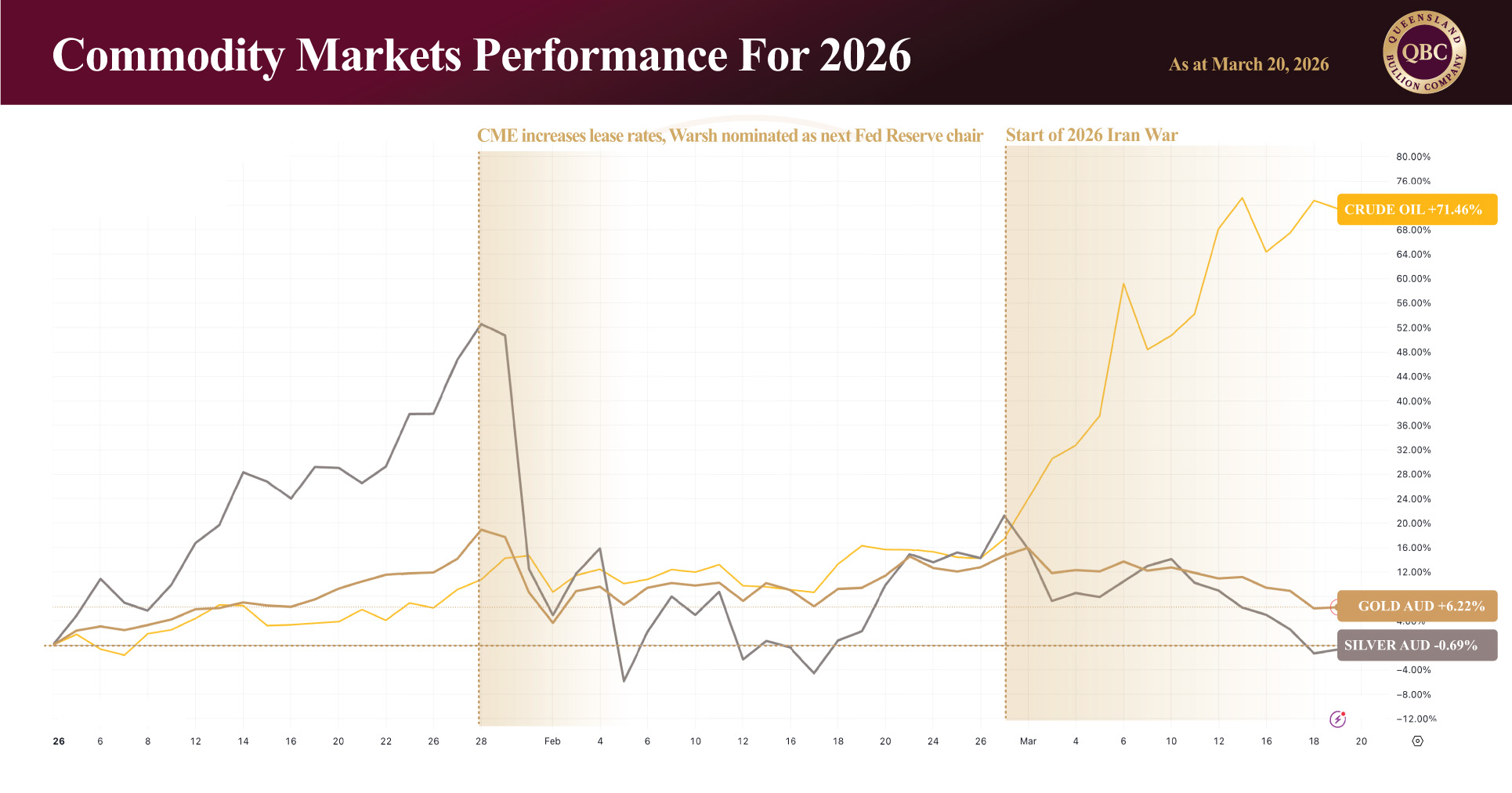

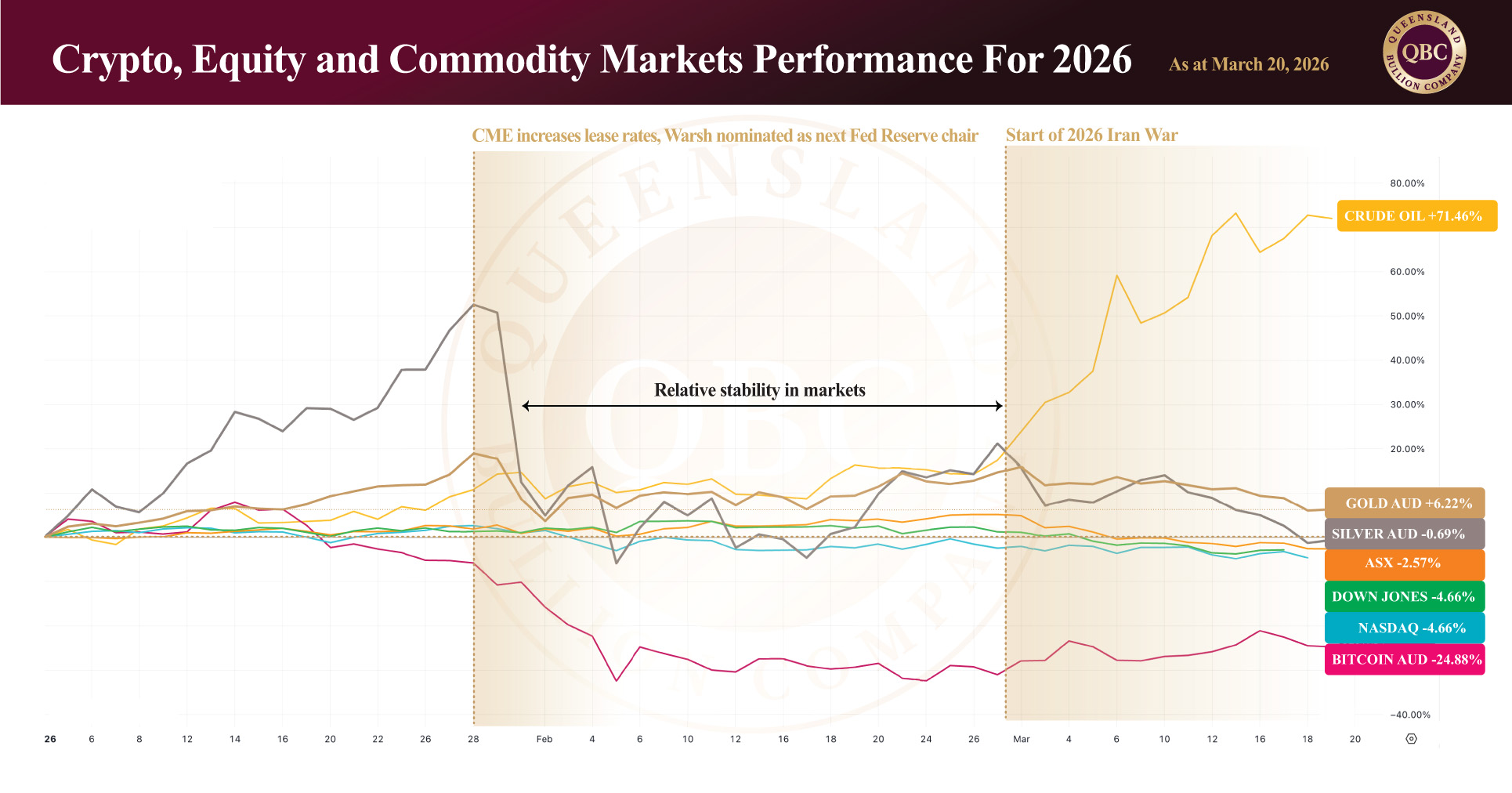

Commodities Lead as Markets Fracture

by Evie SoemardiGlobal markets in early 2026 have been defined by sharp divergence, elevated volatility, and a clear rotation toward hard assets. What began as a relatively stable opening to the year quickly shifted into a fragmented landscape, with capital fleeing risk and concentrating into select commodities. In local terms, gold currently trades at approximately AUD $6,662, silver at around AUD $104.33 and platinum near AUD $2,845.62. While broader markets have struggled to maintain direction, since the beginning of the year precious metals have demonstrated resilience even though the past four weeks has seen significant volatility, reinforcing their role as defensive anchors in uncertain conditions.

Oil Shock and Commodity Strength

The standout performer has been oil, surging over 70% in a matter of weeks in what can only be described as a classic supply shock response to geopolitical conflict. Gold has quietly followed, holding gains of over 6% year-to-date despite experiencing a sharp shakeout in February. Silver, while attracting criticism for its pullback from earlier highs, has in reality held steady across the same period, effectively flat after absorbing significant volatility. When viewed objectively, commodities (particularly oil, gold, and silver) are the strongest asset classes that have either advanced or maintained structural strength.

