Oil’s Shrinking Buffer

by Evie Soemardi

Global oil markets are entering increasingly dangerous territory as the 2026 U.S-Isreal-Iran War continues to disrupt flows through the Persian Gulf. What initially appeared to be a temporary supply shock is now evolving into a deeper structural problem: the world is rapidly burning through the inventories that normally protect against severe shortages and price spikes. At the time of writing, gold trades at approximately AUD $6,342 per ounce, silver at AUD $107.31 and platinum at AUD $2,745, while oil markets remain under sustained pressure.

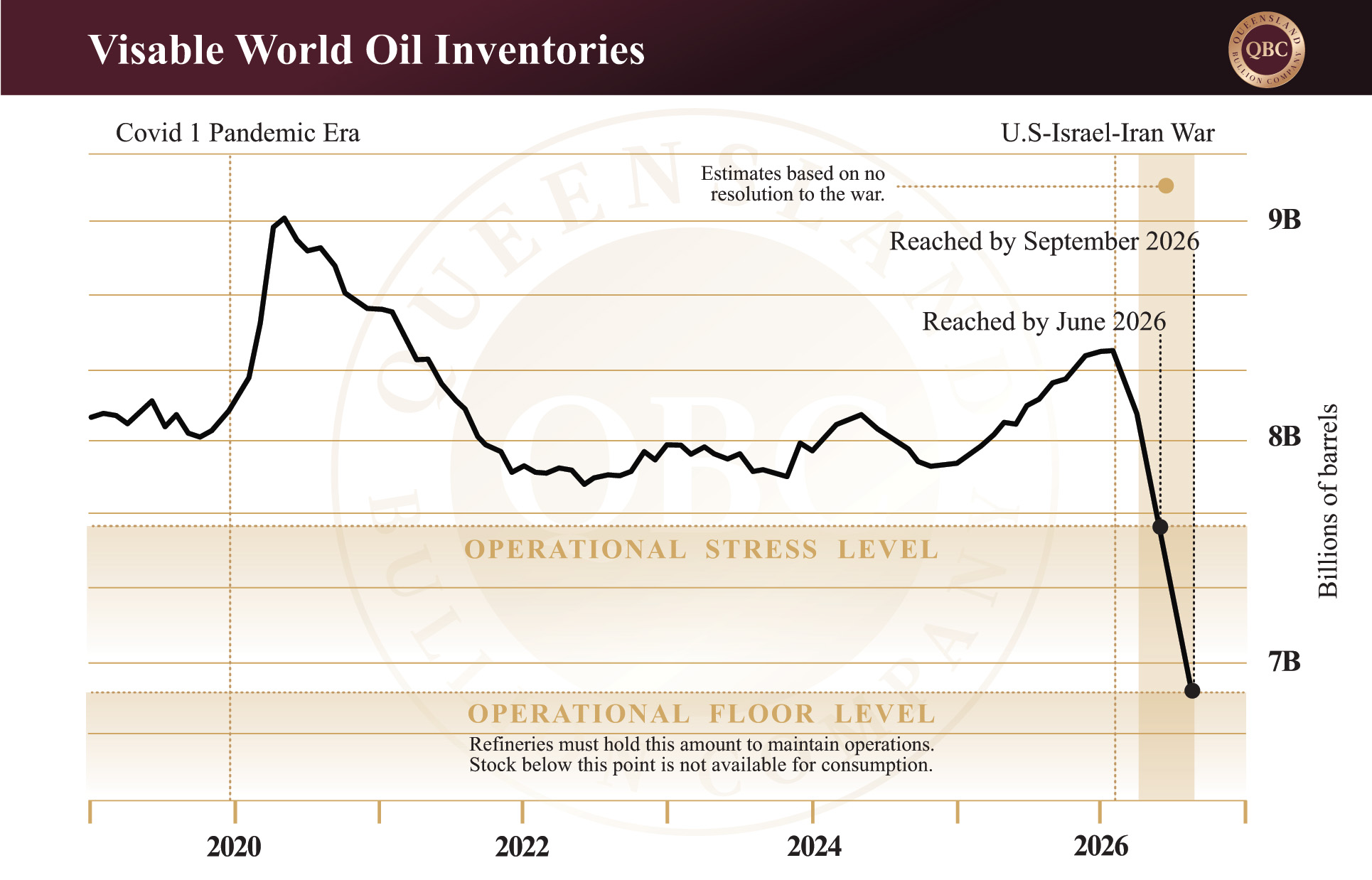

Since the Strait of Hormuz has moved toward near closure, the global oil system has been forced to rely heavily on stored reserves to maintain supply. These inventories act as the shock absorber of the global energy market and cushions disruptions when production or shipping becomes impaired. The problem is that the buffer is now being depleted at record speed. Morgan Stanley estimates global oil inventories fell by approximately 4.8 million barrels per day between March 1 and April 25, well beyond any previous quarterly drawdown recorded by the International Energy Agency. Crude oil accounted for almost 60% of the decline, with refined fuels making up the balance. This is not a minor adjustment in supply chains; it is a historically significant depletion of emergency capacity across the global energy system. So far, supply loss from Gulf producers exceed more than one billion barrels.

The operational minimum

