When War Reprices Markets: Oil and Bonds Up, Everything Else Down

by Evie Soemardi

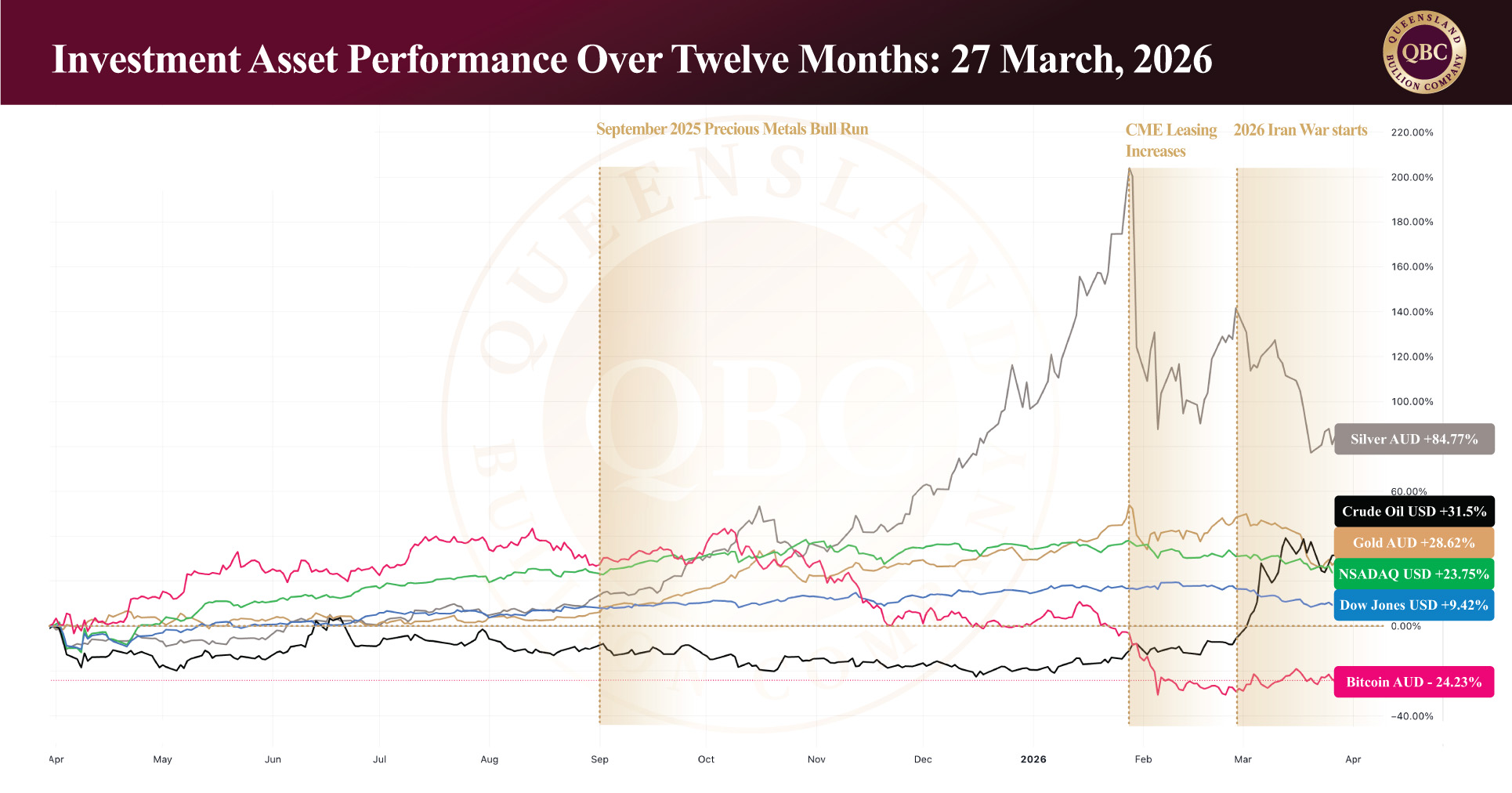

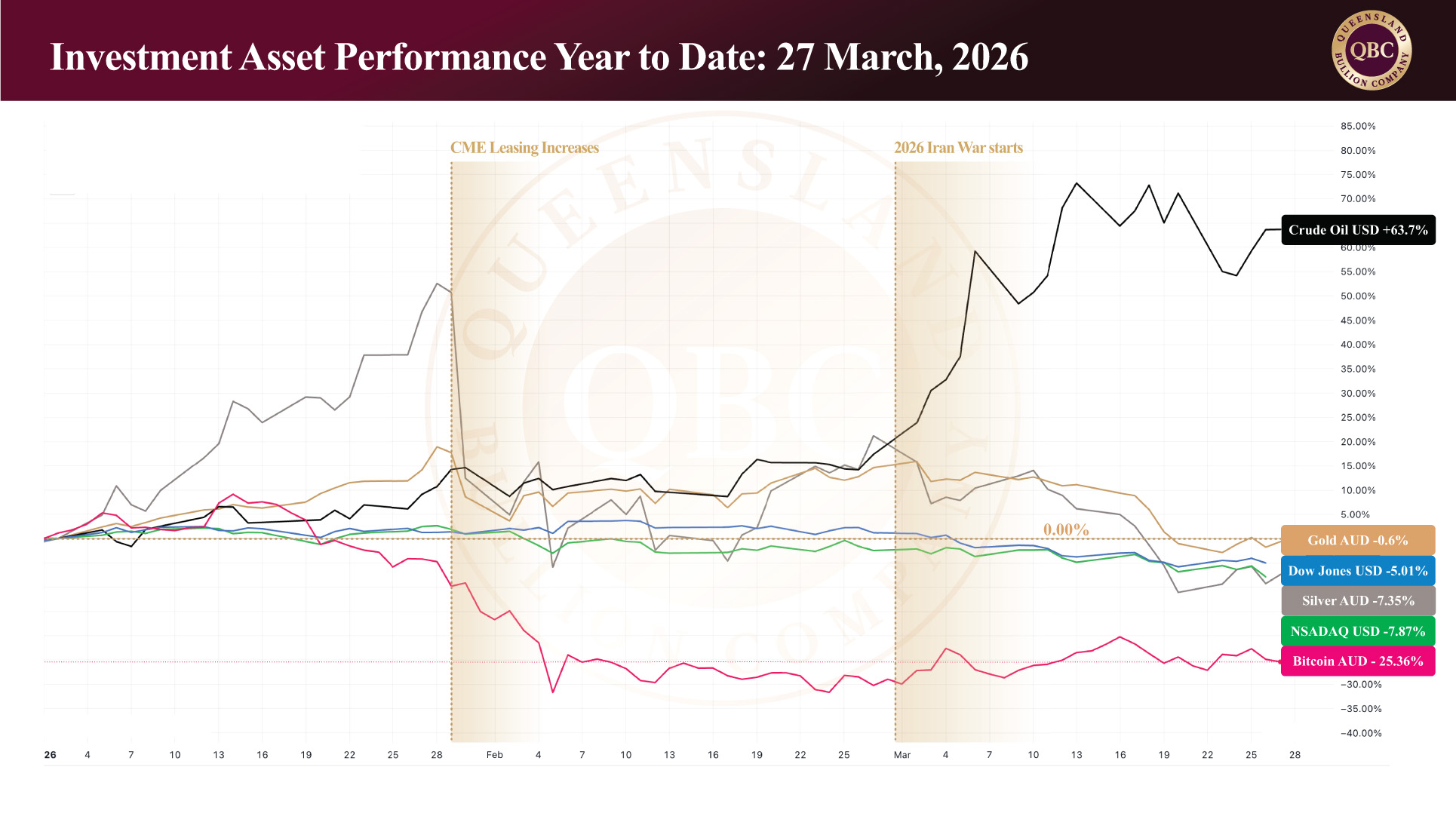

Global markets have entered a phase where nearly all asset classes are under pressure, with two notable exceptions: oil and U.S. Treasury yields. Since the escalation of the Iran conflict, capital has been forced to reposition rapidly, producing a divergence rarely seen across financial markets. At the time of writing, gold trades around AUD $6,401 per ounce, silver sits near AUD $99.19, and platinum around AUD $2,670, each reflecting varying degrees of consolidation or decline following earlier gains.