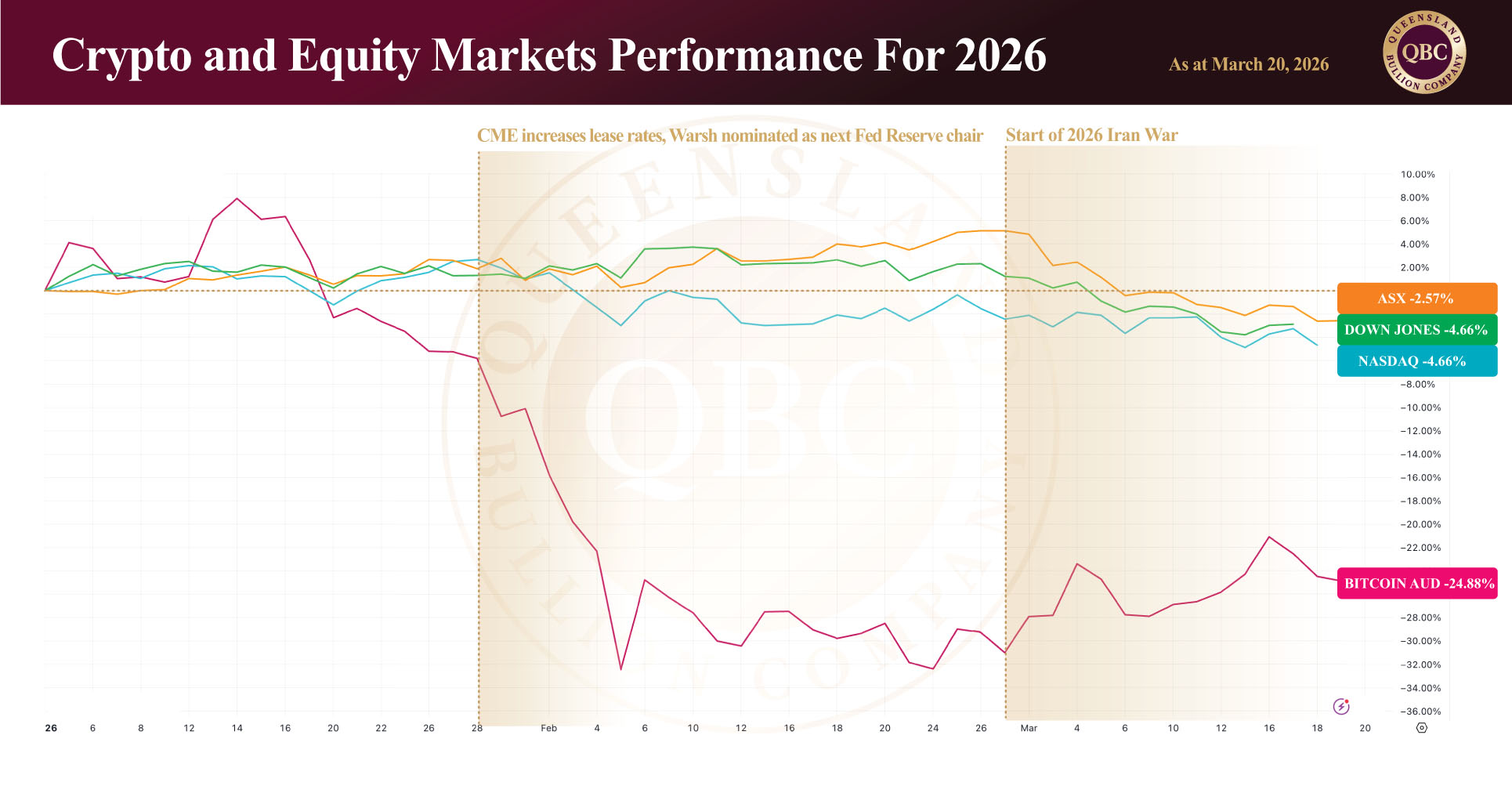

Equities and Crypto Under Pressure

By contrast, equities and cryptocurrencies have struggled under the same macro pressures. The ASX, Dow Jones, and Nasdaq have all drifted lower, while Bitcoin has experienced a far more severe drawdown, declining nearly 25% in Australian dollar terms. These moves reflect a broader risk-off environment thus far, where liquidity tightens and speculative assets are repriced. Despite this, the narrative focus has disproportionately centred on silver’s pullback, overlooking the broader context: it has outperformed most risk assets simply by holding its ground.

Event-Driven Volatility

Volatility this year has not been random; it has been event-driven. The late-January precious metals correction, triggered by rising lease rates, temporarily disrupted momentum and shook investor confidence. This was followed by the escalation of conflict in early March, which sent oil sharply higher and reinforced the global shift toward commodities. Between these two events, February appeared relatively subdued, though beneath the surface, risk assets (particularly crypto) continued to deteriorate. The pattern is clear: major macro events are dictating price action, not isolated market dynamics.

Silver Holding the Line

Looking ahead, silver remains technically constructive despite recent turbulence. It continues to trade within a broader upward trend established over the past year with gains of approximately 97% over twelve months still intact. While a break below key support around AUD $102 would challenge that structure, current sales volume trends suggest renewed buyer interest at lower levels. Australian bullion dealers are already reporting increased activity over the last 48 hours, indicating that investors are viewing recent price softness as an accumulation opportunity rather than a structural breakdown.