Importantly, oil inventories do not need to reach zero before markets break down. Energy systems require a minimum amount of crude and refined fuel simply to continue functioning. Pipelines, export terminals, refineries and storage infrastructure all rely on what analysts call an “operational minimum.” JPMorgan has warned that inventories of the Organisation for Economic Co-operation and Development (OECD) could reach “operational stress levels” as early as next month if the Strait of Hormuz remains restricted, with “operational minimum” conditions potentially emerging by September. Indeed OECD countries have seen the sharpest declines in oil inventories at 146 million barrels, versus non-OECD countries seeing a drop of 24 million barrels.

This distinction matters. Markets can tolerate falling inventories for a period of time, but once operational minimums are approached the system becomes highly unstable. At that point, even small disruptions can create outsized price reactions because there is no longer enough spare supply available to absorb shocks. While Goldman Sachs notes the pace of drawdowns may have slowed slightly due to weaker Chinese demand, global visible oil inventories are already near their lowest levels since 2018. The world is no longer operating with a comfortable surplus.

The state of liquid fuel in Australia

Although Australia’s fuel inventories remain above mandated minimum levels, recent data highlights just how reliant the country remains on uninterrupted global supply chains. During the 2024–25 financial year, diesel stockpiles averaged 2,968 megalitres (ML), compared with a required minimum of 2,485 ML, leaving a buffer of approximately 19% above the government’s Minimum Stockholding Obligation (MSO). Petrol (gasoline) inventories averaged 1,743 ML against a required 1,070 ML, or 63% above minimum levels; while aviation fuel stocks averaged 799 ML compared with a required 581 ML, roughly 38% above mandated requirements.