This environment is being shaped by more than just conflict headlines. The interaction between geopolitics, energy markets, inflation expectations, and monetary policy is creating a complex backdrop where some traditional safe-haven behaviour is being challenged. To understand why precious metals, equities, and cryptocurrencies are under pressure while oil and yields rise, we must first examine the evolving situation on the ground and how markets are interpreting it.

A conflict without resolution

What initially appeared to be a contained escalation has evolved into a prolonged and increasingly complex regional conflict. Iran and the United States now appear entrenched at an impasse, with ceasefire discussions failing to gain traction and military positioning intensifying across the Middle East.

U.S. President Donald Trump has extended the deadline for Iran to reopen the Strait of Hormuz to April 6, while Iran has simultaneously tightened its control over the passage. Israel has increased troop deployments into southern Lebanon to confront Hezbollah, further broadening the scope of the conflict. The situation has become one defined less by clear objectives and more by endurance, a test of which side can absorb the most sustained pressure.

Despite heavy strikes by U.S. and Israeli forces, including attacks on leadership targets and military infrastructure, Iran continues to respond with missile launches across the region. There is no indication of internal destabilisation within Iran, and diplomatic channels remain largely inactive. While the United States has reportedly delivered a 15-point framework for a potential resolution via Pakistan, Iranian officials have publicly stated that no meaningful negotiations of note are underway. The continued delay of the deadline from the U.S. Administration supports this notion.

This disconnect between political messaging and battlefield reality is critical. Markets, at least initially, appear to have priced in a shorter conflict; however, developments on the ground suggest a scenario that could extend far longer, and with broader economic consequences.

Oil: the immediate transmission mechanism

The most immediate and visible market response has been in energy. Iran’s control over the Strait of Hormuz, combined with continued attacks on Gulf energy infrastructure, has triggered a sharp repricing of oil.

Brent crude has risen more than 40% since the conflict began, recently settling at USD $101.89, up from approximately $70 pre-conflict. West Texas Crude (WTI) has followed a similar trajectory, climbing to USD $94.48 per barrel. These moves reflect not just current disruption, but the market’s attempt to price in the risk of sustained supply constraints.

Importantly, Iran itself has not been economically isolated by the conflict. Its oil exports continue largely unimpeded and are now fetching significantly higher prices. Estimates suggest Iran is generating approximately USD $139 million per day from oil sales, a notable increase from pre-conflict levels of approximately USD $106 million per day. This is up more than $25 million per day from historical levels. This dynamic introduces a paradox: while global markets are disrupted, Iran’s revenue base has strengthened, potentially prolonging its capacity to sustain the conflict.

Oil, in this context, becomes the central transmission mechanism through which geopolitical risk feeds into global markets.

Interest Rates and the Cost of Capital

The surge in oil prices has immediate implications for inflation, and by extension, U.S. federal fund rates. As energy costs rise, inflation expectations are pushed higher, a development that complicates the Federal Reserve’s policy outlook.

Recent labour data suggests a gradual softening in the U.S. job market, which under normal conditions might support a case for rate cuts; however, the inflationary pressure stemming from higher oil prices has effectively removed that option from consideration. Markets that entered 2026 expecting multiple rate cuts have rapidly repriced with expectations now shifting toward a higher-for-longer interest rate environment.