Gold Navigating Crosscurrents

Gold, meanwhile, is navigating a more complex set of influences. The U.S. Federal Reserve’s decision to hold rates, coupled with expectations of limited further easing, has supported yields and encouraged some rotation into income-generating assets such as Treasuries. At the same time, developments in the Middle East have intermittently restored risk-on sentiment, reducing immediate demand for safe-haven assets. Added to this, equity market weakness has forced some investors to liquidate gold positions to meet margin calls. These factors have contributed to short-term price softness; however, emerging rising volume suggests underlying demand remains intact.

Summary

What we are witnessing is not weakness in precious metals, but a broader repricing of global risk. In a year where equities, cryptocurrencies, and other speculative assets have struggled, gold and silver have demonstrated resilience by maintaining structure and attracting consistent demand. Volatility will remain a defining feature of this market, particularly as geopolitical tensions and monetary policy continue to evolve.

For investors, this environment reinforces a familiar but often overlooked principle: strength is not always measured by rapid gains, but by the ability to hold ground when everything else is falling. Gold and silver are doing exactly that. While short-term fluctuations may persist, the underlying trend of capital rotating toward tangible, non-counterparty assets remains firmly in place. In that context, current conditions are not a warning sign, they are a reminder of why precious metals continue to play a critical role in preserving wealth.