Purchasing Precious Metals: How to Make Sense of Premiums

by Evie SoemardiThe past fortnight delivered one of the most dramatic reversals in silver’s modern history. After surging into overbought territory in January, silver’s euphoric run came to an abrupt end. At its peak on January 29th, silver reached an intraday high of AUD $172, only to plunge to AUD $92.90 by February 6th, a staggering $79 correction in just one week. It marked the most significant weekly decline since the volatility of the 1980s.

At the time of writing, gold trades at approximately AUD $7,093, silver at AUD $106.66, and platinum at AUD $2876. While the headline price moves captured attention, Australian retail investors quickly discovered that spot price is only one part of the equation. Two overlapping forces, extreme volatility and rising wholesale premiums, have shaped the local buying environment. Understanding both is essential when navigating precious metals markets during periods of stress.

Volatility: what really caused the crash?

Mainstream commentary was quick to attribute the sudden drop in asset prices to U.S. President Donald Trump’s nomination of Kevin Warsh as the next Federal Reserve Chair. Markets had largely anticipated a more dovish appointment, someone more likely to lower interest rates to support growth. Instead, Warsh is widely regarded as more hawkish, potentially favouring continued quantitative tightening and even rate hikes if inflation persists. News outlets framed the sell-off as a market repositioning event, investors adjusting expectations around interest rates and economic growth after Trump suggested Warsh could help deliver 15% economic expansion, something the U.S. has historically achieved only during wartime mobilisations.

However, while political headlines dominated coverage, a more mechanical force was unfolding beneath the surface. The CME Group (owners of the COMEX) raised margin requirements on silver from 15% to 18%, and on gold from 8% to 9%. In the following two weeks, margin requirements were adjusted upward three separate times.

When margin requirements rise, leveraged traders must either inject additional capital or liquidate positions. In a market already heavily leveraged, this can trigger cascading forced sales. Automatic stop-loss orders are hit. Positions are unwound. Selling feeds on itself. The result was not simply a change in economic expectations, it was a forced liquidation cycle. Historically, margin hikes have been used during overheated conditions to cool speculative excess. In this instance, the scale of leverage amplified the impact dramatically. Read more about the paper versus physical divide within Western markets here.

How did this affect the Australian market?

Volatility at this magnitude does more than move prices; it alters trading behaviour. Bullion merchants must constantly manage inventory risk. When silver swings $79 in a week, the ability to hedge exposure becomes strained. Depending on previous positioning and risk appetite, many dealers responded differently. Some temporarily closed trading; others limited online or in-store transactions; still others introduced minimum purchase thresholds.

Queensland Bullion Company was one of a very few operators that remained open and trading throughout the volatility, both in-store and online, but the broader industry response highlights how extreme paper market movements can disrupt physical retail access.