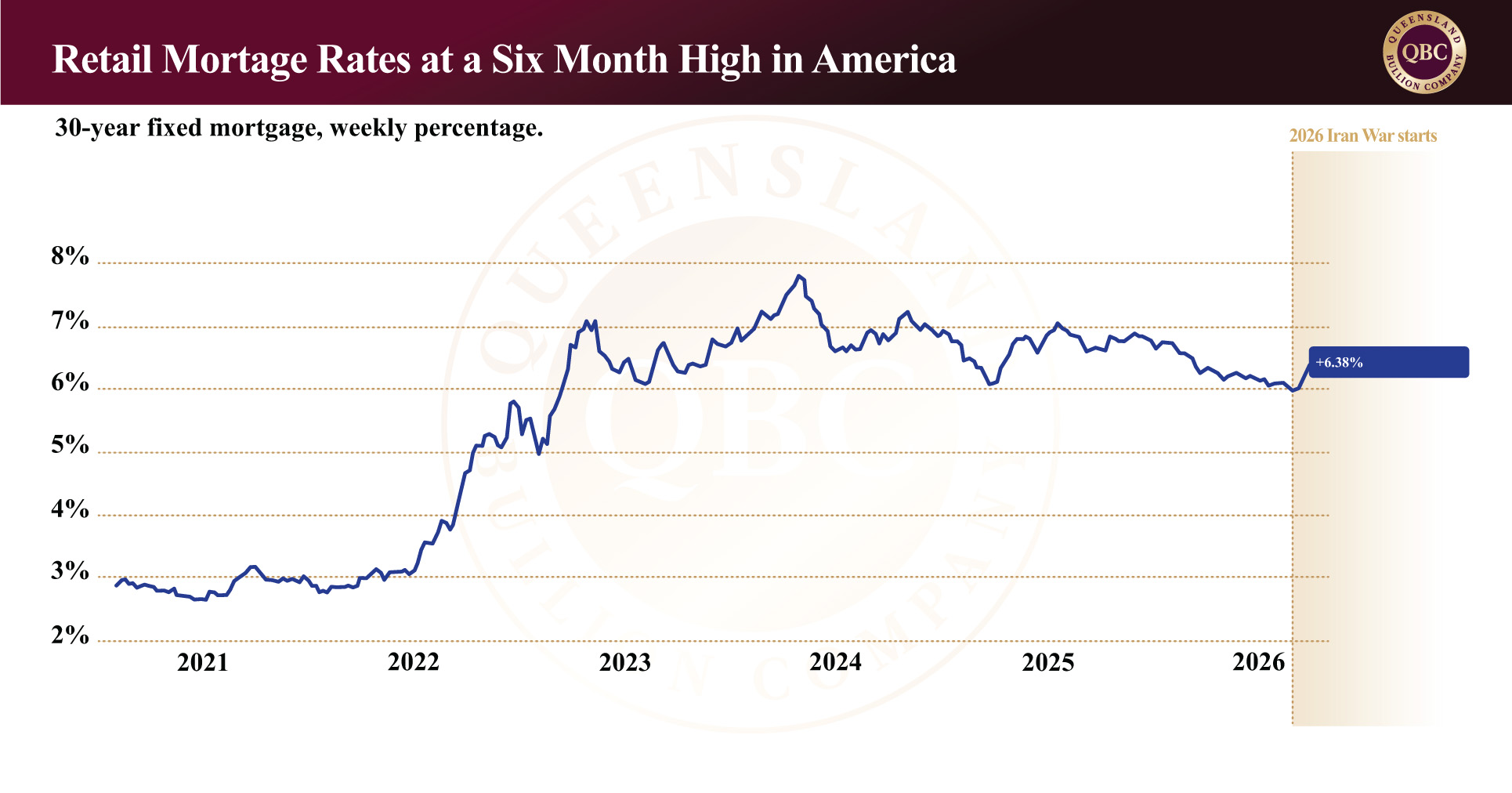

This shift is already flowing through to U.S. retail borrowing costs. The average 30-year fixed mortgage rate has risen to 6.38%, marking its highest level in more than six months and one of the sharpest short-term increases in recent periods. As financing costs rise across the economy, consumption slows, investment becomes more selective, and economic momentum begins to moderate.

