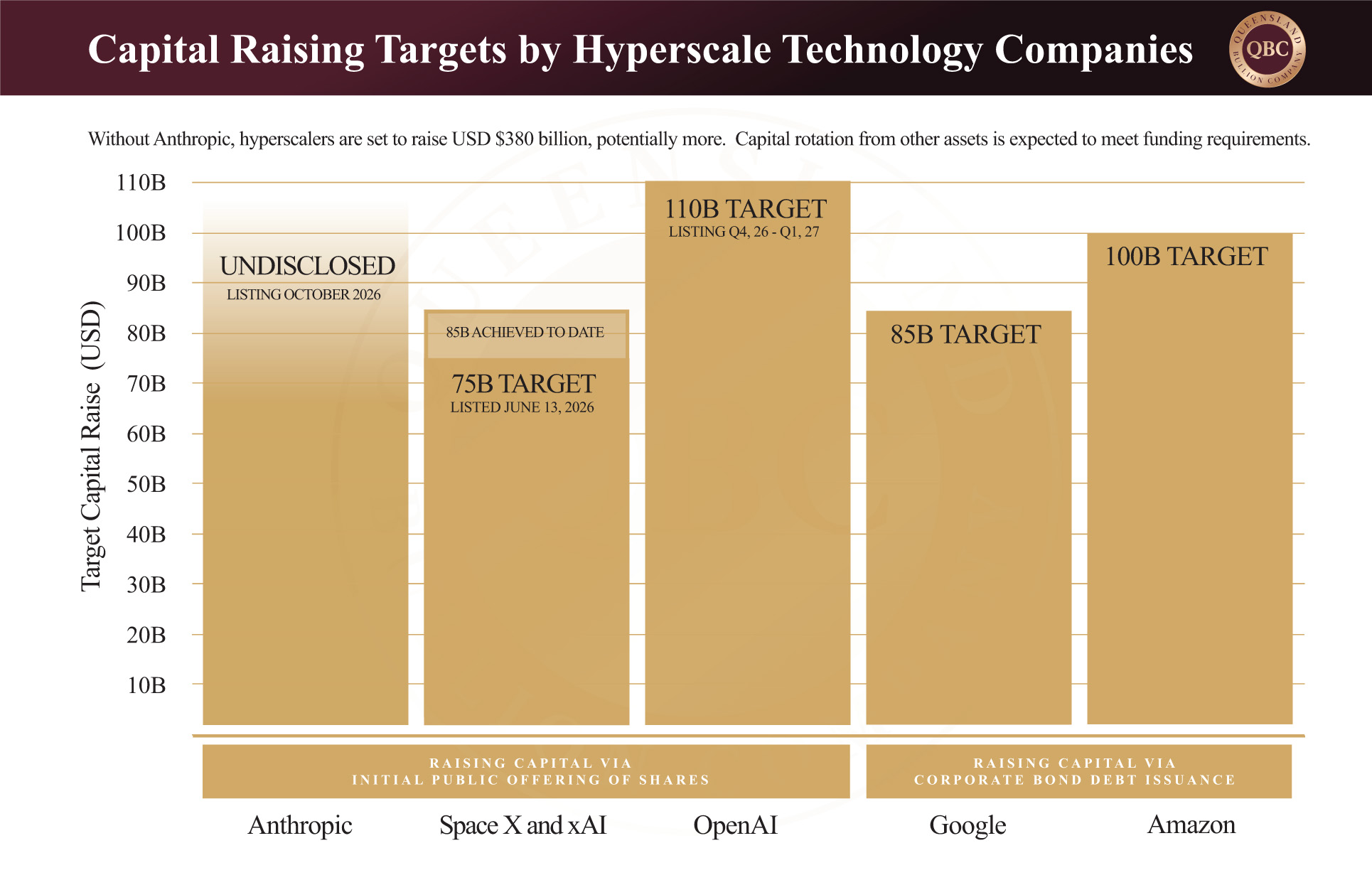

Artificial intelligence continues to dominate financial markets, but the story is evolving beyond valuations and upcoming initial public offerings (IPOs). While investors have focused heavily on listings such as SpaceX, OpenAI and Anthropic, another capital-raising wave is quietly developing alongside them. This time it is coming from some of the world’s largest publicly listed technology companies.

At the time of writing, gold trades at approximately AUD $6,134, silver at AUD $99.23 and platinum at AUD $2,544.51. Meanwhile, technology giants are committing unprecedented sums toward AI infrastructure, data centres and cloud-computing capacity. Whether through IPOs, bond issuances or capital expenditure programmes, the common theme is capital. While the mechanisms differ, all of these initiatives are ultimately competing for the same pool of global capital within a relatively compressed timeframe.

Different paths to the same destination

The upcoming AI-related IPOs involve private companies selling ownership stakes to public investors for the first time. The objective is straightforward: raise capital to fund growth while providing liquidity to existing shareholders. Established public companies operate differently. Rather than selling new ownership interests, they often raise funds through debt markets by issuing corporate bonds (i.e. they sell debt and pay back with interest). Investors lend money to the company in exchange for a fixed return, while the company gains access to capital without diluting existing shareholders. These debt obligations are paid out prior to dividends. Although the structures differ, the outcome is remarkably similar. Investors must decide where to allocate their funds. Capital directed toward a bond issue is capital unavailable for an IPO or share purchase. Capital committed to an equity raising cannot simultaneously be invested elsewhere. Money can only be spent once.