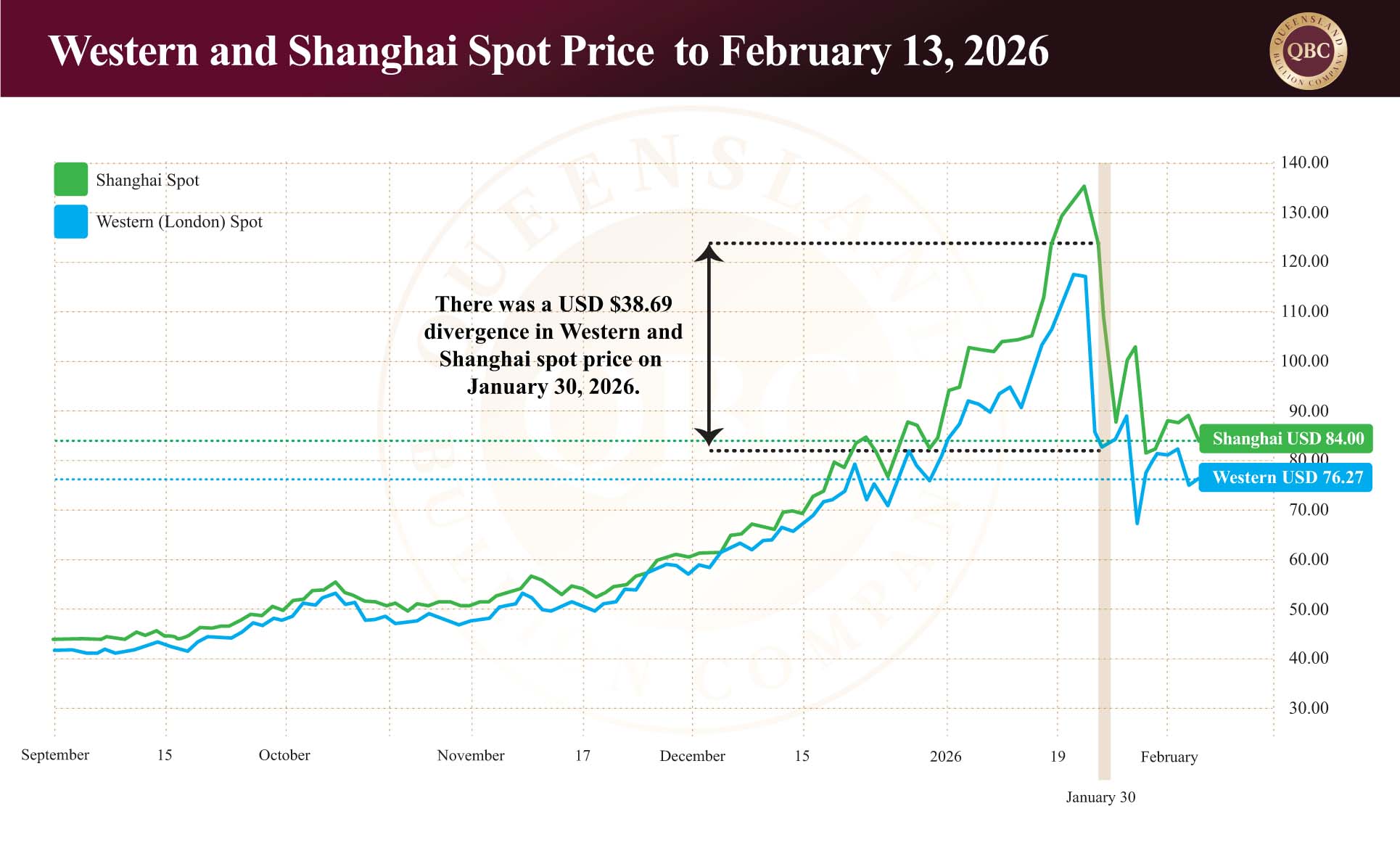

Western spot vs Shanghai spot: the physical disconnect

To understand premiums, one must understand the divergence between Western and Shanghai spot pricing. Western spot prices are derived primarily from futures contracts traded on the COMEX in New York and the London market. Each silver futures contract typically represents 5,000 troy ounces. However, for every contract backed by physical silver, estimates suggest there may be 350 or more paper claims referencing the same underlying metal. The result is a pricing mechanism dominated by leveraged financial instruments (paper contracts), not necessarily by physical supply.

China operates differently. Through a licensing system as at January 1, 2026, the Chinese government has limited exporters to approximately 44 approved entities and maintains tighter strategic control over silver flows, indicating its willingness to maintain as much control of physical silver as possible. Hence, Shanghai pricing reflects a market far more influenced by physical metal than derivatives.

Traditionally, Western and Shanghai spot prices track closely. But during January’s volatility, the gap widened dramatically. On January 30th the divergence reached USD $38.69, an unprecedented spread and a clear signal of strain within the Western paper market and the lack of silver in the system. When physical demand outpaces available supply and paper claims exceed deliverable metal disconnects appear.

Sourcing silver in Australia

Australian refineries historically sourced much of their stock domestically. That dynamic has now shifted.

With tight global supply conditions and a persistent five-year deficit between mined output and industrial demand, refineries are increasingly sourcing silver from Asia. Asian markets reference Shanghai pricing, not Western paper pricing. This means refinery input costs have risen materially. Those higher wholesale costs flow downstream: refineries pass increased costs to bullion merchants and bullion merchants adjust retail pricing via higher premiums.

Since the September 2025 bull run, wholesale premiums for silver have increased more than tenfold as wholesale costs balloon. Importantly, these higher premiums are largely reflected in bullion merchant sell prices, not buy-back prices, meaning investors selling silver are not typically receiving the same premium expansion.

This is a supply-chain adjustment, not opportunistic pricing.

In Summary

Two overlapping forces have shaped the current retail environment. The first is volatility, (driven largely by margin hikes and forced liquidation in leveraged futures markets) which disrupted normal trading conditions and triggered sharp price swings. The second is a structural shift in sourcing as refineries have become increasingly tied to higher Shanghai-based physical pricing, resulting in sustained increases in premiums across the supply chain.

Despite the turbulence, the broader backdrop remains intact. A five-year global supply deficit continues to weigh on the market, while new silver mines require seven to twelve years from discovery to production. At the same time, approximately 65% of silver demand is industrial, embedded in the infrastructure of modern living. The underlying market drivers have not changed. Corrections serve to reset excess, premiums reflect supply chain realities, and physical metal remains finite. For long-term investors, the message is clear: understand the mechanics, look beyond the noise, and continue accruing physical metal strategically.