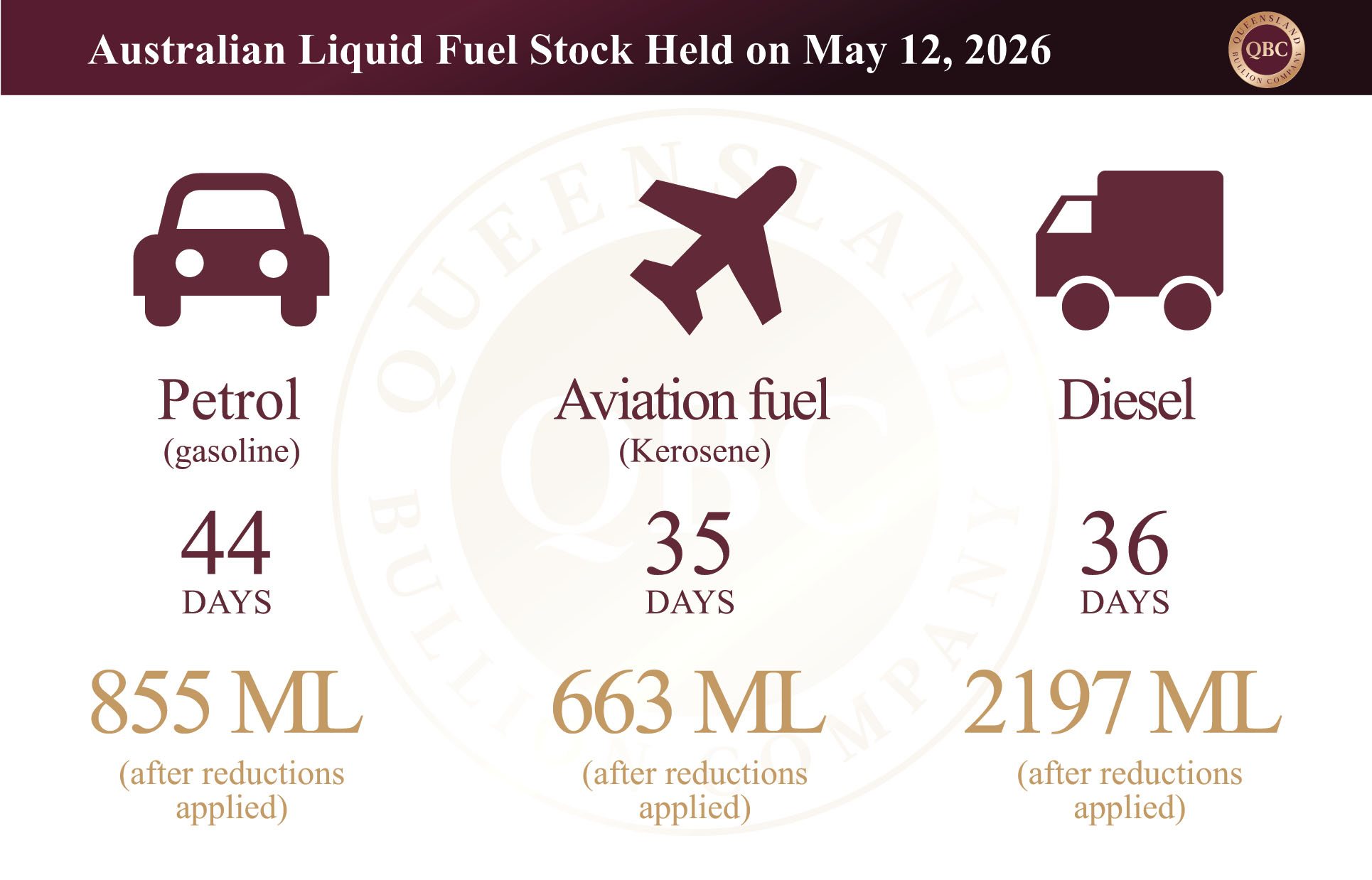

However, more recent figures as at May 12 this year suggest those buffers are tightening materially. Diesel inventories have fallen to 2,905 ML against a minimum requirement of 2,742 ML, leaving stock only 6% above mandated levels. Petrol inventories currently sit at 1,631 ML versus a required 1,067 ML, while aviation fuel inventories stand at 790 ML against a minimum 663 ML, reducing the surplus to approximately 19%. The decline in diesel reserves is particularly significant because diesel underpins freight transport, mining, agriculture and much of Australia’s industrial economy. Officially, Australia holds the equivalent of around 36 days of diesel consumption, 44 days of petrol, and 35 days of aviation fuel under normal conditions, hence the country remains heavily dependent on imported refined fuel and vulnerable to disruptions across major shipping routes and energy corridors such as the Strait of Hormuz.

Asia faces the greatest risk

The immediate pressure points are emerging in import-reliant Asian economies. Energy traders are increasingly highlighting Indonesia, Vietnam, Pakistan and the Philippines as the countries most vulnerable to critical shortages, with some estimates suggesting fuel supplies could reach dangerous levels within a month if disruptions continue. Europe is also beginning to feel strain, particularly in jet fuel markets heading into the summer travel season.