Google’s historic debt raise

Google’s parent company, Alphabet, has increased their target raise from USD $80 billion to USD $84.75 billion. They have already recently demonstrated the scale of this competition by raising approximately USD $32 billion through eleven separate corporate bond tranches. The offering ranged from two-year notes through to 100-year bonds making it one of the largest corporate debt issuances in recent years. The century bond alone attracted approximately USD $9.5 billion in orders despite offering a spread of only 120 basis points above comparable government debt. The last time 100-year bonds were issued was during the dot-com bubble in 1997; in this instance Motorola offered USD $300 million worth of 100-year bonds and is today heralded as a prime example of peak corporate confidence to occur near the top of a cycle. As with many other technology giants during the dot-com crash, Motorola went on to lose approximately 79% of market capital over the next three years. Again, history does not repeat but it certainly can rhyme.

The timing is noteworthy. Just days before the debt issue, Alphabet announced plans to increase capital expenditure to approximately USD $80 billion in 2026, largely directed toward artificial intelligence infrastructure. The debt raise therefore appears less about strengthening the balance sheet and more about funding one of the largest technology expansion programmes currently underway.

The data centre arms race

The debt itself is not the most important story. The spending it enables is. Artificial intelligence requires extraordinary amounts of computing power. That computing power requires data centres, semiconductors, networking equipment, electricity generation and cooling systems on a scale rarely seen in the private sector. Morgan Stanley estimates spending by hyperscale cloud-computing companies could reach approximately USD $400 billion during 2026, up from around USD $165 billion in 2025. In a single year, projected investment is expected to increase by approximately USD $235 billion. Alphabet’s USD $80 billion commitment is only one part of a much larger trend. Amazon is expected to spend approximately USD $200 billion on capital expenditure this year, while Microsoft and Meta continue directing tens of billions of dollars toward AI-related infrastructure. Collectively, these commitments represent one of the largest peacetime technology build-outs ever undertaken. Debt raises, bond offerings and equity issuances are financing mechanisms. Capital expenditure represents the physical deployment of resources into productive assets. The AI story is increasingly becoming an infrastructure story.

Amazon and the expanding investment cycle

Amazon sits at the centre of the same trend. Through Amazon Web Services (AWS), the company operates one of the world’s largest cloud-computing businesses and remains heavily exposed to the growth of artificial intelligence. Some of its customers include Netflix, Airbnb, Adobe, Canva, and thousands of government agencies, with 924 data centres and counting spread across 50 countries as at 2023. To put this in perspective, Australia is home to just over 250 data centres nationwide. To maintain its competitive position, Amazon has published capital expenditure of USD $128.3 billion in 2025. In order to remain a contender the company has announced a spend of $200 billion in 2026, the bulk of which has been assigned to support AI infrastructure, data-centre construction and computing capacity. Why is Amazon investing so heavily into AI and customised web services? As a company asset, AWS generates around 60% of total profits and is seen to be capped by supply issues rather than demand.

What makes this particularly significant is that Amazon, Alphabet, Microsoft and Meta are all pursuing similar strategies simultaneously. Each company is seeking to expand computing capacity at an unprecedented pace, placing increasing pressure on engineering talent, semiconductor supply chains, electrical infrastructure and available investment capital. The result is an industry-wide competitive investment cycle that increasingly resembles a modern industrial build-out rather than a traditional software expansion.

The competition for capital

Viewed in isolation, a USD $32 billion bond issue or a USD $75 billion IPO may not appear extraordinary; however, viewed collectively a different picture emerges. SpaceX overshot their target raise of USD $75 billion by USD $10 billion, raising $85.7 billion to date. OpenAI is pursuing USD $110 billion. Anthropic is targeting a valuation approaching USD $1 trillion and needs to raise enough capital to match. Alphabet wants to raise USD $84.75 billion in funds via debt while planning approximately USD $80 billion in capital expenditure. And Amazon is targeting around USD $100 billion. Investors seeking exposure to these opportunities may fund their participation by reducing positions elsewhere. Institutions allocating funds to major IPOs may rebalance existing portfolios. Bond investors participating in large debt issuances may redirect capital away from other fixed-income opportunities. The question is how broader markets will respond as hundreds of billions of dollars are simultaneously drawn toward a single investment theme.

In summary

The most important development is not the individual moving parts. Rather it is the combined effect of investment capital raising in a contracted timeframe during a significant technology stock boom. Some is being raised through debt markets. Some comes from retained earnings and internal cash flows. And some of that capital is being raised through IPOs (which could turn out to be the most excessive pump and dump scheme in history). Regardless of the source, the destination remains the same: a massive build-out of AI infrastructure. Inflows of capital into a single sector of this magnitude has historically equated to excessive valuations; consequently, other asset classes become undervalued as capital rotates into the “next big thing.” In such an environment gold and silver stand out as the perfect contrarian investment. While short-term price movements will continue to be dictated by broader market conditions, the long-term trend remains clear. The AI revolution is no longer simply a software story. It is becoming one of the largest infrastructure projects in modern economic history, and that carries significant implications for the commodities required to build it.