In this environment, capital naturally gravitates toward assets that offer yield and limited downside, and that brings Treasury markets into focus.

Treasury yields: the short-term safe haven

The most telling move across markets has been the rise in U.S. Treasury yields. The yield on the 10-year Treasury has climbed to 4.42%, up from 3.97% before the conflict began. For bond markets, this is a significant shift, one that reflects both inflation expectations and increased demand for income-generating safe assets.

Treasuries are fulfilling a dual role. They are acting as a safe haven during geopolitical uncertainty, while simultaneously offering increasingly attractive yields as interest rate expectations adjust. This combination makes them highly competitive relative to other defensive assets.

The consequence is a redistribution of capital. Rather than flowing exclusively into gold, investors are splitting exposure between Treasury bonds and the U.S. dollar, both of which benefit from rising yields and global uncertainty.

Precious metals: pressure beneath the surface

This dynamic helps explain the current counterintuitive behaviour of precious metals.

Gold, traditionally one of the primary safe-haven assets, has come under pressure despite the escalation in conflict. Part of this weakness can be attributed to central bank activity, most notably Turkey’s recent sale and swap of approximately 60 tonnes of gold, worth over USD $8 billion. These transactions, driven by currency stabilisation efforts and rising energy costs, have added tangible supply into the market at a time when demand is being split across competing safe-haven assets.

Price action reflects this pressure. Gold in Australian markets is down 2.6% overnight, 3.5% over the past week, and 16.5% since the conflict began, though it remains up over 31% over the last twelve months — a reminder that the longer-term trend is still intact.

Silver has experienced even more pronounced movement. The metal has broken its prior uptrend and entered a corrective phase, with Australian prices down 27.4% since the start of the war and 41.5% from January highs. Despite this, silver remains over 81% higher on a 12-month basis, underscoring the magnitude of the preceding bull run.

In both cases, the key takeaway is not structural weakness, but capital competition. Gold and silver are not being rejected; they are being repriced within a broader safe-haven framework that now includes higher-yielding alternatives.

Equities and crypto: risk assets reprice

Risk-on assets have suffered even more than precious metals over the last twelve months. Overnight equity markets declined globally, with the Dow Jones falling 1% and the Nasdaq dropping 2.4%, officially entering correction territory after falling more than 10% from its recent highs.

Technology stocks have led the decline, with notable losses among major names such as Nvidia (4.2%), Meta (8%), Alphabet (3.4%), and Amazon (2%). This reflects a broader reassessment of risk in an environment where higher interest rates and geopolitical uncertainty reduce the appeal of growth-oriented investments. It also reflects that traders expect a lack of consumer demand in the future.

In the Australian market Bitcoin has followed a similar pattern, declining 2.6% overnight and remaining largely sideways over the last week. While it has held some ground since the conflict began, it remains down over 33% over the past twelve months.

In summary

Markets are currently operating under a fragile equilibrium shaped by a single dominant assumption: that the conflict will remain contained and relatively short-lived. Oil prices reflect disruption, Treasury yields reflect inflation and policy constraints, and most other asset classes reflect a cautious repricing of risk.

Yet the situation on the ground suggests a different possibility.

If the conflict continues to expand (or simply persists longer than expected) the current market positioning may prove incomplete. Oil could remain elevated or rise further, inflation pressures could intensify, and the competition between safe-haven assets could shift once again.

In that scenario, precious metals may reassert themselves more forcefully. Not because they have been absent, but because they have been competing. The current weakness in gold and silver is not necessarily a rejection of their role, but a reflection of how capital is being distributed in a more complex risk environment.

As history has shown, markets are most vulnerable when they are confident in their assumptions. If those assumptions begin to change, the reallocation of capital can happen quickly. In such conditions, preparation matters more than prediction, when considering protection.