The United States, despite becoming the world’s supplier of last resort, is facing its own inventory problems. U.S. crude stockpiles, including the Strategic Petroleum Reserve, have declined for four consecutive weeks. Refined petroleum products such as diesel and jet fuel recently fell to their lowest levels since 2005, while petrol (gasoline) inventories remain near their weakest seasonal levels since 2014. The United States itself has only deployed around 79.7 million barrels of the 172 million barrels it pledged to release, partly because policymakers are attempting to balance short-term supply needs against the longer-term risk of exhausting strategic reserves. If the full release proceeds, U.S. reserves would fall to their lowest level since 1982.

Governments are attempting to stabilise the market through strategic reserve releases. The International Energy Agency has already coordinated the release of a record 400 million barrels from emergency stockpiles. Yet even this creates a dilemma: every barrel released today further reduces the future buffer available if the conflict worsens.

Why oil prices could still move higher

At first glance, higher prices should solve the problem by reducing demand. To some extent this is already occurring. Global oil consumption has softened as elevated prices and supply disruptions begin constraining economic activity. However, analysts increasingly warn that demand destruction may not yet be sufficient to rebalance the market. Oil import-dependent countries could face critical shortages through the June-July period. And petrol shortages across parts of Asia could emerge rapidly if the Strait of Hormuz remains constrained into June.

This is the key point: inventories are falling faster than demand. As long as that imbalance persists, prices remain vulnerable to another leg higher. And even if the waterway reopens, the problem does not disappear immediately. Governments and companies will eventually need to rebuild depleted stockpiles, creating an entirely new layer of future demand. Demand will rise above pre-war levels as nations attempt to restore energy security buffers. In other words, the consequences of the conflict may continue influencing oil markets long after the fighting subsides.

Inflation and the economic cycle

The economic implications of sustained higher oil prices are significant. Oil sits near the centre of the global economy. When energy prices rise sharply, transportation, manufacturing, agriculture and retail costs all increase alongside it. This feeds directly into inflation.

During this stage, gold prices can soften despite geopolitical instability because higher inflation expectations also push bond yields upward. This temporarily makes fixed-income assets (bonds) more attractive relative to non-yielding gold. This explains why precious metals do not always rally immediately during geopolitical crises. However, this relationship changes once inflation begins outpacing bond yields. At that point, real returns on bonds deteriorate because investors lose purchasing power after accounting for inflation. Historically, this is the moment when gold tends to reassert itself as the preferred safe haven asset.

The sequence is often straightforward:

Oil prices rise. The cost of goods rises. Consumer spending contracts. Economic growth slows. Demand eventually weakens enough to pressure oil prices lower again.

But before that balancing process occurs, inflation can become highly disruptive to financial markets.

Precious metals and the next phase

As long as the oil crisis persists, precious metals prices may continue to experience periods of softness despite the broader geopolitical instability. Rising oil prices feed directly into inflation, which in turn support Treasury yields and strengthen the U.S. dollar in the short term. During this phase, capital often rotates toward yield-bearing safe havens such as government bonds rather than non-yielding assets like gold. This partially explains why precious metals have not responded as aggressively to the conflict as many initially expected.

However, this dynamic rarely lasts indefinitely. History shows that prolonged energy shocks eventually begin placing unsustainable pressure on the broader economy. Higher fuel costs filter through transportation, manufacturing, food production and consumer goods, steadily eroding purchasing power and slowing economic activity. At a certain point, inflation begins rising faster than bond yields can compensate and the market narrative shifts. What initially favoured bonds and cash transitions into a search for assets capable of preserving purchasing power in real terms and discounted assets as a result of the downturn. That is typically the point where precious metals begin outperforming more decisively.

In that sense, the current environment may ultimately prove to be the calm before the storm. The market is still attempting to absorb the inflationary consequences of higher oil prices while assuming the disruption remains temporary. But if inventories continue tightening, inflation persists, and economic stress deepens, the balance between bonds, currencies and precious metals is likely to shift once again. Historically, it is during these later-stage inflationary periods that gold and silver tend to emerge as the preferred safe haven assets.